Stock Analysis

- Canada

- /

- Metals and Mining

- /

- TSXV:ATC

We Think ATAC Resources (CVE:ATC) Can Easily Afford To Drive Business Growth

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should ATAC Resources (CVE:ATC) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

View our latest analysis for ATAC Resources

When Might ATAC Resources Run Out Of Money?

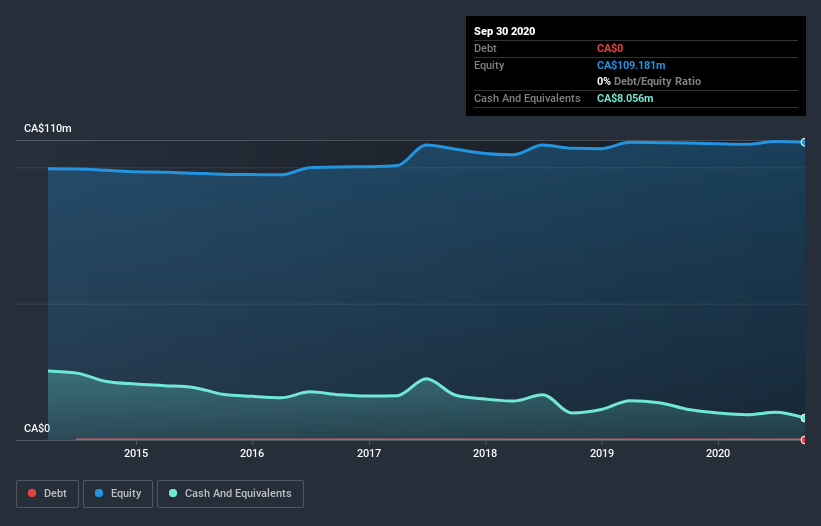

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at September 2020, ATAC Resources had cash of CA$8.1m and no debt. Importantly, its cash burn was CA$1.1m over the trailing twelve months. Therefore, from September 2020 it had 7.4 years of cash runway. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. The image below shows how its cash balance has been changing over the last few years.

Can ATAC Resources Raise More Cash Easily?

Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

ATAC Resources has a market capitalisation of CA$28m and burnt through CA$1.1m last year, which is 3.8% of the company's market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About ATAC Resources' Cash Burn?

Given it's an early stage company, we don't have a lot of data with which to judge ATAC Resources' cash burn. We would undoubtedly be more comfortable if it had reported some operating revenue. However, it is fair to say that its cash runway gave us comfort. Summing up, its cash burn doesn't bother us and we're excited to see what kind of growth it can achieve with its current cash hoard. Separately, we looked at different risks affecting the company and spotted 4 warning signs for ATAC Resources (of which 1 can't be ignored!) you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you decide to trade ATAC Resources, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether ATAC Resources is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:ATC

ATAC Resources

ATAC Resources Ltd., an exploration stage company, engages in the acquisition, exploration, and evaluation of mineral properties in Canada and the and United States.

Adequate balance sheet and overvalued.