Advertisement

How Will Intact Financial’s (TSX:IFC) Preferred Share Offering Shape Its Capital Strategy and Growth Path?

Simply Wall St

Reviewed by Sasha Jovanovic

- Intact Financial Corporation recently completed a CAD 150 million fixed-income offering, issuing 6,000,000 callable 5.50% Class A non-convertible preferred shares at CAD 25 per share with a CAD 0.75 discount per security.

- This move enhances Intact’s capital flexibility and may influence investor perceptions of the company’s ability to fund growth and manage its balance sheet.

- We’ll now explore how this successful preferred share issuance affects Intact Financial’s investment narrative, particularly its impact on capital structure and growth initiatives.

We've found 16 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Intact Financial Investment Narrative Recap

To be a shareholder in Intact Financial, you need to believe in the company’s ability to sustain premium growth, deliver steady profitability, and effectively balance capital for future expansion. The successful CAD 150 million preferred share issuance boosts Intact’s capital flexibility, but does not materially alter the main near-term catalyst, continued earnings stability amid integration of recent acquisitions, or the biggest risk, which is ongoing claims volatility from severe weather events. The capital raise itself does not eliminate exposure to catastrophe-driven margin pressure.

Among recent announcements, Intact’s Q3 2025 earnings report is particularly relevant here, with strong net income growth underscoring robust underlying profitability. The enhanced capital position from the preferred share offering could reinforce this trend by supporting further investments, but it does not directly address the risk of elevated catastrophe losses impacting future quarters.

In contrast, investors should be aware that while Intact’s capital position has improved, pressure from unpredictable climate losses remains a concern for...

Read the full narrative on Intact Financial (it's free!)

Intact Financial's narrative projects CA$23.7 billion revenue and CA$3.0 billion earnings by 2028. This requires a 7.0% annual revenue decline and a CA$0.7 billion earnings increase from the current CA$2.3 billion.

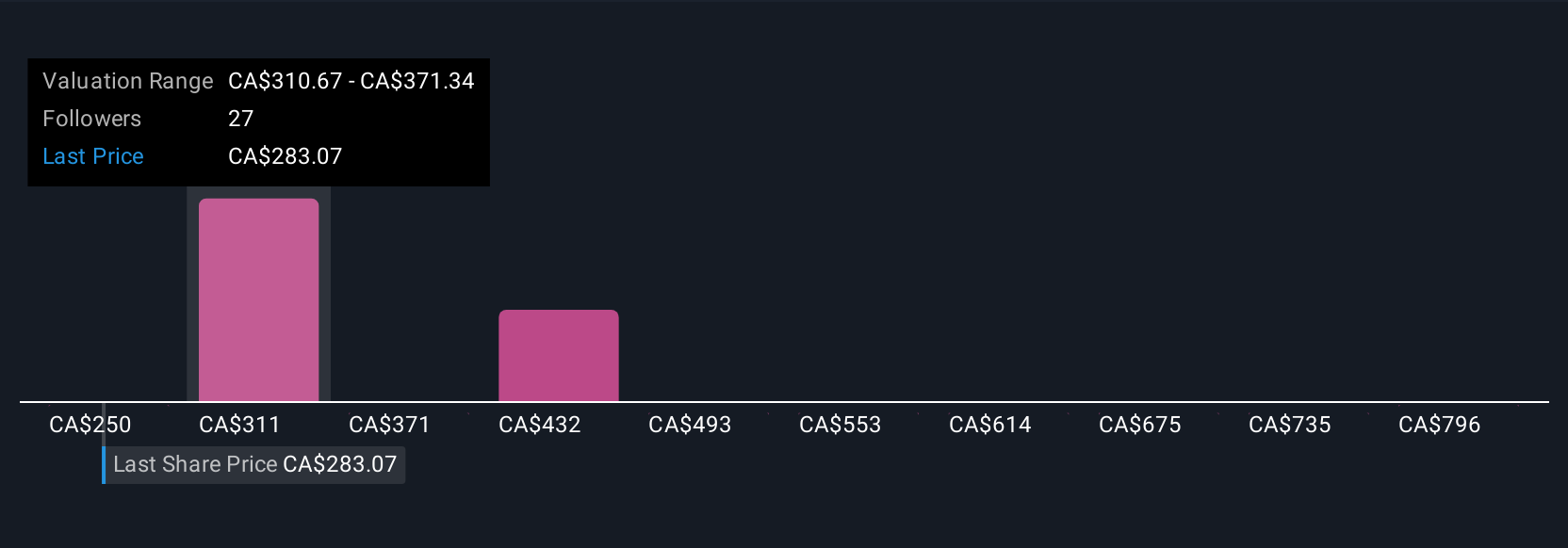

Uncover how Intact Financial's forecasts yield a CA$319.92 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Seven Simply Wall St Community members placed fair value estimates for Intact shares between CA$254 and CA$856.69. While opinions are wide ranging, the risk of recurring catastrophic weather events continues to shape overall performance outlooks.

Explore 7 other fair value estimates on Intact Financial - why the stock might be worth 11% less than the current price!

Build Your Own Intact Financial Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Intact Financial research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Intact Financial research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Intact Financial's overall financial health at a glance.

No Opportunity In Intact Financial?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:IFC

Intact Financial

Through its subsidiaries, provides property and casualty insurance products to individuals and businesses in Canada, the United States, the United Kingdom, and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor