Stock Analysis

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. In light of that, when we looked at Georg Fischer (VTX:GF) and its ROCE trend, we weren't exactly thrilled.

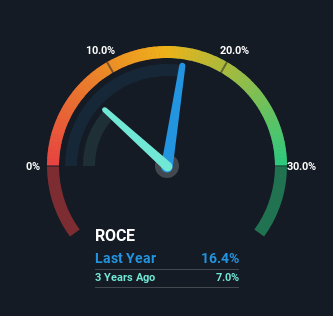

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Georg Fischer, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = CHF402m ÷ (CHF3.6b - CHF1.1b) (Based on the trailing twelve months to June 2023).

Therefore, Georg Fischer has an ROCE of 16%. That's a relatively normal return on capital, and it's around the 15% generated by the Machinery industry.

See our latest analysis for Georg Fischer

In the above chart we have measured Georg Fischer's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Georg Fischer here for free.

What The Trend Of ROCE Can Tell Us

Things have been pretty stable at Georg Fischer, with its capital employed and returns on that capital staying somewhat the same for the last five years. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. So don't be surprised if Georg Fischer doesn't end up being a multi-bagger in a few years time. With fewer investment opportunities, it makes sense that Georg Fischer has been paying out a decent 36% of its earnings to shareholders. Given the business isn't reinvesting in itself, it makes sense to distribute a portion of earnings among shareholders.

Our Take On Georg Fischer's ROCE

In a nutshell, Georg Fischer has been trudging along with the same returns from the same amount of capital over the last five years. Although the market must be expecting these trends to improve because the stock has gained 51% over the last five years. But if the trajectory of these underlying trends continue, we think the likelihood of it being a multi-bagger from here isn't high.

If you want to continue researching Georg Fischer, you might be interested to know about the 1 warning sign that our analysis has discovered.

While Georg Fischer isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're helping make it simple.

Find out whether Georg Fischer is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:GF

Georg Fischer

Georg Fischer AG engages in the provision of piping systems, and casting and machining solutions in Europe, the Americas, Asia, and internationally.

Good value average dividend payer.