Advertisement

Revenues Working Against Conch (Anhui) Energy Saving and Environment Protection New Material Co., Ltd.'s (SZSE:000619) Share Price

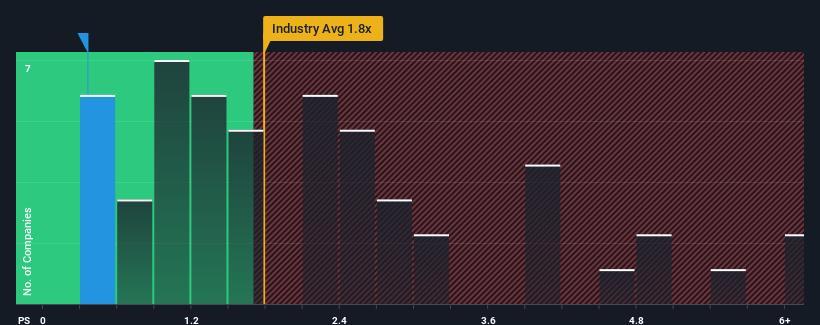

When close to half the companies operating in the Building industry in China have price-to-sales ratios (or "P/S") above 1.8x, you may consider Conch (Anhui) Energy Saving and Environment Protection New Material Co., Ltd. (SZSE:000619) as an attractive investment with its 0.4x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Conch (Anhui) Energy Saving and Environment Protection New Material

What Does Conch (Anhui) Energy Saving and Environment Protection New Material's P/S Mean For Shareholders?

The recent revenue growth at Conch (Anhui) Energy Saving and Environment Protection New Material would have to be considered satisfactory if not spectacular. It might be that many expect the respectable revenue performance to degrade, which has repressed the P/S. If that doesn't eventuate, then existing shareholders may have reason to be optimistic about the future direction of the share price.

Although there are no analyst estimates available for Conch (Anhui) Energy Saving and Environment Protection New Material, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Conch (Anhui) Energy Saving and Environment Protection New Material's Revenue Growth Trending?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Conch (Anhui) Energy Saving and Environment Protection New Material's to be considered reasonable.

Retrospectively, the last year delivered a decent 5.7% gain to the company's revenues. Pleasingly, revenue has also lifted 48% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Comparing that to the industry, which is predicted to deliver 25% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this information, we can see why Conch (Anhui) Energy Saving and Environment Protection New Material is trading at a P/S lower than the industry. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

What We Can Learn From Conch (Anhui) Energy Saving and Environment Protection New Material's P/S?

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

In line with expectations, Conch (Anhui) Energy Saving and Environment Protection New Material maintains its low P/S on the weakness of its recent three-year growth being lower than the wider industry forecast. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. If recent medium-term revenue trends continue, it's hard to see the share price experience a reversal of fortunes anytime soon.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Conch (Anhui) Energy Saving and Environment Protection New Material (2 don't sit too well with us!) that you should be aware of before investing here.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000619

Conch (Anhui) Energy Saving and Environment Protection New Material

Manufactures and sells plastic, aluminum, and eco-home furnishings in China, Thailand, Myanmar, Indonesia, Uzbekistan, and internationally.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor