Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:SSL

A Fresh Look at Sandstorm Gold (TSX:SSL) Valuation After Sustained Outperformance

Simply Wall St

Reviewed by Kshitija Bhandaru

Sandstorm Gold (TSX:SSL) shares have seen movement recently, with investors keeping a close eye on its performance. The company’s returns over the past month and the past 3 months offer some interesting signals about how sentiment is shifting.

See our latest analysis for Sandstorm Gold.

Zooming out, Sandstorm Gold’s 1-year total shareholder return has soared over 100%, firmly outpacing most of its sector. This sustained rally, with momentum building over the past quarter, hints at growing investor confidence in both its assets and outlook, particularly with the recent 30-day share price return continuing to show strength.

If recent gold rallies have sparked your curiosity, now is the perfect time to discover other fast-growing companies with strong insider backing. Explore fast growing stocks with high insider ownership.

But with the stock trading close to analyst targets and recent growth already rewarded by the market, investors face a crucial question: is Sandstorm Gold currently undervalued, or has the market already priced in future gains?

Most Popular Narrative: 6.7% Undervalued

Based on the most-followed narrative, Sandstorm Gold’s fair value estimate stands just above the latest close, hinting at modest undervaluation. The story behind that number centers on ambitious projections for production and efficiency gains, setting the stage for what comes next.

The completion of transformational projects like Glencore's MARA mine and Rio Tinto's development on the Entree joint venture grounds at Oyu Tolgoi could significantly enhance Sandstorm's revenue stream in the coming years. Initiatives to increase throughput and optimize operations at existing mines like Fruta del Norte and Chapada can lead to better production efficiency, potentially enhancing operational margins.

Wonder what factors drive that premium? The narrative banks on accelerating profit margins, bold operational upgrades, and a future earnings trajectory that rivals the sector’s heavyweights. Uncover which assumptions power this surprising upside and see what could shift the entire outlook.

Result: Fair Value of $18.26 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, setbacks at key mines or lower than expected gold output could quickly challenge this optimistic picture and shift the narrative for investors.

Find out about the key risks to this Sandstorm Gold narrative.

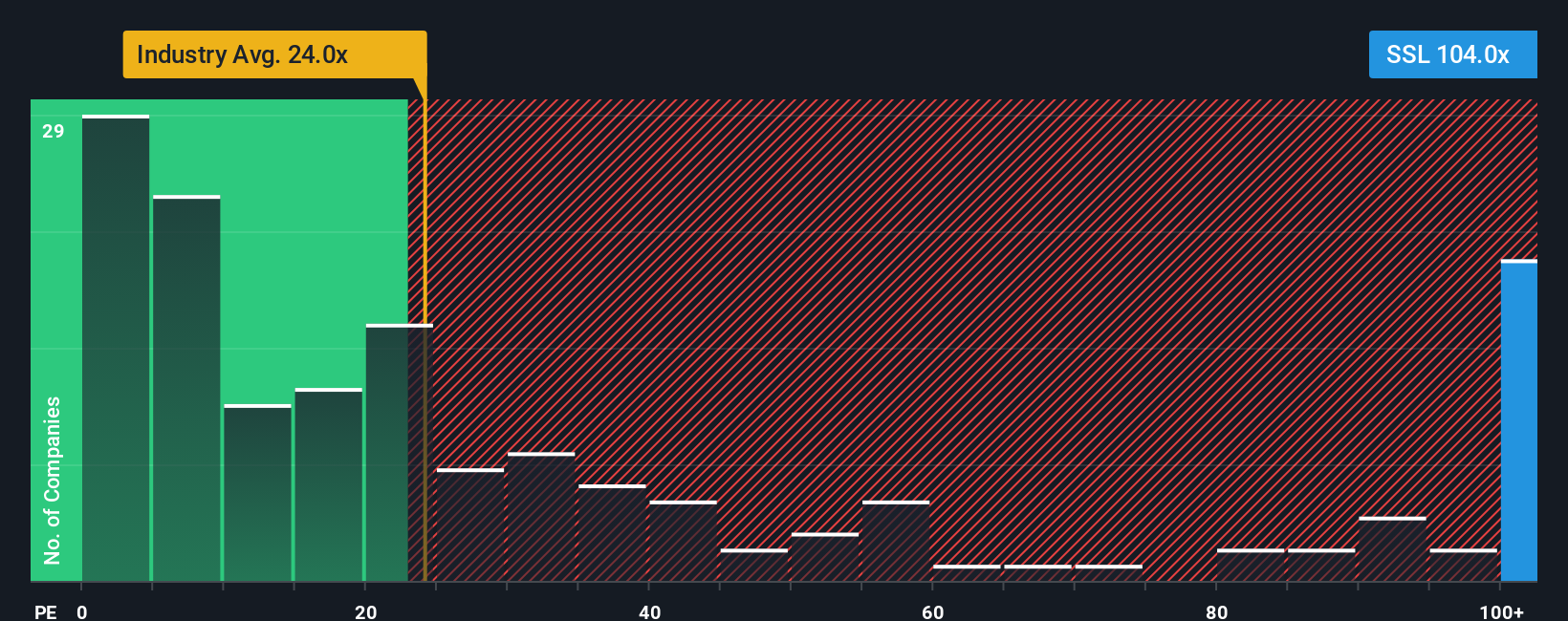

Another View: Looking at Valuation Multiples

While the most-followed narrative sees Sandstorm Gold as modestly undervalued, its current earnings multiple of 104.2x is far higher than the Canadian Metals and Mining industry average of 22.5x and its peers at 21.1x. The fair ratio, based on market regression, sits at 21.5x. This wide gap suggests the market has high hopes built into the price. What happens if growth does not keep up?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sandstorm Gold Narrative

If you see the story differently, or want to do some digging of your own, it takes just a few minutes to shape your own view. Do it your way.

A great starting point for your Sandstorm Gold research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Broaden your portfolio and keep your edge by checking out these ready-made stock ideas. There is real opportunity waiting, and quick action can put you ahead of the curve.

- Spot tomorrow’s technology leaders before the crowd by reviewing these 24 AI penny stocks, which are showing strong growth in artificial intelligence and automation.

- Capture stable income with these 18 dividend stocks with yields > 3%, offering yields above 3 percent and robust financials, ideal for balancing risk and reward.

- Take advantage of undervalued opportunities by analyzing these 878 undervalued stocks based on cash flows that meet strict cash flow standards and offer long-term upside potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SSL

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

JO

JohnJ on Worldline ·

No miracle in sight

Fair Value:€7.0178.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

78 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative