Advertisement

- Switzerland

- /

- Machinery

- /

- SWX:SUN

Sulzer Ltd (VTX:SUN) Is Going Strong But Fundamentals Appear To Be Mixed : Is There A Clear Direction For The Stock?

Most readers would already be aware that Sulzer's (VTX:SUN) stock increased significantly by 32% over the past three months. But the company's key financial indicators appear to be differing across the board and that makes us question whether or not the company's current share price momentum can be maintained. Specifically, we decided to study Sulzer's ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Sulzer

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Sulzer is:

21% = CHF230m ÷ CHF1.1b (Based on the trailing twelve months to December 2023).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each CHF1 of shareholders' capital it has, the company made CHF0.21 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Sulzer's Earnings Growth And 21% ROE

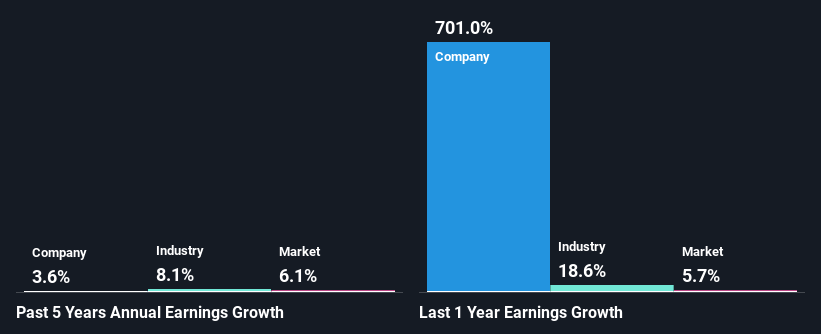

First thing first, we like that Sulzer has an impressive ROE. Even when compared to the industry average of 18% the company's ROE is pretty decent. However, for some reason, the higher returns aren't reflected in Sulzer's meagre five year net income growth average of 3.6%.Despite this, Sulzer's five year net income growth was quite low averaging at only 3.6%.Yet, Sulzer has posted measly growth of 3.6% over the past five years. This is generally not the case as when a company has a high rate of return it should usually also have a high earnings growth rate. We reckon that a low growth, when returns are quite high could be the result of certain circumstances like low earnings retention or poor allocation of capital.

Next, on comparing with the industry net income growth, we found that Sulzer's reported growth was lower than the industry growth of 8.1% over the last few years, which is not something we like to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Has the market priced in the future outlook for SUN? You can find out in our latest intrinsic value infographic research report.

Is Sulzer Efficiently Re-investing Its Profits?

Sulzer's very high three-year median payout ratio of 130% suggests that the company is paying its shareholders more than what it is earning and it definitely contributes to the low earnings growth seen by the company. That's a huge risk in our books.

Additionally, Sulzer has paid dividends over a period of nine years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to drop to 49% over the next three years. Regardless, the ROE is not expected to change much for the company despite the lower expected payout ratio.

Conclusion

In total, we're a bit ambivalent about Sulzer's performance. In spite of the high ROE, the company has failed to see growth in its earnings due to it paying out most of its profits as dividend, with almost nothing left to invest into its own business. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:SUN

Sulzer

Develops and sells products and services for fluid engineering and chemical processing applications worldwide.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor