Advertisement

- China

- /

- Auto Components

- /

- SZSE:002715

Huaiji Dengyun Auto-parts (Holding) Co.,Ltd. (SZSE:002715) May Have Run Too Fast Too Soon With Recent 26% Price Plummet

The Huaiji Dengyun Auto-parts (Holding) Co.,Ltd. (SZSE:002715) share price has softened a substantial 26% over the previous 30 days, handing back much of the gains the stock has made lately. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 12%.

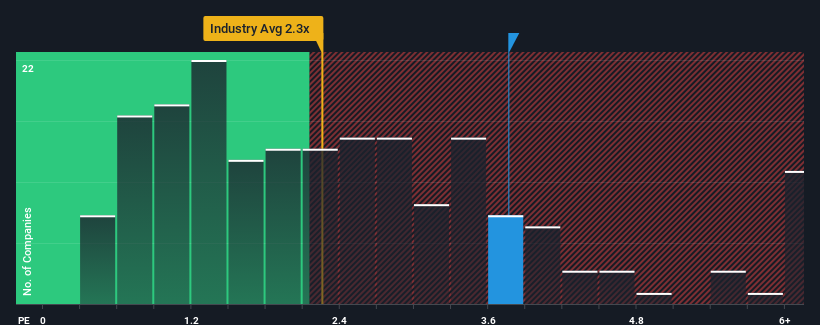

In spite of the heavy fall in price, you could still be forgiven for thinking Huaiji Dengyun Auto-parts (Holding)Ltd is a stock not worth researching with a price-to-sales ratios (or "P/S") of 3.8x, considering almost half the companies in China's Auto Components industry have P/S ratios below 2.3x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

See our latest analysis for Huaiji Dengyun Auto-parts (Holding)Ltd

What Does Huaiji Dengyun Auto-parts (Holding)Ltd's Recent Performance Look Like?

Revenue has risen at a steady rate over the last year for Huaiji Dengyun Auto-parts (Holding)Ltd, which is generally not a bad outcome. It might be that many expect the reasonable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Huaiji Dengyun Auto-parts (Holding)Ltd will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Huaiji Dengyun Auto-parts (Holding)Ltd?

In order to justify its P/S ratio, Huaiji Dengyun Auto-parts (Holding)Ltd would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered a decent 4.7% gain to the company's revenues. Pleasingly, revenue has also lifted 33% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing that to the industry, which is predicted to deliver 25% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this information, we find it concerning that Huaiji Dengyun Auto-parts (Holding)Ltd is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

There's still some elevation in Huaiji Dengyun Auto-parts (Holding)Ltd's P/S, even if the same can't be said for its share price recently. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Huaiji Dengyun Auto-parts (Holding)Ltd revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

Before you take the next step, you should know about the 1 warning sign for Huaiji Dengyun Auto-parts (Holding)Ltd that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Huaiji Dengyun Auto-parts (Holding)Ltd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002715

Huaiji Dengyun Auto-parts (Holding)Ltd

Huaiji Dengyun Auto-parts (Holding) Co.,Ltd.

Mediocre balance sheet low.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor