Advertisement

- China

- /

- Electrical

- /

- SHSE:600577

Tongling Jingda Special Magnet Wire (SHSE:600577) Has A Pretty Healthy Balance Sheet

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Tongling Jingda Special Magnet Wire Co., Ltd. (SHSE:600577) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Tongling Jingda Special Magnet Wire

What Is Tongling Jingda Special Magnet Wire's Net Debt?

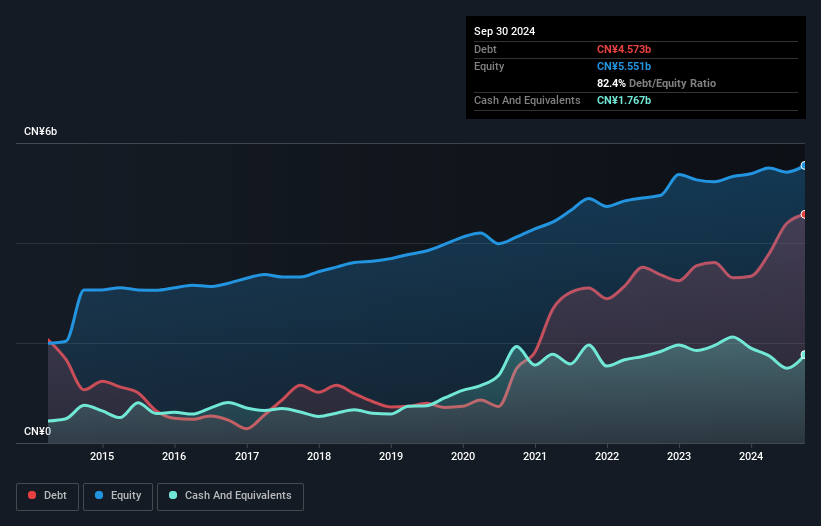

You can click the graphic below for the historical numbers, but it shows that as of September 2024 Tongling Jingda Special Magnet Wire had CN¥4.57b of debt, an increase on CN¥3.30b, over one year. However, it does have CN¥1.77b in cash offsetting this, leading to net debt of about CN¥2.81b.

How Healthy Is Tongling Jingda Special Magnet Wire's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Tongling Jingda Special Magnet Wire had liabilities of CN¥6.48b due within 12 months and liabilities of CN¥814.0m due beyond that. On the other hand, it had cash of CN¥1.77b and CN¥6.09b worth of receivables due within a year. So it actually has CN¥572.0m more liquid assets than total liabilities.

This short term liquidity is a sign that Tongling Jingda Special Magnet Wire could probably pay off its debt with ease, as its balance sheet is far from stretched.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Tongling Jingda Special Magnet Wire has a debt to EBITDA ratio of 3.0 and its EBIT covered its interest expense 6.5 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. We note that Tongling Jingda Special Magnet Wire grew its EBIT by 21% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Tongling Jingda Special Magnet Wire's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Tongling Jingda Special Magnet Wire created free cash flow amounting to 9.7% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

On our analysis Tongling Jingda Special Magnet Wire's EBIT growth rate should signal that it won't have too much trouble with its debt. But the other factors we noted above weren't so encouraging. For instance it seems like it has to struggle a bit to convert EBIT to free cash flow. When we consider all the elements mentioned above, it seems to us that Tongling Jingda Special Magnet Wire is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example Tongling Jingda Special Magnet Wire has 2 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Tongling Jingda Special Magnet Wire might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600577

Tongling Jingda Special Magnet Wire

Tongling Jingda Special Magnet Wire Co., Ltd.

Solid track record and fair value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor