Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:SOMA

Soma Gold (TSXV:SOMA) Profit Margin Drops as Q3 Net Income Falls to $0.42 Million

Simply Wall St

Reviewed by Simply Wall St

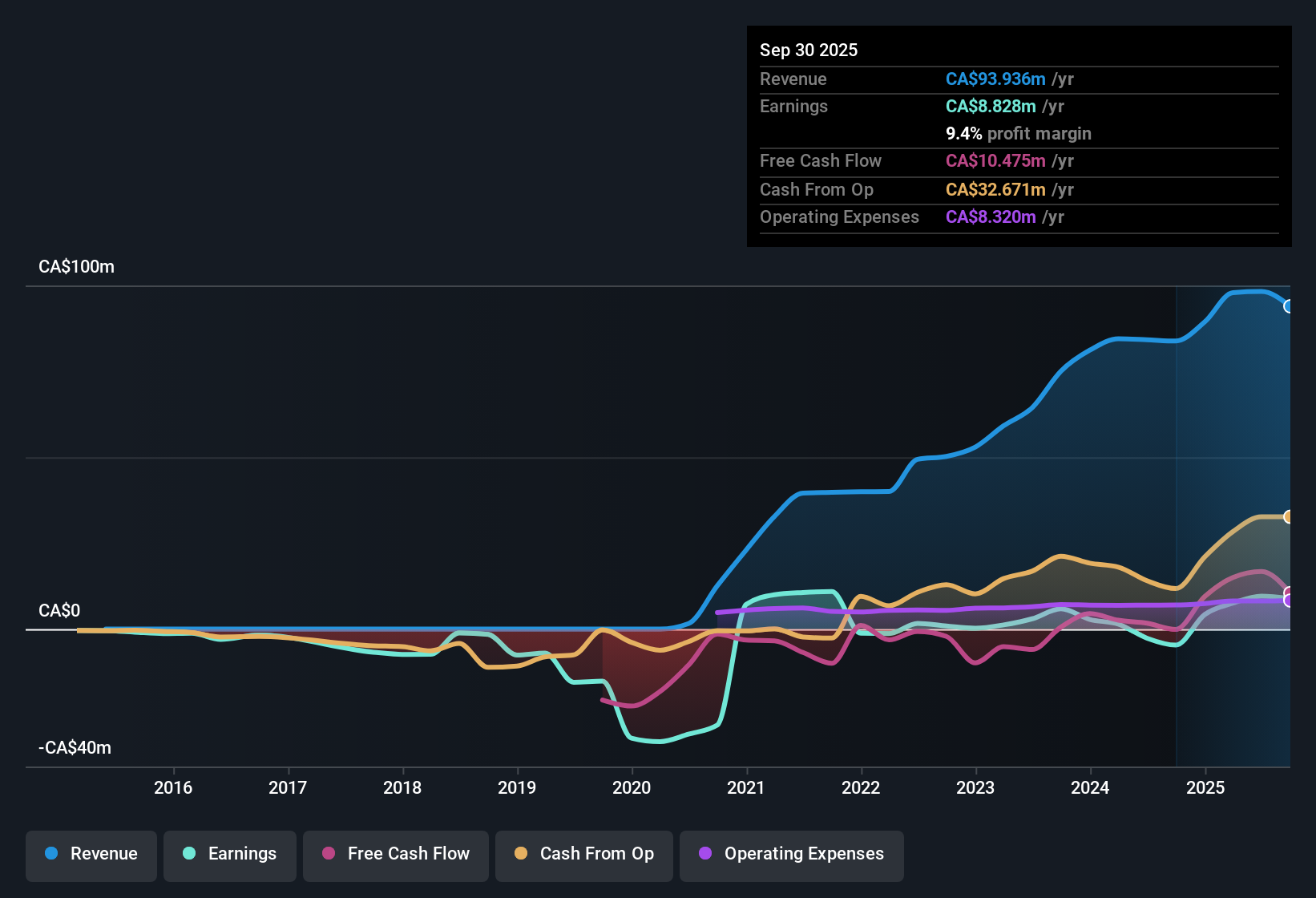

Soma Gold (TSXV:SOMA) has posted its Q3 2025 results, reporting total revenue of $18.1 million, basic EPS of $0.0041 CAD, and net income of $0.42 million for the quarter. The company has seen revenue fluctuate over recent periods, with the past two quarters at $23.0 million and $27.9 million respectively. Basic EPS also shifted from $0.0172 CAD and $0.0344 CAD in Q2 and Q1 2025. Margins delivered a mixed picture this quarter, setting the stage for investors to weigh the quarter's dynamics in the context of a rapidly evolving profit story.

See our full analysis for Soma Gold.Next, we’ll see how these headline results measure up against ongoing market narratives and what they might mean for the stock's big-picture outlook.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Recovery Faces Near-Term Pressure

- Trailing twelve month net income reached $8.8 million, capping a return to profitability after an extended period of mixed results in prior years.

- Recent profitability heavily supports the view that Soma Gold’s operational turnaround is real and not just a one-off, with

- $3.2 million in net income in Q1 2025 outpacing the latest Q3 read of $0.42 million. This suggests positive, but patchy trends rather than steady quarterly growth.

- Analysts highlight the company’s 22.1% five-year earnings growth rate as a sign of underlying business quality. This may help the company weather momentary dips.

Valuation Discount Versus Peers

- Soma Gold trades at a Price-To-Earnings ratio of 21.4x, well above its peer group average of 6.8x. Its share price of $1.61 is roughly 70.3% below the DCF fair value estimate of $5.41.

- What is surprising is the valuation disconnect. Some investors point to the fair value discount as a core bullish argument, but

- Peers and the broader Canadian metals/mining industry both post lower multiples. This raises questions about whether recent earnings quality fully warrants the stock’s premium valuation.

- The consensus narrative notes valuation-focused investors will need to weigh the discounted share price against the above-average P/E and sector positioning when sizing up upside potential.

Shareholder Dilution Colors the Comeback

- While the past year saw Soma Gold become profitable, shareholders faced new dilution. The overall share count rose to support capital needs despite earnings growth.

- Critics highlight that although the quality of earnings improved, the dilution risk tempers total per-share gains, as

- The higher share count may partly explain modest basic EPS figures, which dipped to $0.0041 CAD in Q3 2025 from $0.0172 CAD and $0.0344 CAD just two quarters prior.

- The relatively expensive P/E multiple coupled with dilution means recent profitability may not fully translate to shareholder value unless future earnings growth accelerates.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Soma Gold's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Soma Gold’s inconsistent quarterly earnings and recent shareholder dilution raise doubts about reliable growth and the sustainability of its profitability trend.

For a portfolio with more dependable results, check out stable growth stocks screener (2076 results) to discover companies consistently delivering steady earnings and revenue, even when the market shifts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:SOMA

Soma Gold

A natural resource company, engages in the acquisition, exploration, and development of mineral properties in Columbia.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

933 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative