Advertisement

Bullish: Analysts Just Made A Neat Upgrade To Their Converge Technology Solutions Corp. (CVE:CTS) Forecasts

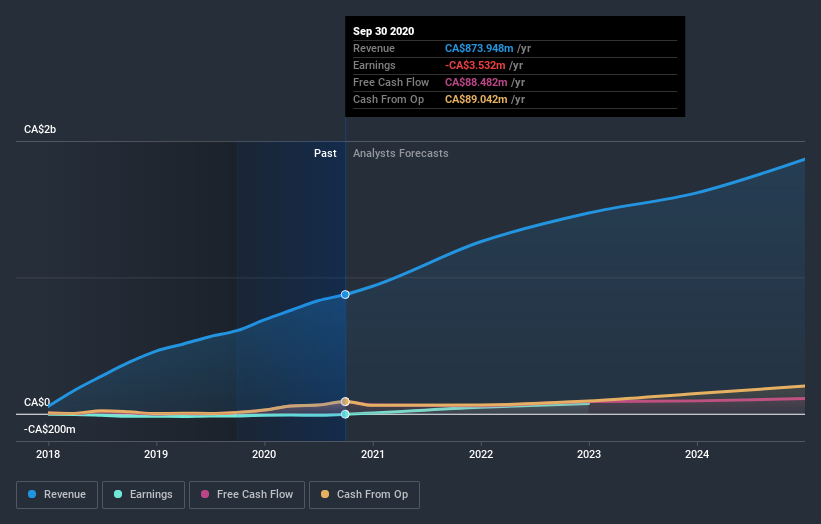

Celebrations may be in order for Converge Technology Solutions Corp. (CVE:CTS) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

After this upgrade, Converge Technology Solutions' six analysts are now forecasting revenues of CA$1.3b in 2021. This would be a sizeable 46% improvement in sales compared to the last 12 months. Losses are expected to turn into profits real soon, with the analysts forecasting CA$0.33 in per-share earnings. Prior to this update, the analysts had been forecasting revenues of CA$1.2b and earnings per share (EPS) of CA$0.29 in 2021. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

See our latest analysis for Converge Technology Solutions

With these upgrades, we're not surprised to see that the analysts have lifted their price target 26% to CA$6.11 per share. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values Converge Technology Solutions at CA$6.75 per share, while the most bearish prices it at CA$4.90. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. Next year brings more of the same, according to the analysts, with revenue forecast to grow 46%, in line with its 55% annual growth over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 9.1% per year. So although Converge Technology Solutions is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for next year, expecting improving business conditions. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, Converge Technology Solutions could be worth investigating further.

These earnings upgrades look like a sterling endorsement, but before diving in - you should know that we've spotted 2 potential risk with Converge Technology Solutions, including major dilution from new stock issuance in the past year. For more information, you can click through to our platform to learn more about this and the 1 other risk we've identified .

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

When trading Converge Technology Solutions or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:CTS

Converge Technology Solutions

Provides software-enabled IT and cloud solutions in the United States, Canada, Germany, rest of Europe, the United Kingdom, and Ireland.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|66.7% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|4.8% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor