- Canada

- /

- Renewable Energy

- /

- TSX:TA

TransAlta (TSX:TA) Valuation Revisited After Centralia Extension Order and US$400 Million Senior Notes Issue

Reviewed by Simply Wall St

TransAlta (TSX:TA) has landed back on investors radar after two intertwined developments: a three month federal order keeping its Centralia Unit 2 coal plant online and a US$400 million senior note issue to bolster flexibility.

See our latest analysis for TransAlta.

Despite the headline noise around Centralia and the new senior notes, the share price has drifted to about CA$17.25, with a roughly 15 percent year to date share price decline contrasting with a still impressive five year total shareholder return near doubling. This suggests long term momentum is intact even as short term sentiment cools.

If this kind of repositioning in the power space has you thinking more broadly about opportunities, it could be worth exploring fast growing stocks with high insider ownership.

With the share price down this year but still trading at a steep discount to analyst targets and embedded growth projects, is TransAlta quietly undervalued right now, or is the market already pricing in its future upside?

Most Popular Narrative: 26.9% Undervalued

With TransAlta last closing at CA$17.25 versus a narrative fair value of about CA$23.59, the valuation hinges on some bold profit and margin shifts.

Analysts assume that profit margins will increase from -6.7% today to 9.2% in 3 years time. Analysts expect earnings to reach CA$188.9 million (and earnings per share of CA$0.38) by about September 2028, up from CA$-167.0 million today.

Want to see what drives such a dramatic swing from losses to healthy profits, even as revenue shrinks on paper? The narrative leans on a powerful margin reset, aggressive earnings rebuild, and a future valuation multiple that would turn a utility into a growth-style story. Curious how those pieces fit together, and what has to go right to justify today’s discount?

Result: Fair Value of $23.59 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, faster decarbonization mandates or weaker Alberta power prices could pressure margins, delay projects and undermine the aggressive earnings rebound included in forecasts.

Find out about the key risks to this TransAlta narrative.

Another View: Ratios Tell a Different Story

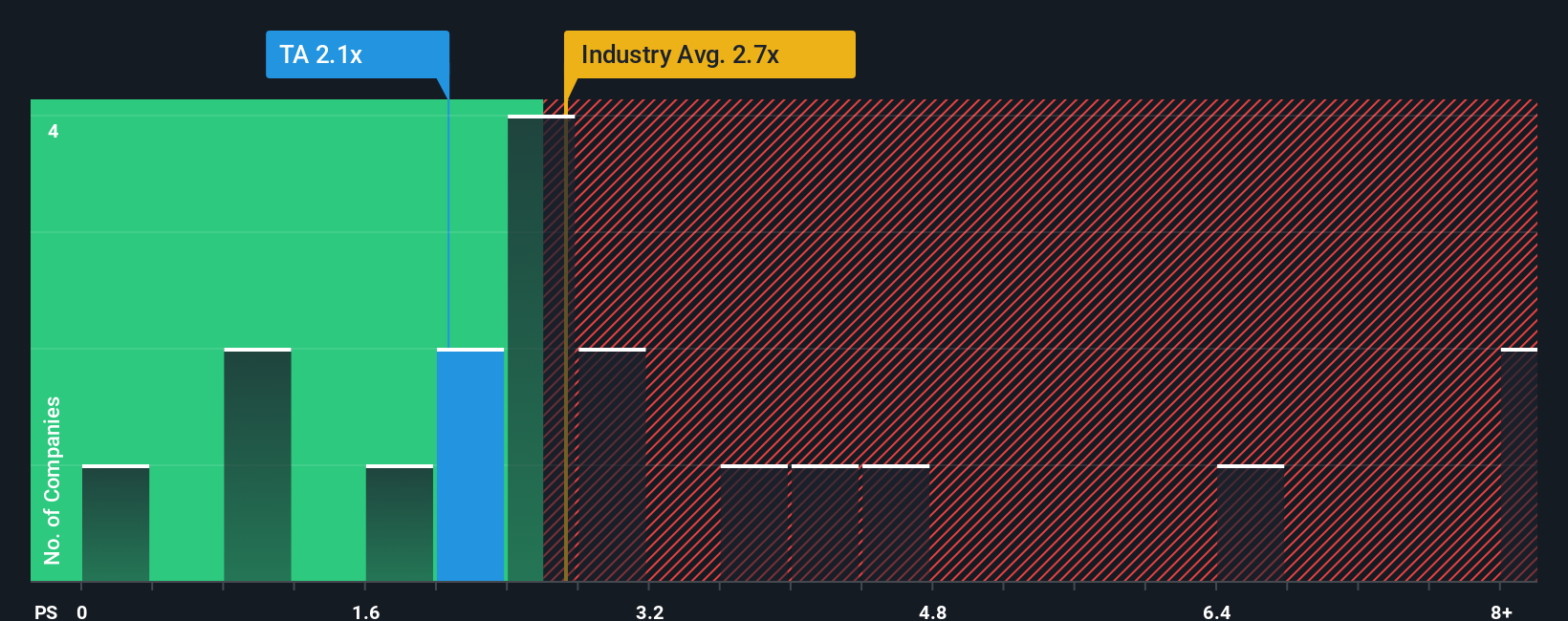

Step away from the narrative fair value and the picture gets messier. On sales, TransAlta trades at 2.1 times revenue versus a fair ratio of 1 times, even while still looking cheaper than industry and peers. Is this a margin of safety, or a value trap if growth slips?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own TransAlta Narrative

If you are not fully aligned with this perspective or want to dig into the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding TransAlta.

Looking for more investment ideas?

Consider scanning multiple opportunities so you can compare a range of setups aligned with your style, risk appetite, and long term wealth goals.

- Explore fast moving, low priced opportunities by scanning these 3624 penny stocks with strong financials that already show strong underlying financial strength instead of unstable speculation.

- Position yourself ahead of emerging technology trends by reviewing these 25 AI penny stocks that pair artificial intelligence tailwinds with attractive market entries.

- Identify potential value before it becomes widely followed by focusing on these 914 undervalued stocks based on cash flows where discounted cash flow analysis still suggests room for appreciation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if TransAlta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TA

TransAlta

Engages in the development, production, and sale of electric energy.

Good value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Q3 Outlook modestly optimistic

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion