Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:ARIS

How Are Rising Costs and Resilient Margins Shaping Aris Mining’s Strategy (TSX:ARIS)?

Simply Wall St

Reviewed by Simply Wall St

- In its recent second-quarter update, Aris Mining Corporation reported an increase in all-in-sustaining costs per ounce due to higher sustaining capital expenditures, inflation-driven mining and mill feed costs, and greater use of contract mining partners.

- Despite these cost pressures, higher realized gold prices and increased sales volumes enabled Aris Mining to maintain healthy operating margins while highlighting the importance of ongoing cost control efforts.

- We’ll now explore how the company’s ability to maintain margins amid rising all-in-sustaining costs could impact its investment narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Aris Mining Investment Narrative Recap

To be a shareholder of Aris Mining, you need to believe in the company’s long-term ability to execute ambitious growth at its Colombian projects while managing geopolitical and operational risks. The recent rise in all-in-sustaining costs has not materially altered the company’s most important short-term catalyst, its ongoing production ramp-up at Segovia, or the primary risk around expansion execution and regulatory stability.

Among recent developments, the successful installation of the second ball mill at Segovia stands out. This is directly relevant to the current cost update, as the increased processing capacity is expected to support higher gold output and help offset inflationary pressures in the coming quarters, underpinning Aris Mining’s core growth catalyst.

Yet, in contrast to the encouraging production expansion, investors should be aware that rising operating costs may test management’s ability to sustain margins if...

Read the full narrative on Aris Mining (it's free!)

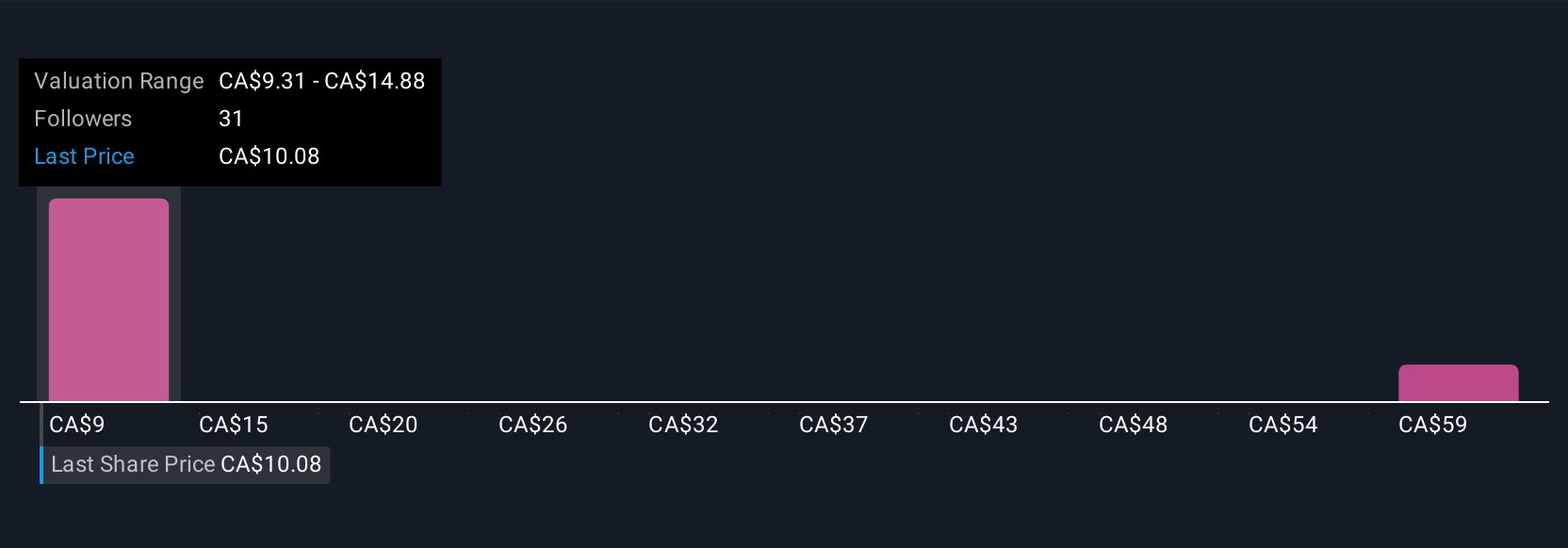

Aris Mining's outlook anticipates $1.5 billion in revenue and $695.3 million in earnings by 2028. This scenario assumes a 32.4% annual revenue growth and a sharp increase in earnings of $690.2 million from the current $5.1 million.

Uncover how Aris Mining's forecasts yield a CA$14.56 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Seven members of the Simply Wall St Community estimate Aris Mining’s fair value with targets ranging from US$2.10 to US$65. With the wide spread of opinions, remember that the company’s growth hinges on timely project expansions and meeting ambitious production targets, so it’s worth considering several perspectives before making up your mind.

Explore 7 other fair value estimates on Aris Mining - why the stock might be worth less than half the current price!

Build Your Own Aris Mining Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Aris Mining research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Aris Mining research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Aris Mining's overall financial health at a glance.

Curious About Other Options?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:ARIS

Aris Mining

Engages in the acquisition, exploration, development, and operation of gold properties in Canada, Colombia, and Guyana.

Exceptional growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|52.5% overvalued

RO

Community Contributor