- Canada

- /

- Renewable Energy

- /

- TSX:TA

Do TransAlta’s (TSX:TA) Coal Shifts Hint At A Deeper Generation Strategy Reset?

Reviewed by Sasha Jovanovic

- In December 2025, TransAlta announced several asset changes as regulators ordered its Centralia Unit 2 coal plant in Washington State to remain available for operation for 90 days beyond its planned retirement, while its Alberta subsidiary Alberta Power (2000) Ltd. disclosed plans to temporarily mothball Sheerness Unit 1 from April 1, 2026, for up to two years.

- Together, these moves highlight how reliability concerns and shifting market conditions are reshaping TransAlta’s generation mix, influencing where capital and operational focus may be directed across its North American fleet.

- We’ll now examine how Centralia’s mandated extension, alongside the planned Sheerness mothballing, could influence TransAlta’s longer-term investment narrative.

We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

TransAlta Investment Narrative Recap

To own TransAlta, you need to believe in its ability to reposition a legacy-heavy fleet toward contracted, lower-carbon power while stabilizing earnings after a tough run of losses. The Centralia extension and Sheerness mothballing both speak to reliability and market shifts, but they do not materially change the key near term swing factor, which is whether TransAlta can secure and execute large, capital intensive transition and data center related projects without further earnings volatility.

In that context, the long term tolling agreement with Puget Sound Energy for a gas conversion of Centralia Unit 2 stands out. It ties a sizable US$600 million capital program to contracted capacity payments, which directly relates to the core catalyst of replacing merchant coal exposure with more predictable cash flows, while still leaving investors exposed to execution, regulatory and cost overrun risks during the multi year build and approval period.

Yet even with these transition projects, investors should be aware that concentrated bets on aging thermal assets and large capex plans could...

Read the full narrative on TransAlta (it's free!)

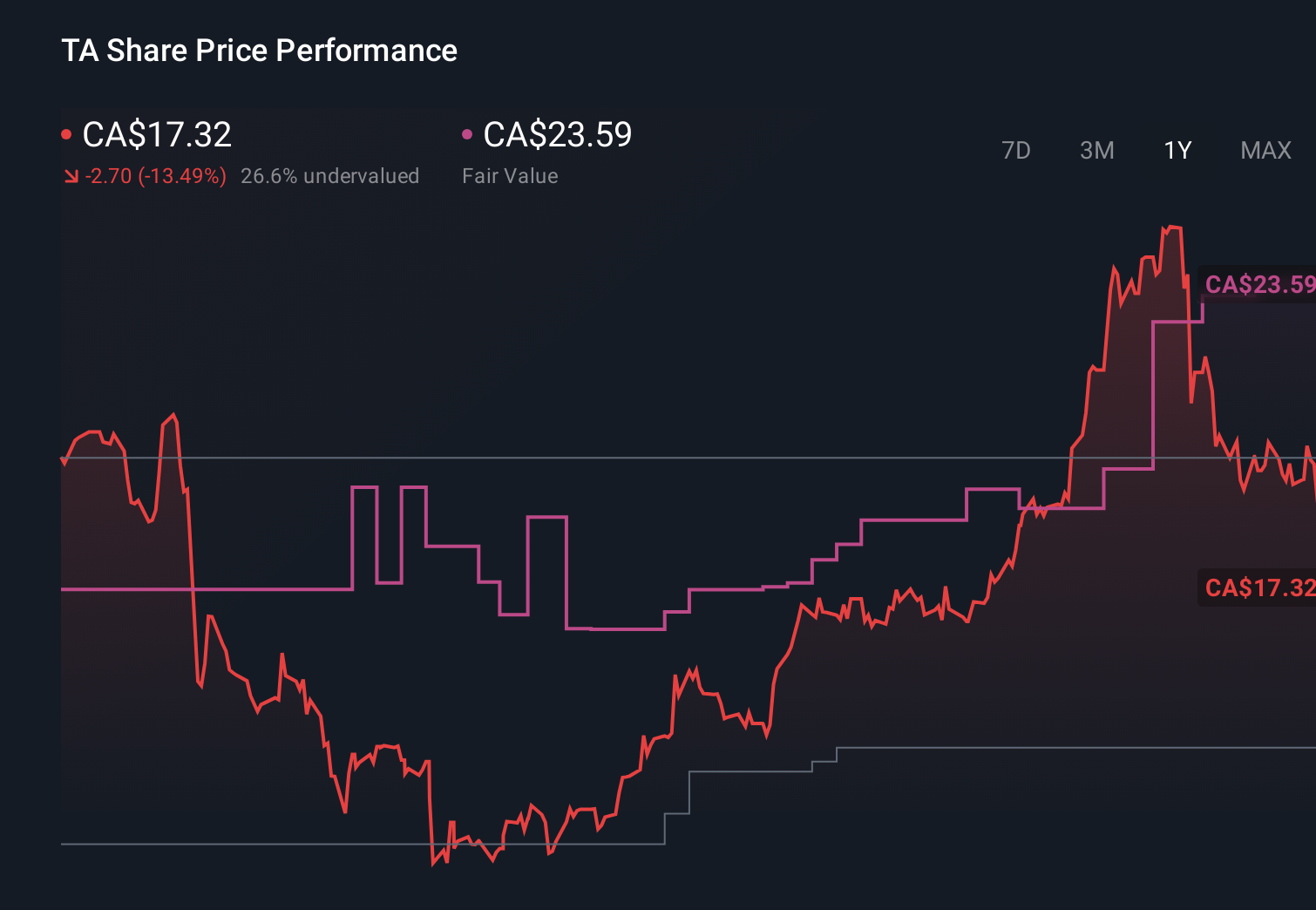

TransAlta’s narrative projects CA$2.0 billion revenue and CA$188.9 million earnings by 2028. This implies a 6.6% yearly revenue decline and an earnings increase of about CA$355.9 million from CA$-167.0 million today.

Uncover how TransAlta's forecasts yield a CA$23.59 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates for TransAlta span from C$23.59 to C$88.93, highlighting very different views on upside. You will want to weigh those opinions against the risk that aging gas and coal units could need higher sustaining capital at the same time as power prices and contracting momentum come under pressure.

Explore 2 other fair value estimates on TransAlta - why the stock might be worth just CA$23.59!

Build Your Own TransAlta Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your TransAlta research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free TransAlta research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate TransAlta's overall financial health at a glance.

Seeking Other Investments?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 34 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TransAlta might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TA

TransAlta

Engages in the development, production, and sale of electric energy.

Good value with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion