Advertisement

- Canada

- /

- Medical Equipment

- /

- TSXV:TLT

We're Not Very Worried About Theralase Technologies' (CVE:TLT) Cash Burn Rate

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Theralase Technologies (CVE:TLT) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business' cash, relative to its cash burn.

Check out our latest analysis for Theralase Technologies

How Long Is Theralase Technologies' Cash Runway?

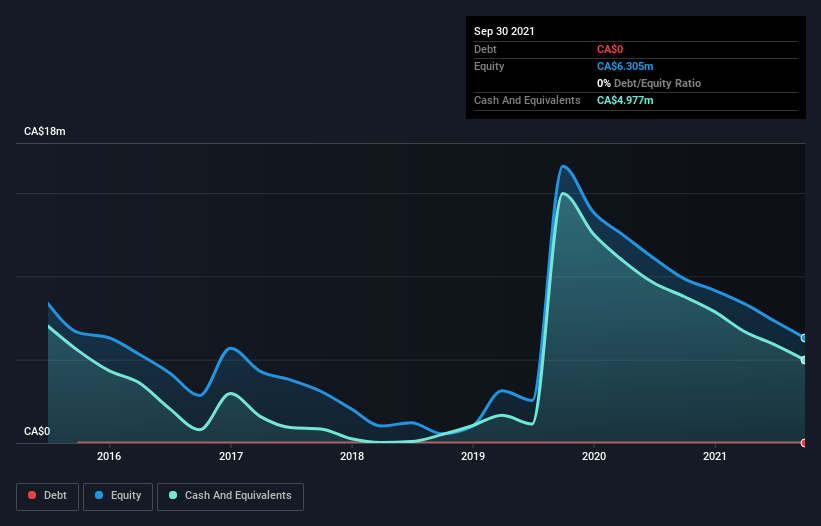

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at September 2021, Theralase Technologies had cash of CA$5.0m and no debt. In the last year, its cash burn was CA$3.8m. That means it had a cash runway of around 16 months as of September 2021. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. Depicted below, you can see how its cash holdings have changed over time.

How Is Theralase Technologies' Cash Burn Changing Over Time?

Whilst it's great to see that Theralase Technologies has already begun generating revenue from operations, last year it only produced CA$968k, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. Even though it doesn't get us excited, the 39% reduction in cash burn year on year does suggest the company can continue operating for quite some time. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Theralase Technologies Raise Cash?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for Theralase Technologies to raise more cash in the future. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Theralase Technologies' cash burn of CA$3.8m is about 5.1% of its CA$74m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

How Risky Is Theralase Technologies' Cash Burn Situation?

The good news is that in our view Theralase Technologies' cash burn situation gives shareholders real reason for optimism. Not only was its cash burn reduction quite good, but its cash burn relative to its market cap was a real positive. Based on the factors mentioned in this article, we think its cash burn situation warrants some attention from shareholders, but we don't think they should be worried. Separately, we looked at different risks affecting the company and spotted 4 warning signs for Theralase Technologies (of which 1 is a bit concerning!) you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

Valuation is complex, but we're here to simplify it.

Discover if Theralase Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:TLT

Theralase Technologies

A clinical stage pharmaceutical company, engages in the research, development, and commercialization of light activated photo dynamic compounds and their associated drug formulations to treat cancers, bacteria, and viruses in Canada, the United States, and internationally.

Exceptional growth potential with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor