Advertisement

- Canada

- /

- Electric Utilities

- /

- TSX:EMA

Pulling back 5.8% this week, Emera's TSE:EMA) one-year decline in earnings may be coming into investors focus

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But one can do better than that by picking better than average stocks (as part of a diversified portfolio). To wit, the Emera Incorporated (TSE:EMA) share price is 24% higher than it was a year ago, much better than the market return of around 1.2% (not including dividends) in the same period. So that should have shareholders smiling. On the other hand, longer term shareholders have had a tougher run, with the stock falling 9.2% in three years.

While the stock has fallen 5.8% this week, it's worth focusing on the longer term and seeing if the stocks historical returns have been driven by the underlying fundamentals.

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

During the last year, Emera actually saw its earnings per share drop 52%.

Given the share price gain, we doubt the market is measuring progress with EPS. Indeed, when EPS is declining but the share price is up, it often means the market is considering other factors.

We note that the most recent dividend payment is higher than the payment a year ago, so that may have assisted the share price. Income-seeking investors probably helped bid up the stock price.

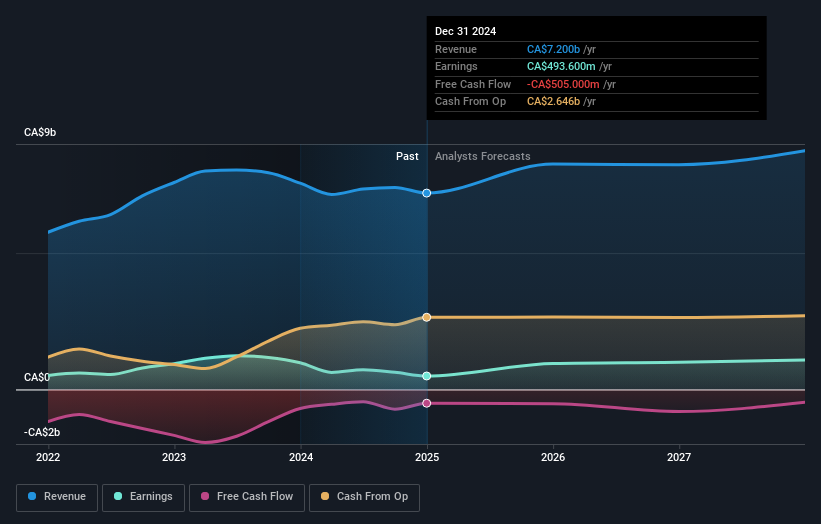

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

We like that insiders have been buying shares in the last twelve months. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. You can see what analysts are predicting for Emera in this interactive graph of future profit estimates .

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Arguably, the TSR gives a more comprehensive picture of the return generated by a stock. In the case of Emera, it has a TSR of 31% for the last 1 year. That exceeds its share price return that we previously mentioned. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

It's nice to see that Emera shareholders have received a total shareholder return of 31% over the last year. That's including the dividend. That's better than the annualised return of 7% over half a decade, implying that the company is doing better recently. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Emera better, we need to consider many other factors. For instance, we've identified 3 warning signs for Emera (2 are concerning) that you should be aware of.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of undervalued small cap companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Canadian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Emera might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:EMA

Emera

An energy and services company, invests in generation, transmission, and distribution of electricity in the United States, Canada, Barbados, and the Bahamas.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

87 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

925 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative