Advertisement

Is Shanghai Highly (Group) (SHSE:600619) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Shanghai Highly (Group) Co., Ltd. (SHSE:600619) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Shanghai Highly (Group)

What Is Shanghai Highly (Group)'s Net Debt?

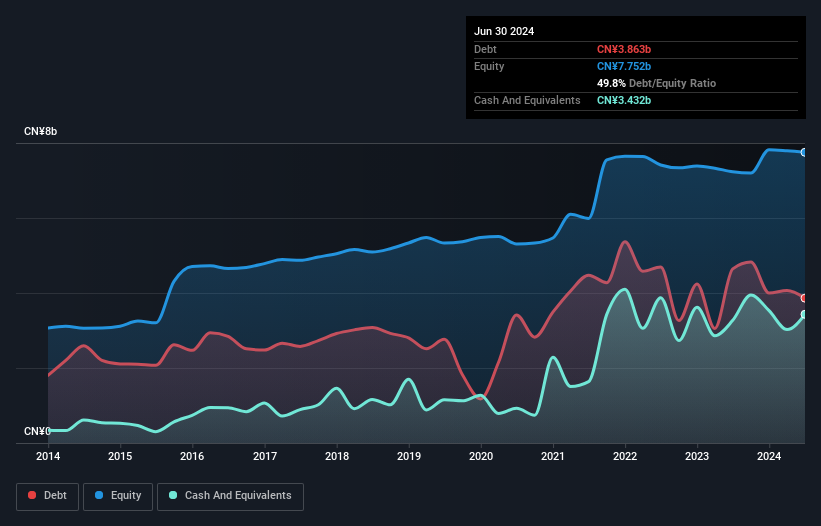

You can click the graphic below for the historical numbers, but it shows that Shanghai Highly (Group) had CN¥3.86b of debt in June 2024, down from CN¥4.64b, one year before. On the flip side, it has CN¥3.43b in cash leading to net debt of about CN¥431.1m.

How Healthy Is Shanghai Highly (Group)'s Balance Sheet?

The latest balance sheet data shows that Shanghai Highly (Group) had liabilities of CN¥11.7b due within a year, and liabilities of CN¥2.35b falling due after that. Offsetting these obligations, it had cash of CN¥3.43b as well as receivables valued at CN¥6.99b due within 12 months. So its liabilities total CN¥3.60b more than the combination of its cash and short-term receivables.

Shanghai Highly (Group) has a market capitalization of CN¥8.32b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Given net debt is only 0.57 times EBITDA, it is initially surprising to see that Shanghai Highly (Group)'s EBIT has low interest coverage of 1.2 times. So one way or the other, it's clear the debt levels are not trivial. We also note that Shanghai Highly (Group) improved its EBIT from a last year's loss to a positive CN¥107m. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Shanghai Highly (Group)'s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Happily for any shareholders, Shanghai Highly (Group) actually produced more free cash flow than EBIT over the last year. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Based on what we've seen Shanghai Highly (Group) is not finding it easy, given its interest cover, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its conversion of EBIT to free cash flow. When we consider all the elements mentioned above, it seems to us that Shanghai Highly (Group) is managing its debt quite well. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for Shanghai Highly (Group) (1 is significant) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600619

Shanghai Highly (Group)

Researches, develops, manufactures, and sells components for white goods and energy vehicles in China and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|62.4% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.2% undervalued

ZW

Community Contributor