Pivotree Inc. (CVE:PVT) Just Reported And Analysts Have Been Cutting Their Estimates

It's been a mediocre week for Pivotree Inc. (CVE:PVT) shareholders, with the stock dropping 11% to CA$7.95 in the week since its latest annual results. It was a pretty bad result overall; while revenues were in line with expectations at CA$64m, statutory losses exploded to CA$0.57 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

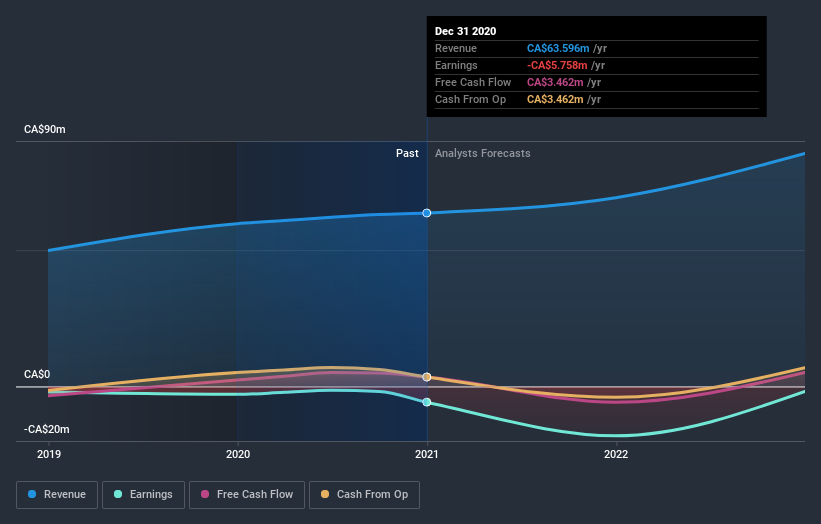

See our latest analysis for Pivotree

Taking into account the latest results, the most recent consensus for Pivotree from five analysts is for revenues of CA$69.2m in 2021 which, if met, would be a meaningful 8.9% increase on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 28% (on a statutory basis) to CA$0.73. In the lead-up to this report, the analysts had been modelling revenues of CA$76.4m and earnings per share (EPS) of CA$0.02 in 2021. The analysts have made an abrupt about-face on Pivotree, administering a small dip in to revenue forecasts and slashing the earnings outlook from a profit to loss.

The consensus price target fell 11% to CA$13.00, with the analysts clearly concerned about the company following the weaker revenue and earnings outlook. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Pivotree, with the most bullish analyst valuing it at CA$15.00 and the most bearish at CA$10.75 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Pivotree's past performance and to peers in the same industry. The analysts are definitely expecting Pivotree's growth to accelerate, with the forecast 8.9% annualised growth to the end of 2021 ranking favourably alongside historical growth of 6.5% per annum over the past year. Compare this with other companies in the same industry, which are forecast to grow their revenue 9.9% annually. Pivotree is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The biggest low-light for us was that the forecasts for Pivotree dropped from profits to a loss next year. They also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Pivotree going out to 2022, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Pivotree that you should be aware of.

If you decide to trade Pivotree, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:PVT

Pivotree

Designs, integrates, deploys, and manages digital platforms in commerce, data management, and supply chain for retail and branded manufacturers worldwide.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion