TELUS (TSX:T) Launches iPhone 17 Series With Up To C$670 Trade-Up Savings

Reviewed by Simply Wall St

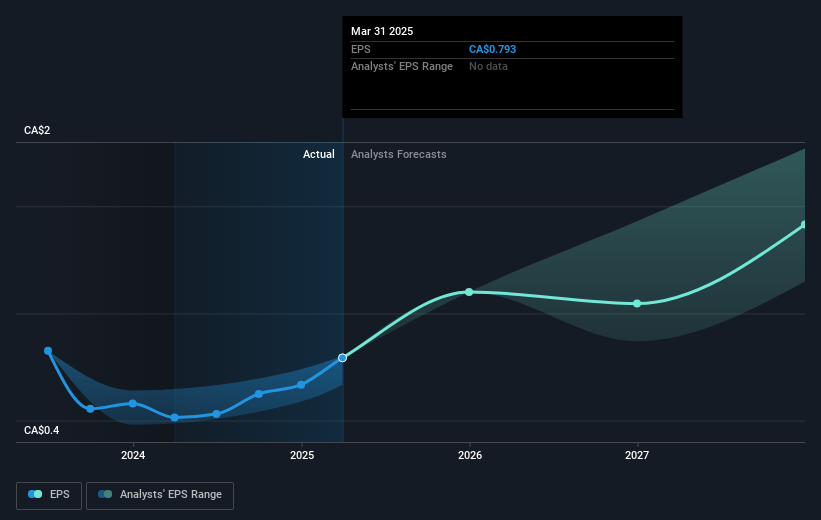

TELUS (TSX:T) recently captured attention with its announcement to offer the latest iPhone models, which may have bolstered the company's perceived value among consumers. Despite the broader market showing a weekly gain of 1.6%, TELUS's stock movement has remained relatively flat over the past quarter. This stability aligns with the mixed performance observed across major U.S. indexes where, despite some tech stocks such as Tesla soaring, other sectors demonstrated more modest gains. Events like TELUS's introduction of Wi-Fi 7 and strategic partnerships with companies like FreeTelecom could have added weight to the broader market trajectory during this period.

We've identified 3 risks for TELUS (2 are a bit unpleasant) that you should be aware of.

The introduction of the latest iPhone models by TELUS, coupled with strategic moves like Wi-Fi 7 and partnerships with FreeTelecom, positions the company to potentially boost its consumer engagement and market presence. Such initiatives could positively impact revenue and earnings projections as TELUS expands its broadband and digital health offerings. These areas are crucial for driving recurring revenues and diversifying beyond core telecom services.

Over the past five years, TELUS has achieved a total shareholder return of 24.62%, indicating moderate long-term growth. While the company has managed to surpass the Canadian Telecom industry's 1-year return of 14.3%, it has yet underperformed the Canadian market’s overall growth of 21% over the same period. This highlights both its strengths and areas where it may face challenges compared to broader market performance.

With consensus analyst price targets valuing TELUS stock at CA$23.38, the current share price of CA$22.10 suggests a modest discount. This slight undervaluation implies potential for upward movement should TELUS successfully capitalize on current initiatives and meet growth expectations. However, as the target reflects only a small premium over the present share price, investors and analysts consider TELUS fairly priced, assuming consistent operational performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TELUS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:T

TELUS

Provides a range of telecommunications and information technology products and services in Canada.

Average dividend payer and fair value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion