Advertisement

Earnings Not Telling The Story For Zhejiang Tiantai Xianghe Industrial Co.,Ltd. (SHSE:603500) After Shares Rise 34%

Despite an already strong run, Zhejiang Tiantai Xianghe Industrial Co.,Ltd. (SHSE:603500) shares have been powering on, with a gain of 34% in the last thirty days. Notwithstanding the latest gain, the annual share price return of 8.8% isn't as impressive.

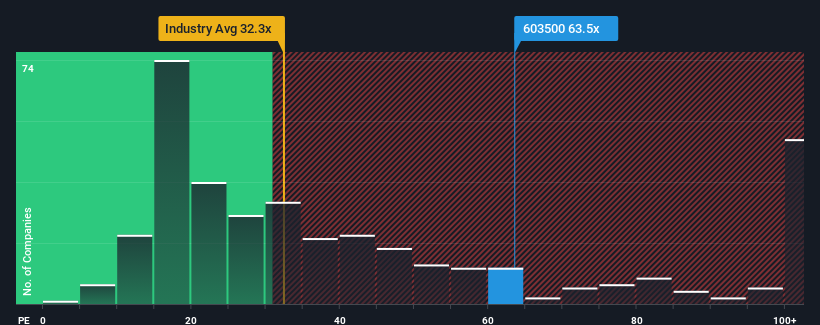

Since its price has surged higher, Zhejiang Tiantai Xianghe IndustrialLtd may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 63.5x, since almost half of all companies in China have P/E ratios under 32x and even P/E's lower than 19x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

As an illustration, earnings have deteriorated at Zhejiang Tiantai Xianghe IndustrialLtd over the last year, which is not ideal at all. One possibility is that the P/E is high because investors think the company will still do enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Zhejiang Tiantai Xianghe IndustrialLtd

Is There Enough Growth For Zhejiang Tiantai Xianghe IndustrialLtd?

The only time you'd be truly comfortable seeing a P/E as steep as Zhejiang Tiantai Xianghe IndustrialLtd's is when the company's growth is on track to outshine the market decidedly.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 20%. As a result, earnings from three years ago have also fallen 21% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 38% shows it's an unpleasant look.

In light of this, it's alarming that Zhejiang Tiantai Xianghe IndustrialLtd's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

What We Can Learn From Zhejiang Tiantai Xianghe IndustrialLtd's P/E?

Zhejiang Tiantai Xianghe IndustrialLtd's P/E is flying high just like its stock has during the last month. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Zhejiang Tiantai Xianghe IndustrialLtd revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Zhejiang Tiantai Xianghe IndustrialLtd (of which 1 shouldn't be ignored!) you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Tiantai Xianghe IndustrialLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603500

Zhejiang Tiantai Xianghe IndustrialLtd

Zhejiang Tiantai Xianghe Industrial Co.,Ltd.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor