Advertisement

As global markets navigate the complexities of new U.S. tariffs and mixed economic signals, Asian markets are capturing attention with their potential for resilience and growth amidst these challenges. In this context, identifying promising small-cap stocks requires a focus on companies that can adapt to shifting trade dynamics and leverage regional economic trends.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Ascentech K.K | NA | 133.18% | 172.84% | ★★★★★★ |

| Episil-Precision | 19.76% | 0.57% | 16.64% | ★★★★★★ |

| Torigoe | 9.03% | 4.76% | 8.35% | ★★★★★☆ |

| Hangzhou Zhengqiang | 26.03% | 2.95% | 16.75% | ★★★★★☆ |

| Uniplus Electronics | 32.17% | 46.30% | 75.33% | ★★★★★☆ |

| KinjiroLtd | 22.32% | 10.69% | 21.02% | ★★★★★☆ |

| Lucky Cement | 61.41% | 4.55% | 15.65% | ★★★★☆☆ |

| Toho Bank | 112.58% | 4.41% | 32.71% | ★★★★☆☆ |

| ASRock Rack Incorporation | 26.93% | 225.32% | 6287.64% | ★★★★☆☆ |

| Lan Fa Textile | 59.50% | -14.81% | 9.91% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

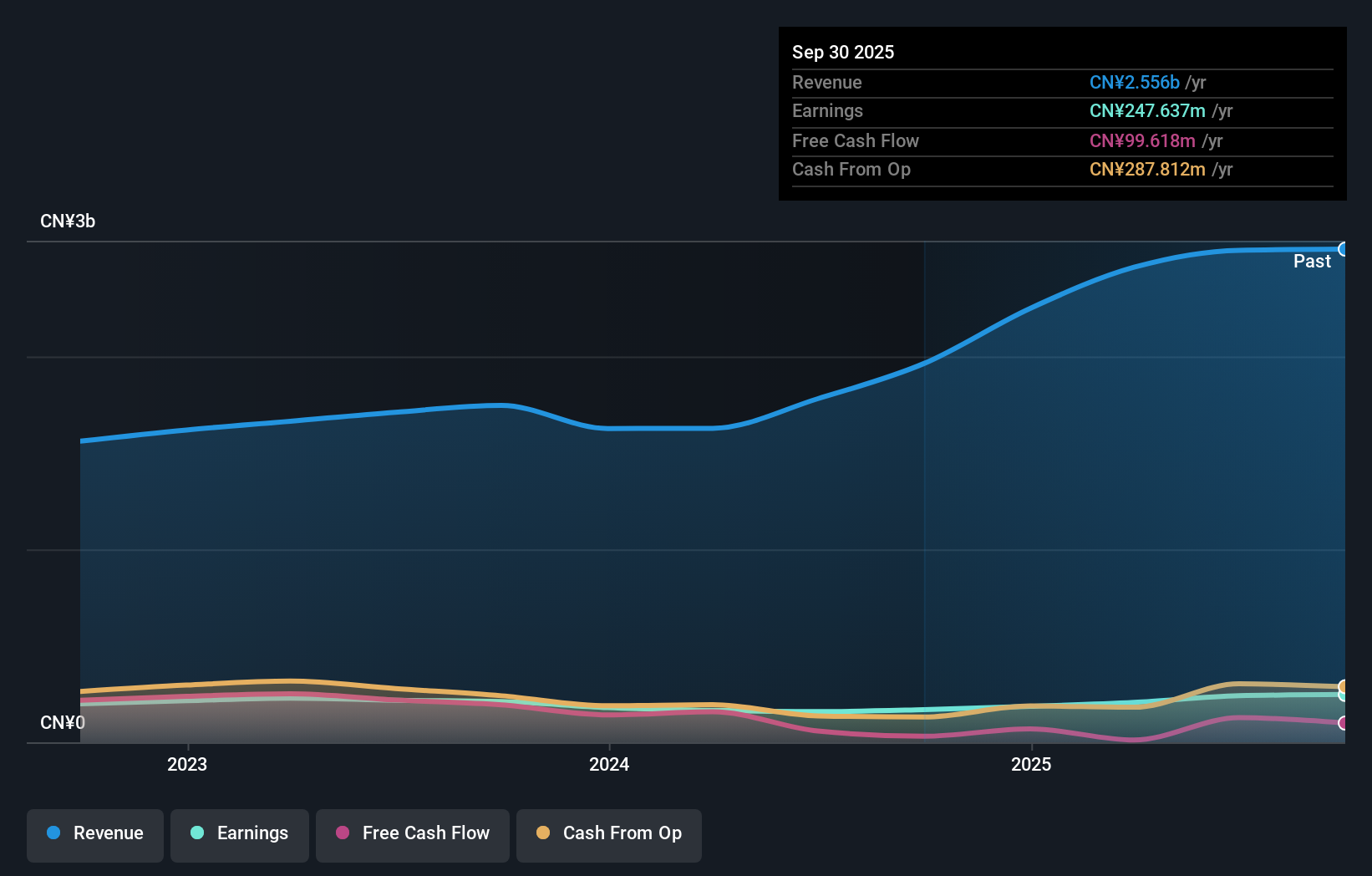

Lutian Machinery (SHSE:605259)

Simply Wall St Value Rating: ★★★★★★

Overview: Lutian Machinery Co., Ltd. specializes in the research, design, development, production, and sale of general power machinery and high-pressure washers in China with a market capitalization of approximately CN¥4.57 billion.

Operations: Lutian Machinery generates revenue primarily from its general equipment manufacturing segment, which accounts for CN¥2.46 billion.

Lutian Machinery, a nimble player in the machinery sector, shows promising financial health with no debt over the past five years and a price-to-earnings ratio of 22.1x, which is attractively below the CN market average of 40.4x. The company reported robust earnings growth of 25.1% last year, outpacing the industry’s mere 1% increase. Recent results highlight strong performance with first-quarter revenue hitting CNY 638.64 million compared to CNY 425.43 million from the previous year and net income climbing to CNY 57.42 million from CNY 36.72 million, reflecting its solid operational footing and potential for continued growth in an evolving market landscape.

- Take a closer look at Lutian Machinery's potential here in our health report.

Gain insights into Lutian Machinery's past trends and performance with our Past report.

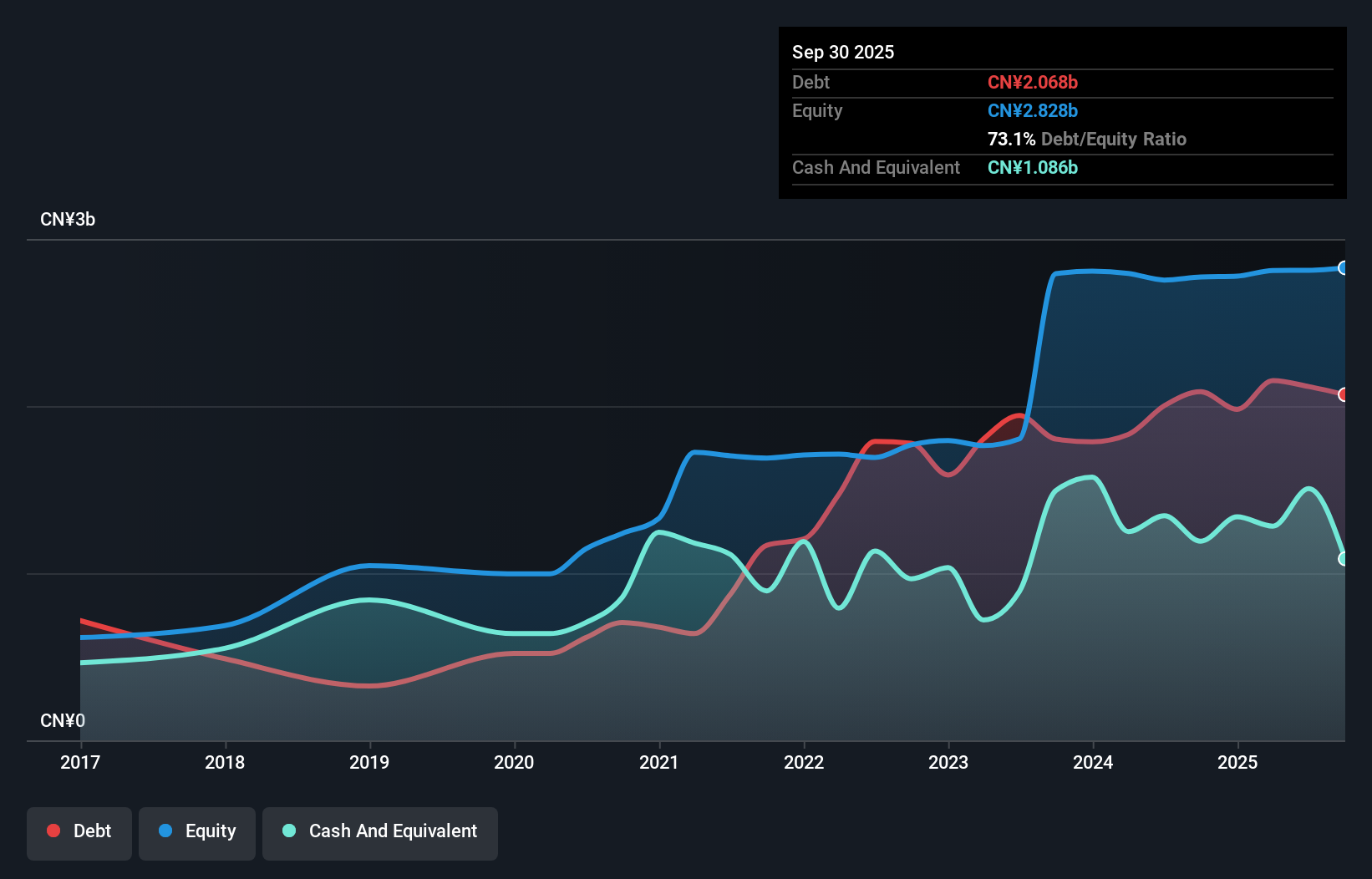

Guangdong Sanhe Pile (SZSE:003037)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Guangdong Sanhe Pile Co., Ltd. specializes in the R&D, production, and sale of prestressed concrete pipe pile products in China with a market cap of CN¥5.64 billion.

Operations: Sanhe Pile's revenue is primarily derived from the sale of prestressed concrete pipe pile products. The company has a market cap of CN¥5.64 billion, indicating its significant presence in the industry.

Guangdong Sanhe Pile, a nimble player in the industry, has demonstrated resilience with a notable earnings surge of 47.5% over the past year, outpacing its sector's -15.1%. Despite earnings declining by 32.8% annually over five years, recent figures show improvement; Q1 2025 saw net income at CNY 34.6 million compared to a loss last year. The company's debt management appears prudent with a net debt to equity ratio at 31%, deemed satisfactory, and interest payments well covered by EBIT at 3.5x coverage. While free cash flow remains negative, profitability ensures cash runway stability for future operations and growth prospects remain cautiously optimistic.

- Dive into the specifics of Guangdong Sanhe Pile here with our thorough health report.

Evaluate Guangdong Sanhe Pile's historical performance by accessing our past performance report.

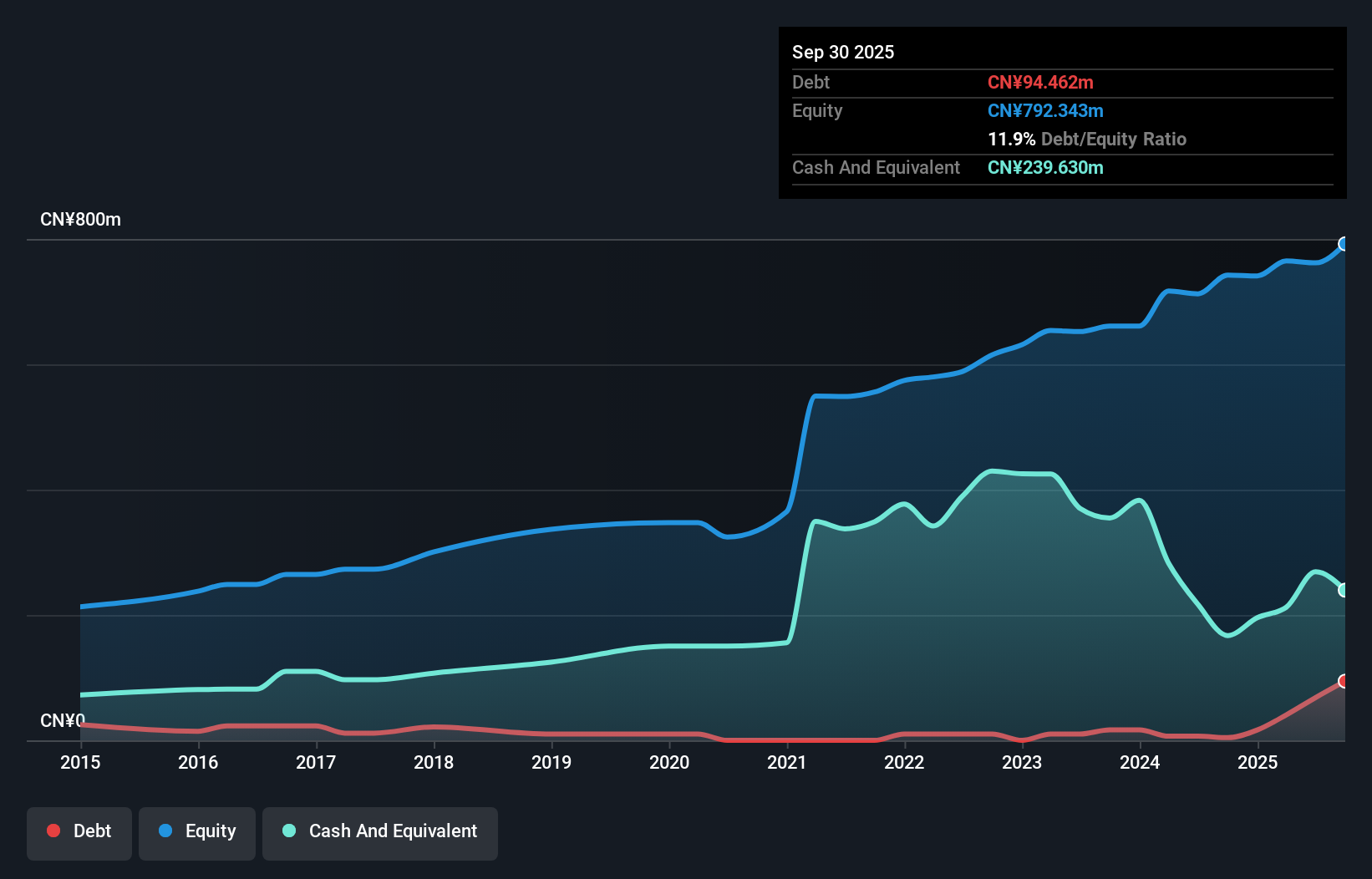

DorightLtd (SZSE:300950)

Simply Wall St Value Rating: ★★★★★☆

Overview: Doright Co., Ltd. specializes in the design, R&D, manufacturing, inspection, sales, and servicing of energy-saving environmental protection equipment in China with a market cap of CN¥4.50 billion.

Operations: DorightLtd generates revenue primarily through the sale and servicing of energy-saving environmental protection equipment. The company's cost structure includes expenses related to manufacturing and R&D. Notably, its gross profit margin is 35%, reflecting the efficiency in managing production costs relative to sales.

Doright Ltd., a smaller player in the Asian market, has seen its earnings grow by 1.3% over the past year, outpacing the Machinery industry’s 1% growth. Despite this, recent financial results show a dip in performance with first-quarter sales at CNY 124.7 million compared to CNY 181.21 million last year and net income at CNY 23.67 million down from CNY 50.63 million previously. The company’s debt-to-equity ratio has increased from 2.9 to 5.3 over five years, indicating rising leverage but remains profitable with high-quality earnings and sufficient interest coverage.

- Click here to discover the nuances of DorightLtd with our detailed analytical health report.

Gain insights into DorightLtd's historical performance by reviewing our past performance report.

Next Steps

- Unlock more gems! Our Asian Undiscovered Gems With Strong Fundamentals screener has unearthed 2608 more companies for you to explore.Click here to unveil our expertly curated list of 2611 Asian Undiscovered Gems With Strong Fundamentals.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300950

DorightLtd

Engages in the design, research and development, manufacture, inspection, sale, and servicing of energy-saving environmental protection equipment in China.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative