Advertisement

Here's Why We're Not Too Worried About Captor Capital's (CSE:CPTR) Cash Burn Situation

Just because a business does not make any money, does not mean that the stock will go down. For example, Captor Capital (CSE:CPTR) shareholders have done very well over the last year, with the share price soaring by 256%. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

In light of its strong share price run, we think now is a good time to investigate how risky Captor Capital's cash burn is. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Captor Capital

When Might Captor Capital Run Out Of Money?

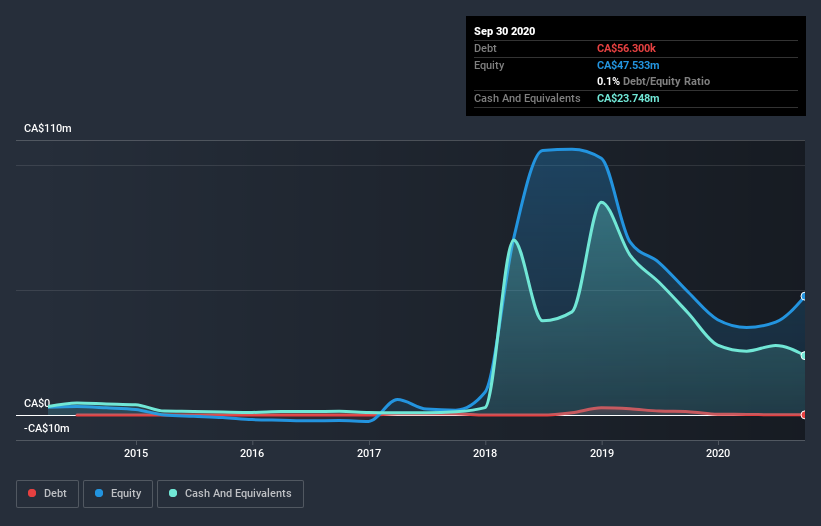

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at September 2020, Captor Capital had cash of CA$24m and such minimal debt that we can ignore it for the purposes of this analysis. In the last year, its cash burn was CA$9.1m. That means it had a cash runway of about 2.6 years as of September 2020. That's decent, giving the company a couple years to develop its business. The image below shows how its cash balance has been changing over the last few years.

Is Captor Capital's Revenue Growing?

We're hesitant to extrapolate on the recent trend to assess its cash burn, because Captor Capital actually had positive free cash flow last year, so operating revenue growth is probably our best bet to measure, right now. While it's not that amazing, we still think that the 5.6% increase in revenue from operations was a positive. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how Captor Capital is building its business over time.

How Hard Would It Be For Captor Capital To Raise More Cash For Growth?

Notwithstanding Captor Capital's revenue growth, it is still important to consider how it could raise more money, if it needs to. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Captor Capital's cash burn of CA$9.1m is about 31% of its CA$30m market capitalisation. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

So, Should We Worry About Captor Capital's Cash Burn?

On this analysis of Captor Capital's cash burn, we think its cash runway was reassuring, while its cash burn relative to its market cap has us a bit worried. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. On another note, we conducted an in-depth investigation of the company, and identified 3 warning signs for Captor Capital (1 is a bit concerning!) that you should be aware of before investing here.

Of course Captor Capital may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Captor Capital or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CNSX:CPTR

Captor Capital

Engages in the retail sale of cannabis products in the United States.

Excellent balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor