Advertisement

- China

- /

- Aerospace & Defense

- /

- SHSE:688523

Hunan Aerospace Huanyu Communication Technology Co.,LTD. (SHSE:688523) Looks Just Right With A 30% Price Jump

Hunan Aerospace Huanyu Communication Technology Co.,LTD. (SHSE:688523) shareholders are no doubt pleased to see that the share price has bounced 30% in the last month, although it is still struggling to make up recently lost ground. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

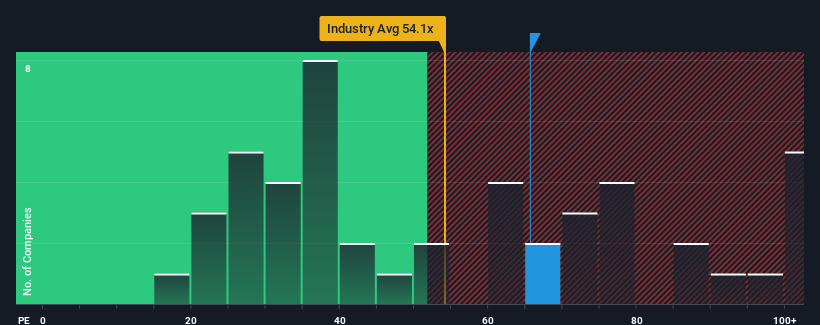

After such a large jump in price, given close to half the companies in China have price-to-earnings ratios (or "P/E's") below 30x, you may consider Hunan Aerospace Huanyu Communication TechnologyLTD as a stock to avoid entirely with its 65.6x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Recent times have been pleasing for Hunan Aerospace Huanyu Communication TechnologyLTD as its earnings have risen in spite of the market's earnings going into reverse. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Hunan Aerospace Huanyu Communication TechnologyLTD

How Is Hunan Aerospace Huanyu Communication TechnologyLTD's Growth Trending?

In order to justify its P/E ratio, Hunan Aerospace Huanyu Communication TechnologyLTD would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a decent 3.6% gain to the company's bottom line. Pleasingly, EPS has also lifted 40% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 79% during the coming year according to the one analyst following the company. Meanwhile, the rest of the market is forecast to only expand by 41%, which is noticeably less attractive.

With this information, we can see why Hunan Aerospace Huanyu Communication TechnologyLTD is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Hunan Aerospace Huanyu Communication TechnologyLTD's P/E

The strong share price surge has got Hunan Aerospace Huanyu Communication TechnologyLTD's P/E rushing to great heights as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Hunan Aerospace Huanyu Communication TechnologyLTD maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Hunan Aerospace Huanyu Communication TechnologyLTD with six simple checks.

If you're unsure about the strength of Hunan Aerospace Huanyu Communication TechnologyLTD's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hunan Aerospace Huanyu Communication TechnologyLTD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688523

Hunan Aerospace Huanyu Communication TechnologyLTD

Hunan Aerospace Huanyu Communication Technology Co.,LTD.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor