Earnings Surge and Doubling EPS Could Be a Game Changer for Kinaxis (TSX:KXS)

Reviewed by Sasha Jovanovic

- Kinaxis Inc. reported third quarter and nine-month earnings for 2025, showing sales of US$134.59 million and US$403.8 million, and net income of US$16.85 million and US$51.2 million, both well above the comparable periods a year earlier.

- This strong earnings report also revealed that Kinaxis' basic earnings per share from continuing operations more than doubled year-over-year for both the quarter and year-to-date periods.

- We'll examine how the significant jump in net income impacts Kinaxis' investment narrative and its outlook on profitability and growth.

Find companies with promising cash flow potential yet trading below their fair value.

Kinaxis Investment Narrative Recap

To be a Kinaxis shareholder, you need to believe that demand for AI-first, cloud-based supply chain platforms will keep rising, and that Kinaxis can differentiate itself compared to larger, established competitors. The recent earnings beat strengthens confidence in the short-term profitability story, but it does not materially shift the biggest risk: whether Kinaxis can maintain its unique value as enterprise customers develop their own AI solutions or seek lower-cost competitors.

Of the recent company announcements, the launch of Maestro Agents in October 2025 stands out as most relevant. This suite of AI-driven tools could further bolster Kinaxis’ competitive position by delivering meaningful improvements in supply chain decision-making, supporting the main catalysts for growth identified by analysts and underpinning the encouraging earnings momentum.

Yet, investors should be aware that, despite strong earnings, growing competition from open-source and in-house AI platforms poses a risk to Kinaxis’ future pricing power and market share...

Read the full narrative on Kinaxis (it's free!)

Kinaxis' narrative projects $742.1 million revenue and $115.9 million earnings by 2028. This requires 13.0% yearly revenue growth and a $91.1 million earnings increase from $24.8 million.

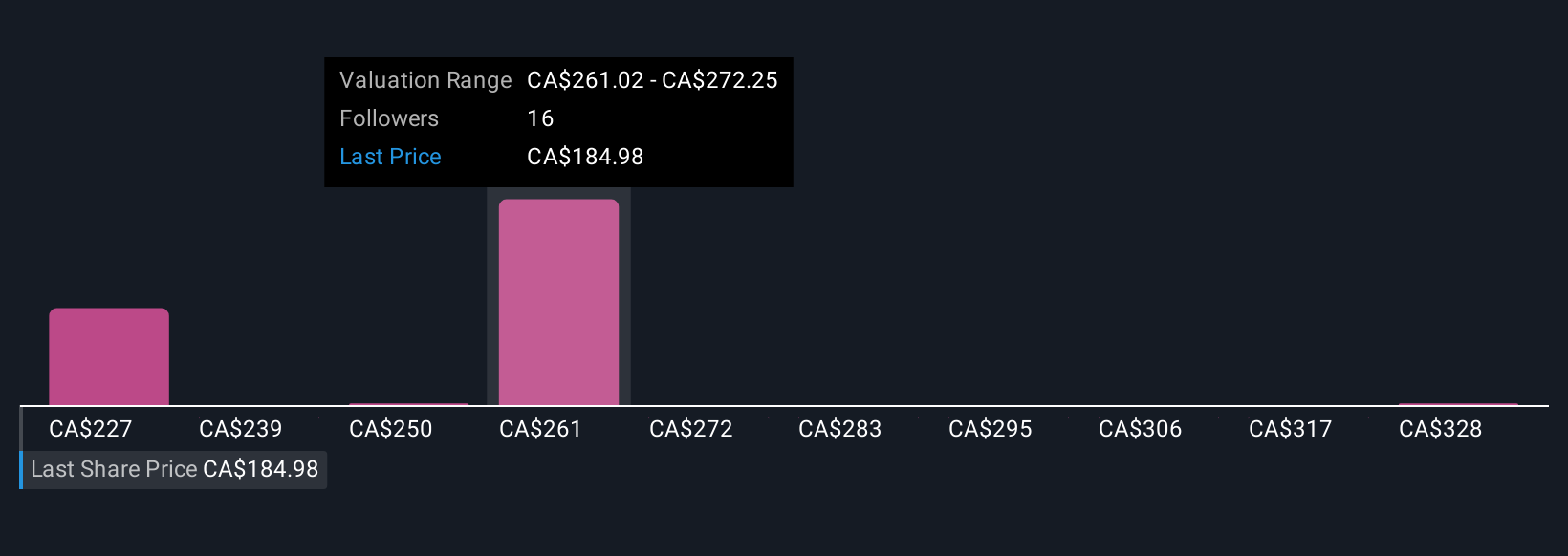

Uncover how Kinaxis' forecasts yield a CA$227.33 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Four private investors in the Simply Wall St Community estimate Kinaxis’ fair value between US$227.33 and US$339.62. As you consider these diverse views, remember that competition from open-source and in-house AI solutions may affect Kinaxis’ long-term margins and growth.

Explore 4 other fair value estimates on Kinaxis - why the stock might be worth as much as 99% more than the current price!

Build Your Own Kinaxis Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kinaxis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Kinaxis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kinaxis' overall financial health at a glance.

No Opportunity In Kinaxis?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- We've found 20 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kinaxis might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:KXS

Kinaxis

Provides cloud-based subscription software for supply chain operations in the United States, Europe, Asia, and Canada.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion