Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies ParcelPal Logistics Inc. (CSE:PKG) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for ParcelPal Logistics

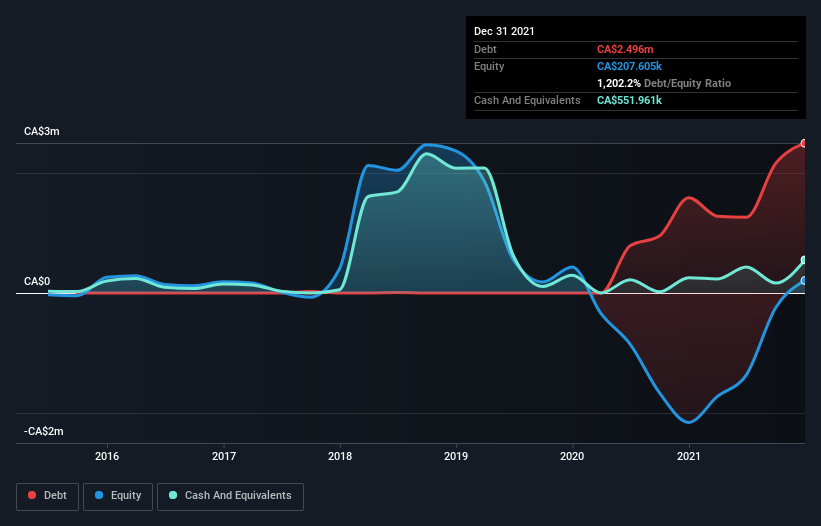

What Is ParcelPal Logistics's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2021 ParcelPal Logistics had CA$2.50m of debt, an increase on CA$1.59m, over one year. However, it does have CA$552.0k in cash offsetting this, leading to net debt of about CA$1.94m.

How Strong Is ParcelPal Logistics' Balance Sheet?

The latest balance sheet data shows that ParcelPal Logistics had liabilities of CA$4.88m due within a year, and liabilities of CA$404.9k falling due after that. Offsetting these obligations, it had cash of CA$552.0k as well as receivables valued at CA$202.1k due within 12 months. So its liabilities total CA$4.53m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of CA$5.14m, so it does suggest shareholders should keep an eye on ParcelPal Logistics' use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry. When analysing debt levels, the balance sheet is the obvious place to start. But it is ParcelPal Logistics's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year ParcelPal Logistics wasn't profitable at an EBIT level, but managed to grow its revenue by 19%, to CA$7.5m. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, ParcelPal Logistics had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping CA$3.1m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through CA$1.1m of cash over the last year. So in short it's a really risky stock. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 5 warning signs for ParcelPal Logistics (4 make us uncomfortable) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CNSX:PKG

ParcelPal Logistics

A courier and logistics company, provides last-mile delivery service and logistics solutions.

Moderate and good value.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3223.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative