- Canada

- /

- Renewable Energy

- /

- TSX:TA

TransAlta (TSX:TA) Ordered To Extend Coal Use While Funding Gas Shift

Reviewed by Bailey Pemberton

- The U.S. Department of Energy has ordered TransAlta to keep its Centralia Unit 2 coal plant running beyond its planned retirement.

- The order overlaps with TransAlta’s agreement to convert Centralia to natural gas under a long term tolling deal with Puget Sound Energy.

- TransAlta has completed a sizable senior notes issuance and moved to temporarily mothball Sheerness Unit 1.

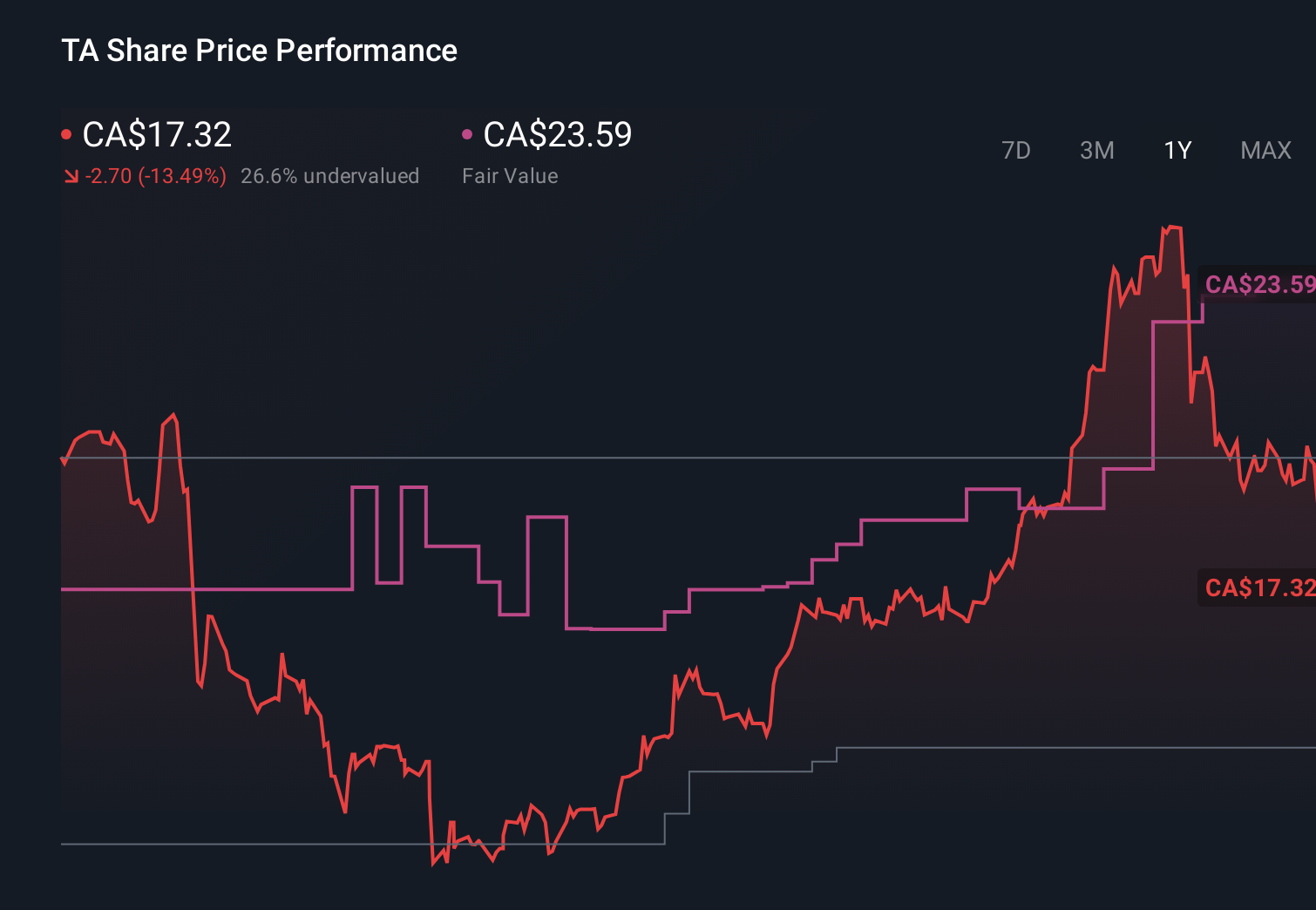

TransAlta (TSX:TA), currently trading around CA$17.245, is navigating these operational changes after a sharp pullback, with the share price down about 15.0% year to date. Despite recent weakness, the stock remains materially higher over the longer term, up roughly 53.6% over three years and 99.3% over five years, underscoring a multi year repositioning of the business.

The DOE order, Centralia conversion plans, new financing and Sheerness mothballing together frame the next phase of TransAlta’s transition strategy and risk profile. Investors will be watching how the company balances mandated coal operations, gas conversion timelines and capital allocation to sustain reliability while advancing decarbonisation goals.

Stay updated on the most important news stories for TransAlta by adding it to your watchlist or portfolio. Alternatively, explore our Community to discover new perspectives on TransAlta.

How TransAlta stacks up against its biggest competitors

The DOE order effectively asks TransAlta’s leadership to stretch its coal exit timeline at Centralia, even as it commits roughly USD 600 million to convert the unit to gas under a long dated tolling deal. This tests the team’s ability to juggle regulatory reliability demands with decarbonisation and capital discipline. Paired with the decision to mothball Sheerness Unit 1 and a US$400 million senior notes issue, this signals an active, hands on approach to portfolio pruning and balance sheet management rather than a passive run off of legacy thermal assets.

TransAlta Narrative, Leadership And Valuation

This development cuts both ways for the existing narrative that strong production and a cleaner fleet will drive upside. Short term coal exposure and incremental capex could pressure earnings, while still supporting the long term goal of repurposing Centralia into contracted, lower carbon generation. With the stock trading below an analyst fair value estimate of roughly CA$23.59 and consensus still baking in higher margins and earnings by 2028, investors will want to see leadership, including the incoming CEO, clearly articulate how these moves keep TransAlta on track with its transition and capital return plans.

Balancing Risks And Rewards In The Transition

- ⚠️ Regulatory and policy risk increases as TransAlta must comply with federal reliability mandates while coordinating state level approvals for the Centralia gas conversion.

- ⚠️ Execution risk on the USD 600 million Centralia capex and Sheerness mothballing could result in cost overruns, downtime or weaker returns than the targeted 5.5 times build multiple.

- 🎁 The long term Centralia tolling agreement and new senior notes enhance contracted cash flow visibility and funding for growth projects if leadership allocates capital prudently.

- 🎁 Optionality to return Sheerness Unit 1 to service and to leverage growing data center and electrification demand could support the earnings growth profile that underpins the current fair value narrative.

What To Watch From Here

Investors should watch how management updates guidance on Centralia timelines, Sheerness economics and balance sheet targets, and how the board and incoming CEO frame these decisions within TransAlta’s broader decarbonisation, data center and renewables strategy, which you can explore further by visiting the community narratives hub for evolving views on the stock.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if TransAlta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TA

TransAlta

Engages in the development, production, and sale of electric energy.

Good value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion