- Switzerland

- /

- Food

- /

- SWX:BARN

Three Companies On SIX Swiss Exchange That May Be Trading Below Estimated Value

Reviewed by Simply Wall St

The Swiss market recently experienced a slight downturn, with the SMI index closing marginally lower despite a late recovery, reflecting mixed performances across various sectors. In this context of fluctuating market conditions, identifying undervalued stocks can be crucial for investors seeking opportunities that may offer potential value relative to their current trading prices.

Top 10 Undervalued Stocks Based On Cash Flows In Switzerland

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Swissquote Group Holding (SWX:SQN) | CHF300.80 | CHF559.34 | 46.2% |

| Georg Fischer (SWX:GF) | CHF55.50 | CHF108.29 | 48.7% |

| lastminute.com (SWX:LMN) | CHF18.10 | CHF28.90 | 37.4% |

| Julius Bär Gruppe (SWX:BAER) | CHF54.32 | CHF103.78 | 47.7% |

| Comet Holding (SWX:COTN) | CHF296.00 | CHF526.48 | 43.8% |

| Komax Holding (SWX:KOMN) | CHF115.20 | CHF202.72 | 43.2% |

| Clariant (SWX:CLN) | CHF12.32 | CHF21.43 | 42.5% |

| Dätwyler Holding (SWX:DAE) | CHF150.60 | CHF237.50 | 36.6% |

| SGS (SWX:SGSN) | CHF94.34 | CHF151.17 | 37.6% |

| Sensirion Holding (SWX:SENS) | CHF67.20 | CHF117.64 | 42.9% |

Let's dive into some prime choices out of the screener.

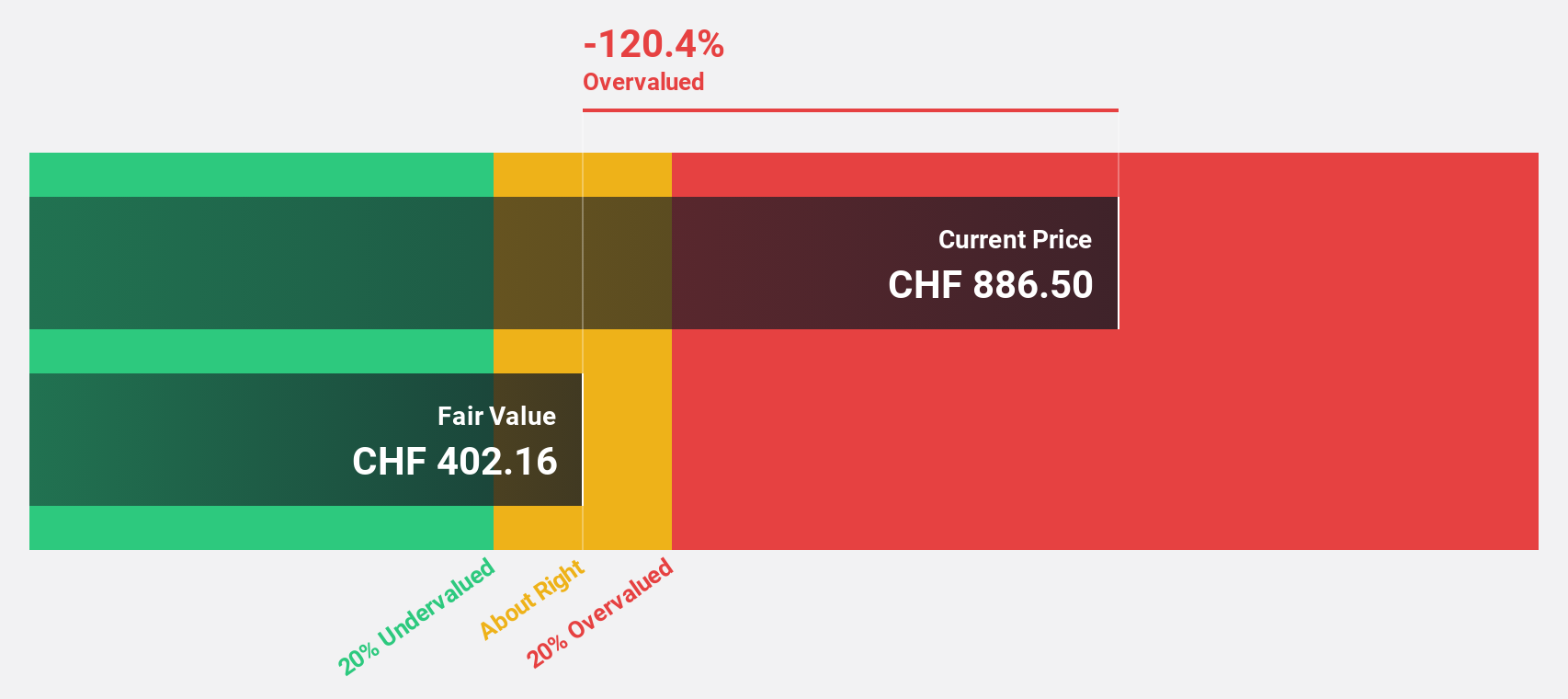

ALSO Holding (SWX:ALSN)

Overview: ALSO Holding AG is a technology services provider for the ICT industry operating in Switzerland, Germany, the Netherlands, Poland, and internationally with a market cap of CHF2.95 billion.

Operations: The company's revenue is primarily derived from its operations in Central Europe, generating €4.62 billion, and Northern/Eastern Europe, contributing €5.24 billion.

Estimated Discount To Fair Value: 33.3%

ALSO Holding is trading at CHF240.5, significantly below its estimated fair value of CHF360.34, suggesting it is undervalued by over 33%. Despite a volatile share price recently, earnings are projected to grow at 26.8% annually, outpacing the Swiss market's growth rate of 11.6%. While revenue growth is slower than earnings, it still surpasses the broader market's pace. The company offers a stable dividend yield of 1.88%.

- Our comprehensive growth report raises the possibility that ALSO Holding is poised for substantial financial growth.

- Dive into the specifics of ALSO Holding here with our thorough financial health report.

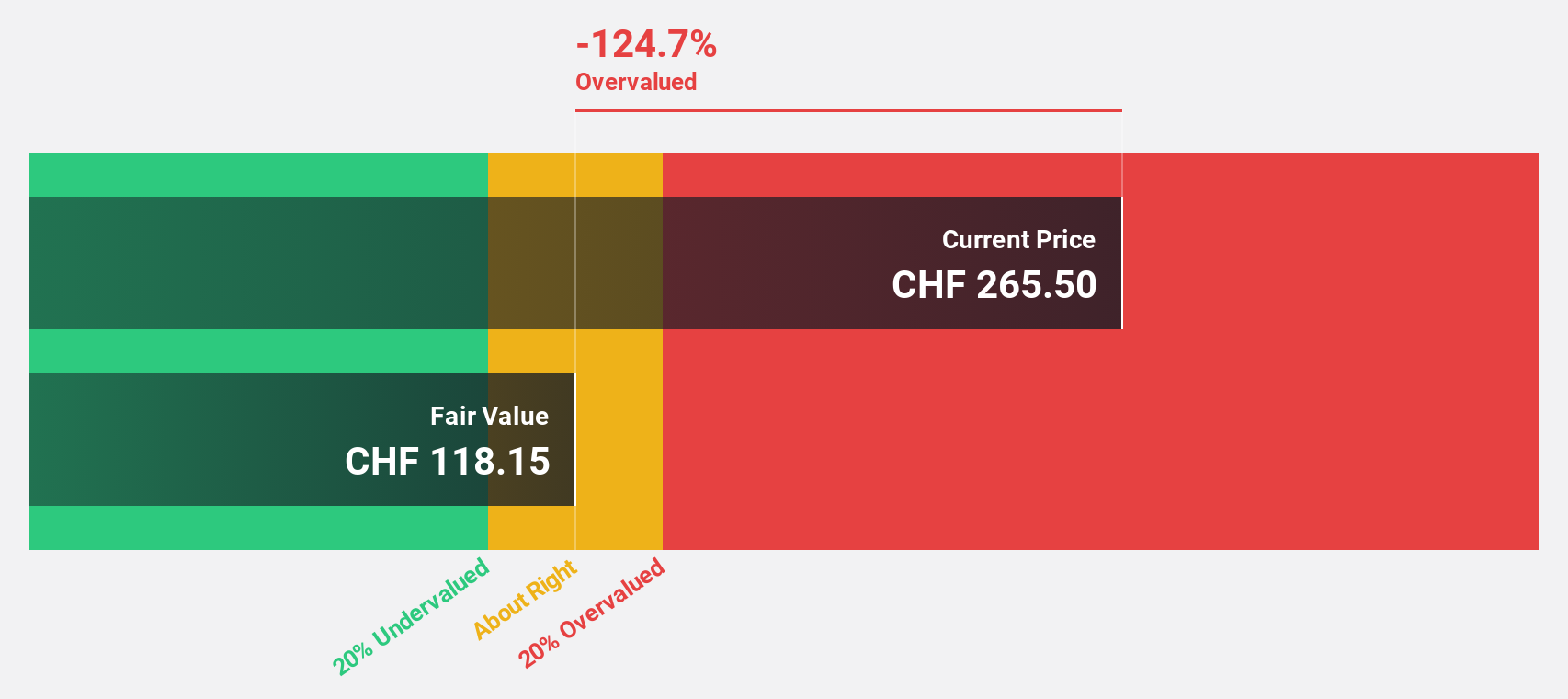

Barry Callebaut (SWX:BARN)

Overview: Barry Callebaut AG, along with its subsidiaries, manufactures and sells chocolate and cocoa products, with a market cap of CHF8.53 billion.

Operations: The company's revenue segments include Global Cocoa, contributing CHF5.31 billion, and a Segment Adjustment of CHF6.76 billion.

Estimated Discount To Fair Value: 31.9%

Barry Callebaut is trading at CHF1558, well below its estimated fair value of CHF2287.69, indicating a significant undervaluation. The company's earnings are projected to grow at 25.9% annually, surpassing the Swiss market's growth rate of 11.6%. However, its dividend yield of 1.86% isn't well covered by free cash flows and debt coverage through operating cash flow is inadequate. Despite these challenges, revenue growth remains robust compared to the market average.

- The analysis detailed in our Barry Callebaut growth report hints at robust future financial performance.

- Navigate through the intricacies of Barry Callebaut with our comprehensive financial health report here.

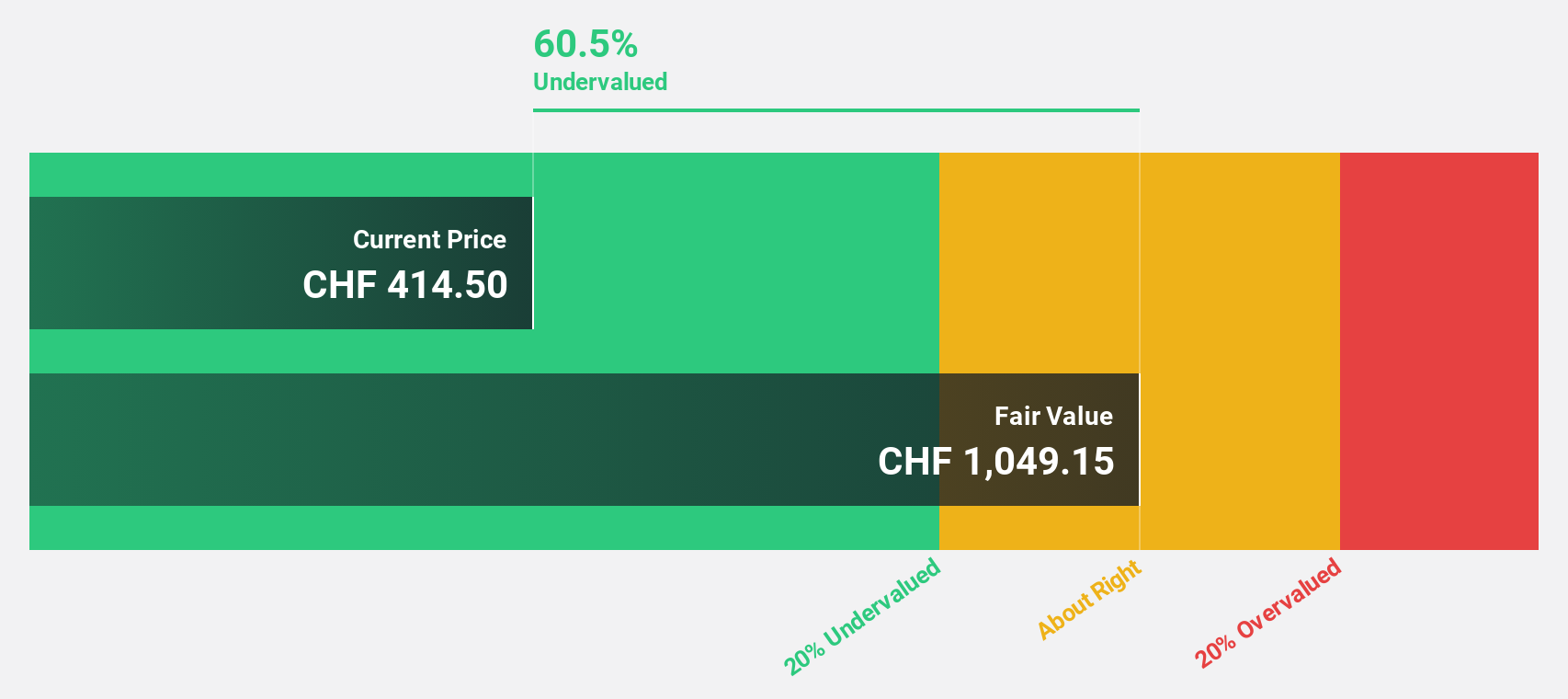

Ypsomed Holding (SWX:YPSN)

Overview: Ypsomed Holding AG, with a market cap of CHF5.58 billion, develops, manufactures, and sells injection and infusion systems for pharmaceutical and biotechnology companies through its subsidiaries.

Operations: The company's revenue is primarily derived from Ypsomed Delivery Systems, contributing CHF385.15 million, and Ypsomed Diabetes Care, which accounts for CHF151.05 million.

Estimated Discount To Fair Value: 23.5%

Ypsomed Holding is trading at CHF409, significantly below its estimated fair value of CHF534.55, highlighting undervaluation. The company's earnings are expected to grow significantly at 33.3% annually, outpacing the Swiss market's growth rate of 11.6%. Recent collaboration with Astria Therapeutics for an autoinjector could enhance future cash flows. However, Ypsomed's return on equity is forecasted to be relatively low at 17.8% in three years, warranting cautious optimism regarding long-term profitability improvements.

- According our earnings growth report, there's an indication that Ypsomed Holding might be ready to expand.

- Delve into the full analysis health report here for a deeper understanding of Ypsomed Holding.

Next Steps

- Click through to start exploring the rest of the 14 Undervalued SIX Swiss Exchange Stocks Based On Cash Flows now.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Barry Callebaut might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:BARN

Barry Callebaut

Engages in the manufacture and sale of chocolate and cocoa products.

Reasonable growth potential with adequate balance sheet and pays a dividend.