Advertisement

- Switzerland

- /

- Building

- /

- SWX:GEBN

Geberit AG Just Recorded A 9.6% EPS Beat: Here's What Analysts Are Forecasting Next

It's been a pretty great week for Geberit AG (VTX:GEBN) shareholders, with its shares surging 12% to CHF550 in the week since its latest quarterly results. The result was positive overall - although revenues of CHF837m were in line with what the analysts predicted, Geberit surprised by delivering a statutory profit of CHF5.73 per share, modestly greater than expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Geberit

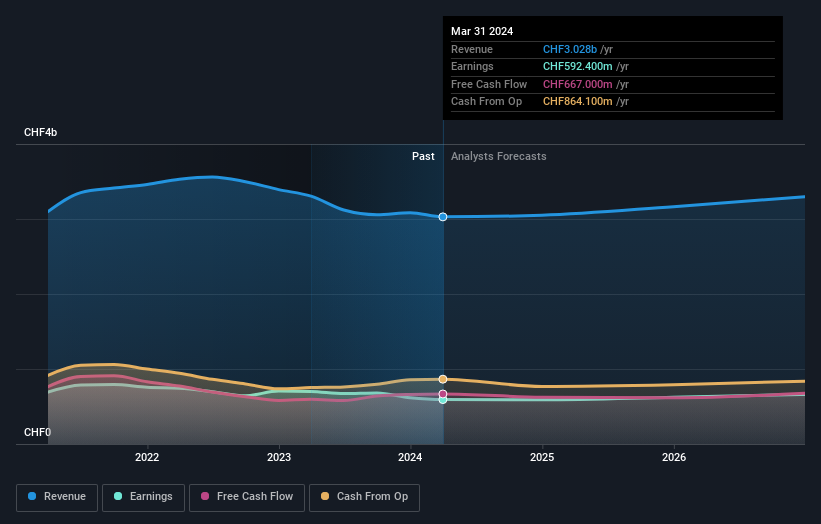

Taking into account the latest results, Geberit's 16 analysts currently expect revenues in 2024 to be CHF3.05b, approximately in line with the last 12 months. Statutory per share are forecast to be CHF17.52, approximately in line with the last 12 months. Yet prior to the latest earnings, the analysts had been anticipated revenues of CHF2.97b and earnings per share (EPS) of CHF16.64 in 2024. It looks like there's been a modest increase in sentiment following the latest results, withthe analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

Althoughthe analysts have upgraded their earnings estimates, there was no change to the consensus price target of CHF466, suggesting that the forecast performance does not have a long term impact on the company's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Geberit at CHF600 per share, while the most bearish prices it at CHF330. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Geberit shareholders.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Geberit's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 1.0% growth on an annualised basis. This is compared to a historical growth rate of 1.3% over the past five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 4.9% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Geberit.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Geberit's earnings potential next year. They also upgraded their revenue estimates for next year, even though it is expected to grow slower than the wider industry. The consensus price target held steady at CHF466, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Geberit. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Geberit going out to 2026, and you can see them free on our platform here..

It is also worth noting that we have found 1 warning sign for Geberit that you need to take into consideration.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:GEBN

Geberit

Develops, produces, and distributes sanitary products and systems for the residential and commercial construction industry.

Established dividend payer with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor