- Canada

- /

- Metals and Mining

- /

- TSX:SXGC

Southern Cross Gold (TSX:SXGC): Assessing Valuation After a Strong 175% Year-to-Date Share Price Rally

Reviewed by Simply Wall St

Southern Cross Gold Consolidated (TSX:SXGC) has quietly turned into one of the stronger movers on the TSX, with the stock up about 6% today and roughly 25% over the past month.

See our latest analysis for Southern Cross Gold Consolidated.

With the share price now at CA$8.84 and a year to date share price return of about 175%, the recent 30 day share price return of roughly 25% suggests momentum is still building as investors warm to its exploration story and risk profile.

If you are looking beyond a single explorer, this could be a handy moment to scout other resource names and discover fast growing stocks with high insider ownership.

With the stock now trading almost exactly in line with analyst targets and up sharply year to date, should investors view Southern Cross Gold Consolidated as undervalued today, or is the market already pricing in its future growth?

Price to Book of 9.4x: Is It Justified?

Based on its latest close at CA$8.84, Southern Cross Gold Consolidated looks expensive on a price to book basis compared to both peers and the wider Canadian metals and mining industry.

The price to book ratio compares the market value of the company to its net assets. This measure is often used for asset heavy, early stage resource names where traditional earnings metrics are less meaningful. For SXGC, a 9.4x multiple suggests investors are paying a substantial premium over the company’s current book value.

That premium stands out when set against the Canadian metals and mining industry average of 2.7x and an already elevated peer average of 7.9x. In both cases, SXGC trades at a richer valuation, implying the market is baking in stronger exploration success or future resource definition than is reflected in today’s balance sheet.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to book of 9.4x (OVERVALUED)

However, investors should remember that exploration outcomes and permitting timelines remain uncertain, and any drilling disappointment or regulatory setback could quickly cool current enthusiasm.

Find out about the key risks to this Southern Cross Gold Consolidated narrative.

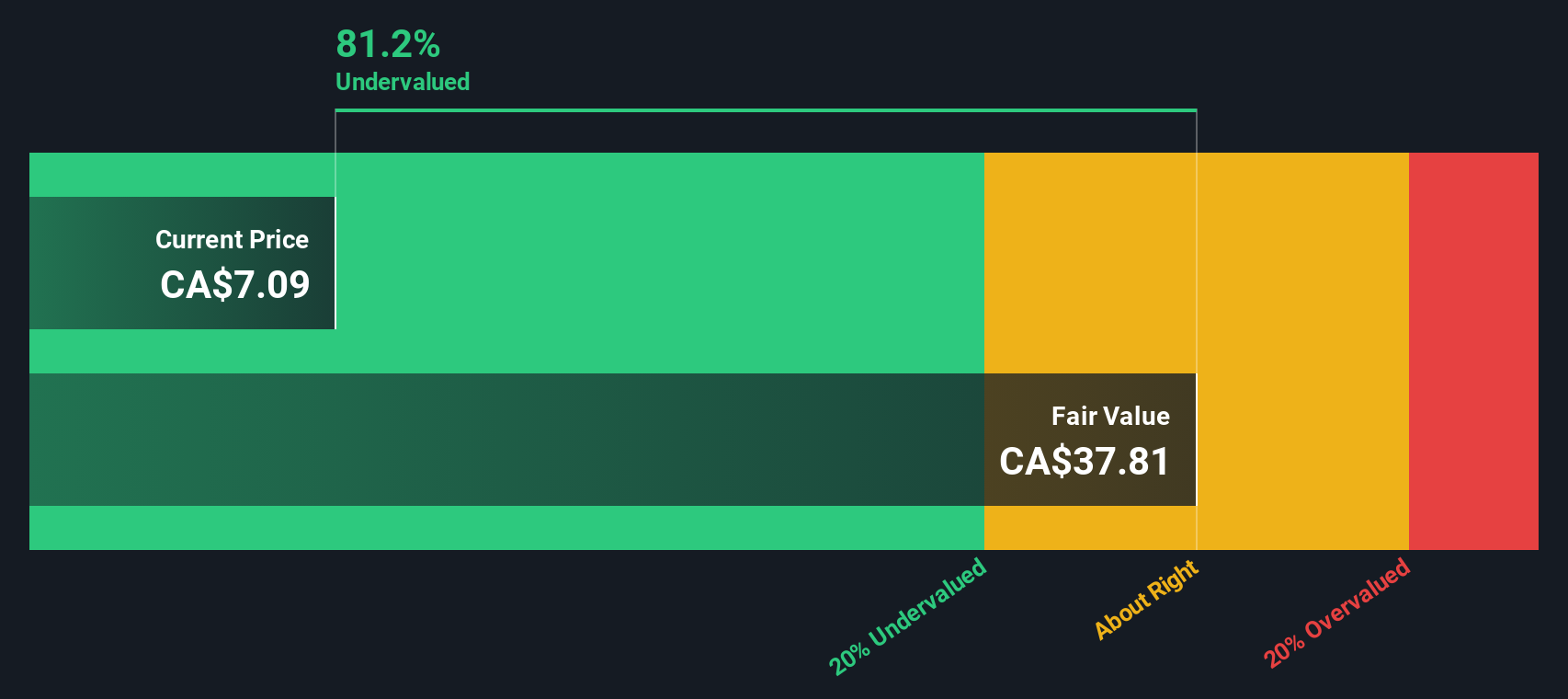

Another Angle: Our DCF Fair Value

While the price to book suggests SXGC looks expensive, our DCF model tells a very different story, implying the shares trade about 90% below an estimated fair value of roughly CA$91. That is a large gap, but it raises an important question: is it a potential opportunity, or a sign that expectations are too aggressive?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Southern Cross Gold Consolidated for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Southern Cross Gold Consolidated Narrative

If you would rather dig into the numbers yourself and challenge these assumptions, you can build a personalised view in just a few minutes: Do it your way.

A great starting point for your Southern Cross Gold Consolidated research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for your next investing edge?

Before the market moves on without you, use the Simply Wall St Screener to pinpoint fresh opportunities that match your strategy and sharpen your portfolio positioning.

- Capture powerful cash flow bargains by scanning these 917 undervalued stocks based on cash flows that the broader market may still be overlooking.

- Tap into next generation innovation by targeting these 24 AI penny stocks positioned to benefit from accelerating adoption of artificial intelligence.

- Build a resilient income stream by focusing on these 13 dividend stocks with yields > 3% that can potentially strengthen long term total returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SXGC

Southern Cross Gold Consolidated

Engages in the acquisition and exploration of precious and energy mineral interests in Australia.

Flawless balance sheet and slightly overvalued.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion