Temenos (SWX:TEMN) has drawn fresh attention after a shift in its recent stock movement. Investors are closely watching how the company’s performance metrics and market sentiment could shape its outlook in the coming months.

Temenos has seen renewed momentum lately, with the share price climbing 14% over the past month and posting a 15% year-to-date gain. While its one-year total shareholder return stands at an impressive 27%, it is still working to recover from deeper five-year losses. Investors seem to be responding to signs of improving sentiment and possible growth potential, but long-term holders are watching for a more sustained turnaround.

But with Temenos trading so close to its analyst price target, investors may be wondering if there is genuine value left to unlock or if the market has already accounted for any future upside.

Advertisement

Price-to-Earnings of 20.1x: Is it justified?

Temenos shares currently trade at a price-to-earnings (P/E) ratio of 20.1x, notably lower than both its peer group and the overall European Software industry. With a last close price of CHF74.2, the market is pricing in expectations that set Temenos apart from its competitors.

The price-to-earnings ratio compares a company’s share price with its earnings per share, offering a snapshot of how much investors are willing to pay for each unit of profit. For software companies like Temenos, this metric reflects market sentiment around profitability and growth prospects, important factors for a sector often characterized by high growth expectations.

Temenos stands out with a P/E of 20.1x while its European Software industry peers average 26.4x and its direct peer group averages an even higher 40.3x. This suggests the market may be underpricing Temenos’s current earnings and overlooking its growth potential. If the P/E ratio were to converge with sector norms, the stock could see meaningful upside, especially if future earnings deliver.

However, persistent net income declines and a multi-year negative total return could quickly challenge the bullish outlook if recent momentum stalls or if fundamentals deteriorate further.

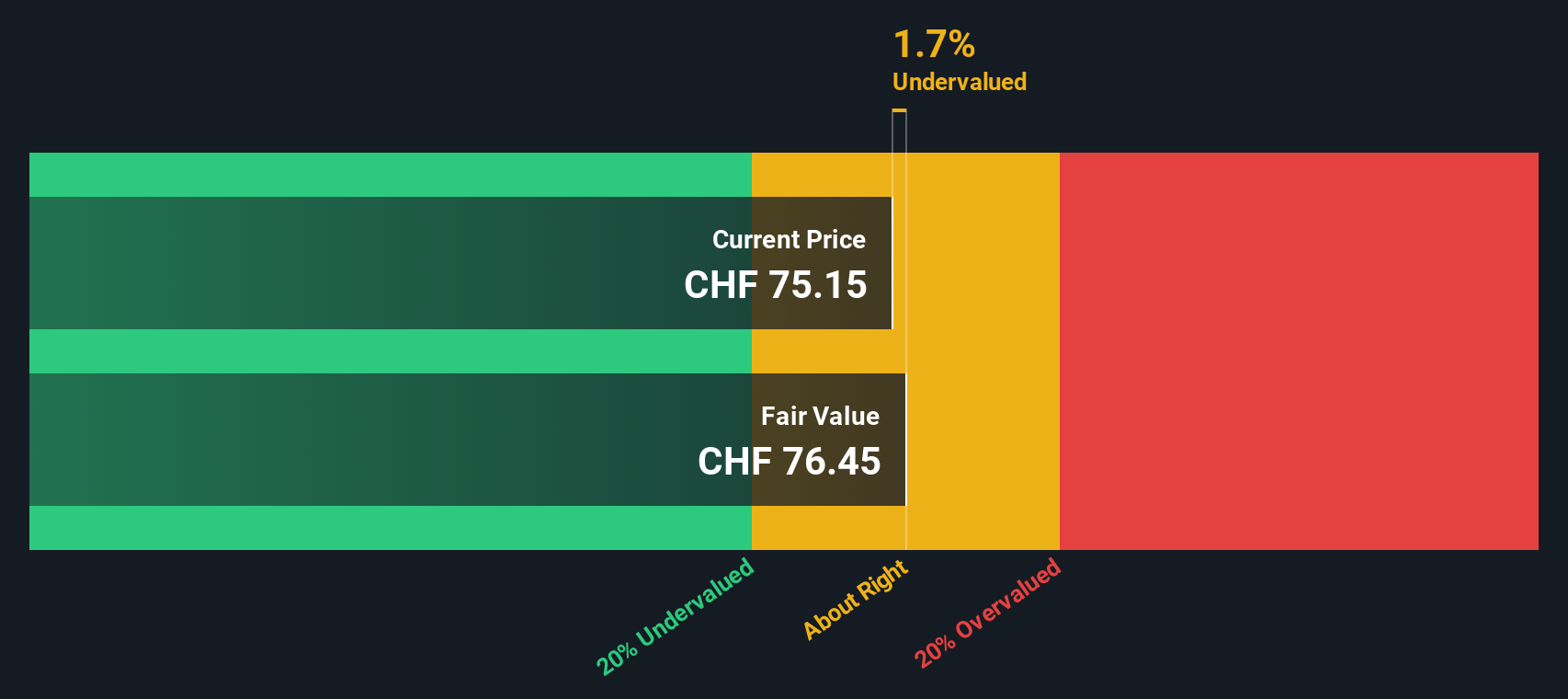

While the price-to-earnings ratio points to potential undervaluation, our DCF model offers a different angle. Based on future cash flows, Temenos is trading about 2.3% below our fair value estimate, making it look slightly undervalued. However, does a modest margin signal hidden upside or simply reflect low growth expectations?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Temenos for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 863 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Temenos Narrative

If you have a different perspective or want to analyze the numbers on your own terms, you can craft your own viewpoint in just a few minutes with Do it your way.

Take control of your portfolio and get ahead by targeting new sectors and trends. Don’t let fresh opportunities slip past while you wait for tomorrow.

Tap into powerful recurring income by reviewing these 16 dividend stocks with yields > 3%, which is packed with stocks yielding over 3% for steady cash flow potential.

Supercharge your exposure to the rise of artificial intelligence through these 24 AI penny stocks, which are reshaping how our economy operates and grows.

Position yourself at the intersection of finance and innovation by checking out these 82 cryptocurrency and blockchain stocks, making waves in digital payments and blockchain progress.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.