Stock Analysis

Exploring Undervalued Small Caps With Insider Buying In Canada July 2024

Reviewed by Simply Wall St

As the U.S. presidential campaign unfolds, key economic issues such as government debt, Federal Reserve policies, and trade relations are poised to influence market sentiment broadly, including impacts on small-cap stocks in Canada. These factors underscore the importance of selecting fundamentally strong yet undervalued small caps that exhibit insider confidence through recent buying activities.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Dundee Precious Metals | 9.0x | 3.1x | 43.72% | ★★★★★★ |

| Martinrea International | 6.0x | 0.2x | 48.44% | ★★★★★★ |

| Primaris Real Estate Investment Trust | 11.6x | 3.0x | 35.03% | ★★★★★☆ |

| Nexus Industrial REIT | 2.6x | 3.2x | 16.98% | ★★★★☆☆ |

| Calfrac Well Services | 2.5x | 0.2x | 23.11% | ★★★★☆☆ |

| Guardian Capital Group | 10.5x | 4.1x | 31.02% | ★★★★☆☆ |

| Bragg Gaming Group | NA | 1.4x | 21.15% | ★★★★☆☆ |

| Sagicor Financial | 1.2x | 0.4x | -89.31% | ★★★★☆☆ |

| Russel Metals | 9.4x | 0.5x | -9.94% | ★★★☆☆☆ |

| Freehold Royalties | 15.8x | 6.8x | 47.34% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

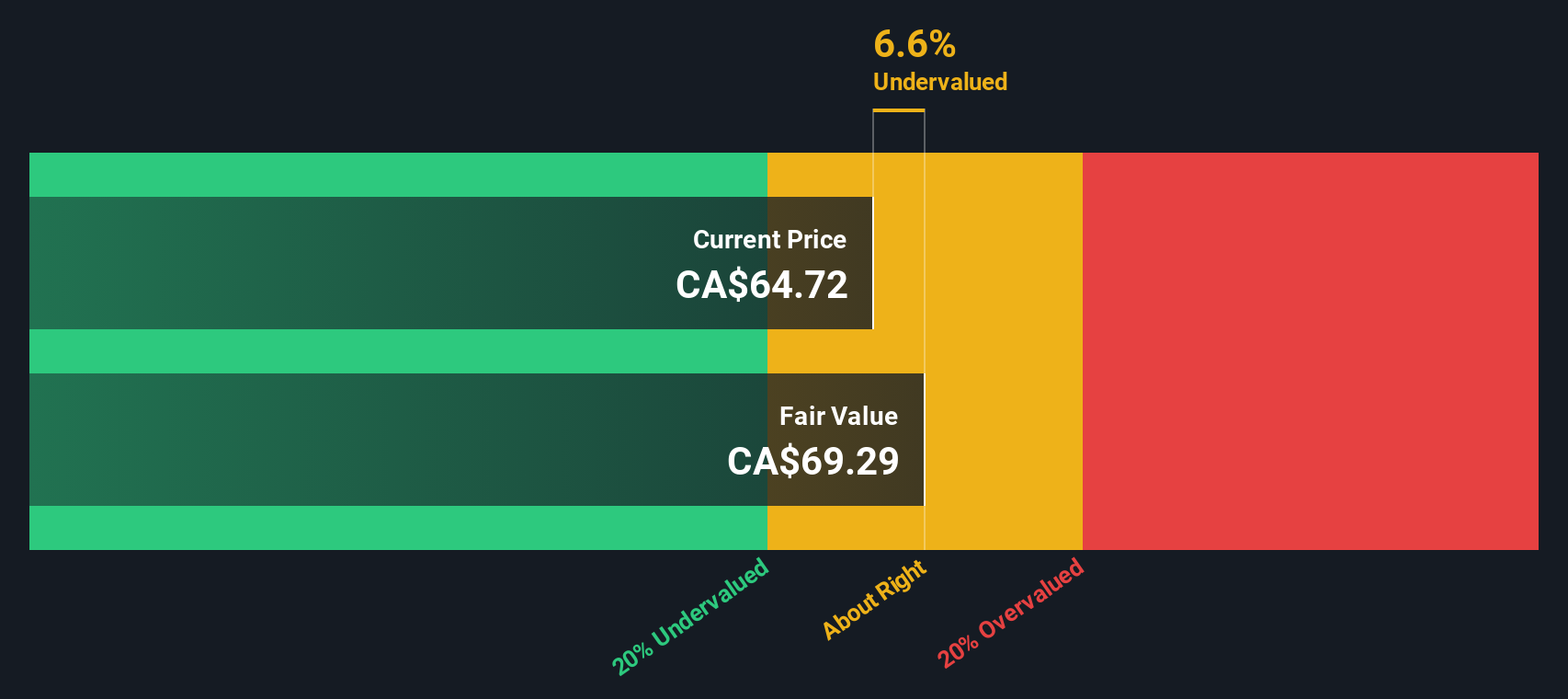

Exchange Income (TSX:EIF)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Exchange Income is a diversified company operating primarily in the manufacturing and aerospace & aviation sectors, with a market capitalization of approximately CA$1.60 billion.

Operations: Manufacturing and Aerospace & Aviation are the primary revenue segments for this entity, generating CA$1.03 billion and CA$1.54 billion respectively. The gross profit margin has shown a trend within the range of approximately 34% to 35% over recent periods, highlighting a consistent aspect of its financial health without significant fluctuations.

PE: 18.9x

Amid a challenging market, Exchange Income has demonstrated resilience with consistent dividend payments, recently affirming a monthly distribution of CA$0.22 per share. Despite a slight dip in net income from CA$6.86 million to CA$4.53 million in the first quarter of 2024, revenue growth remains robust, climbing from CA$526.84 million to CA$601.77 million year-over-year. This financial uplift is shadowed by concerns over interest coverage and shareholder dilution within the same period, underscoring mixed financial health but potential for future growth given its earnings are forecasted to grow by 22.56% annually.

- Click here and access our complete valuation analysis report to understand the dynamics of Exchange Income.

Review our historical performance report to gain insights into Exchange Income's's past performance.

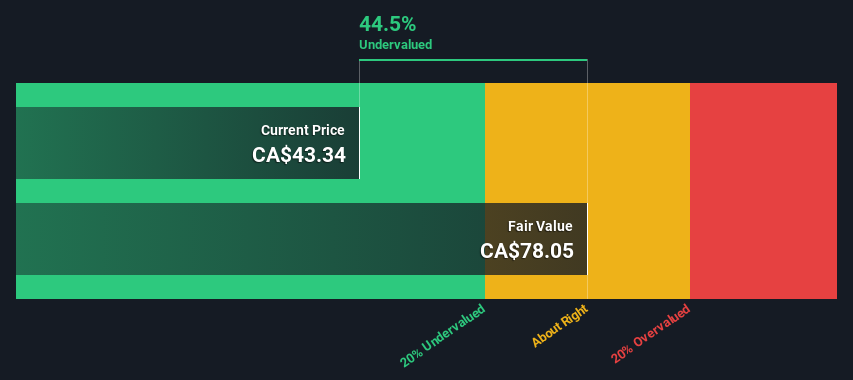

MTY Food Group (TSX:MTY)

Simply Wall St Value Rating: ★★★★☆☆

Overview: MTY Food Group is a diversified company operating primarily in the franchising, processing, distribution, and retail sectors of the food industry with a market capitalization of approximately CA$1.16 billion.

Operations: MTY Food Group generates its revenue primarily through corporate operations and franchising, with notable segments in both Canada and the US & International markets. The company's gross profit margin has shown variability over the periods reviewed, reflecting changes in cost of goods sold and operational efficiency.

PE: 11.6x

MTY Food Group, reflecting a blend of financial prudence and strategic acumen, recently disclosed a modest dip in quarterly earnings with net income sliding to CA$27.28 million from CA$30.36 million year-over-year. Despite this, their commitment to shareholder returns remains robust, evidenced by the recent dividend affirmation and a proactive share repurchase strategy where they bought back 266,700 shares for CA$12.8 million within three months. This activity not only underscores insider confidence but also hints at an intrinsic belief in the company's undervalued status amidst market fluctuations. Their financial structure is notably reliant on external borrowing, avoiding customer deposit volatility but increasing exposure to market risks.

- Click to explore a detailed breakdown of our findings in MTY Food Group's valuation report.

Examine MTY Food Group's past performance report to understand how it has performed in the past.

Russel Metals (TSX:RUS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Russel Metals is a Canadian metal distribution and processing company with operations primarily in metals service centers, energy field stores, and steel distribution, boasting a market capitalization of approximately CA$1.60 billion.

Operations: The company generates significant revenue from Metals Service Centers, contributing CA$2.95 billion, followed by Energy Field Stores and Steel Distributors with CA$982.20 million and CA$429 million respectively. Over recent periods, the firm has observed a gross profit margin of approximately 21.32%.

PE: 9.4x

Russel Metals, a notable player in the metals service center industry, recently demonstrated insider confidence with substantial share purchases. They acquired 300,000 shares for CAD 15 million in the first quarter of 2024, signaling strong belief in the company's future prospects. This move coincides with a strategic expansion through acquiring seven service centers from Samuel, Son & Co., expected to close by Q3 2024. Despite a dip in net income and sales compared to last year's figures—CAD 49.7 million and CAD 1,061.1 million respectively—the firm increased its quarterly dividend by 5%, enhancing shareholder returns amidst challenging market conditions.

- Delve into the full analysis valuation report here for a deeper understanding of Russel Metals.

Gain insights into Russel Metals' historical performance by reviewing our past performance report.

Turning Ideas Into Actions

- Explore the 32 names from our Undervalued TSX Small Caps With Insider Buying screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Exchange Income is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:EIF

Exchange Income

Engages in aerospace and aviation services and equipment, and manufacturing businesses worldwide.

Good value with moderate growth potential.