Advertisement

Improved Earnings Required Before Han's Laser Technology Industry Group Co., Ltd. (SZSE:002008) Shares Find Their Feet

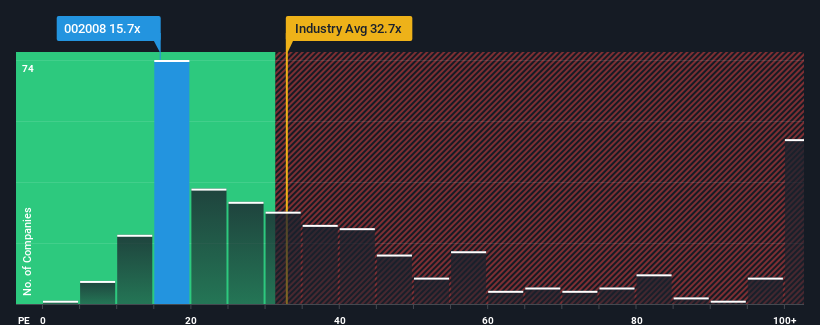

With a price-to-earnings (or "P/E") ratio of 15.7x Han's Laser Technology Industry Group Co., Ltd. (SZSE:002008) may be sending very bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 33x and even P/E's higher than 63x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been pleasing for Han's Laser Technology Industry Group as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Han's Laser Technology Industry Group

How Is Han's Laser Technology Industry Group's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Han's Laser Technology Industry Group's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered an exceptional 95% gain to the company's bottom line. As a result, it also grew EPS by 12% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 21% during the coming year according to the eight analysts following the company. With the market predicted to deliver 38% growth , that's a disappointing outcome.

With this information, we are not surprised that Han's Laser Technology Industry Group is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Final Word

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Han's Laser Technology Industry Group's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 2 warning signs for Han's Laser Technology Industry Group (1 is a bit concerning!) that we have uncovered.

If you're unsure about the strength of Han's Laser Technology Industry Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Han's Laser Technology Industry Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002008

Han's Laser Technology Industry Group

Researches, develops, produces, and sells laser processing equipment in China and internationally.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor