- Canada

- /

- Healthcare Services

- /

- TSX:EXE

Don't Buy Extendicare Inc. (TSE:EXE) For Its Next Dividend Without Doing These Checks

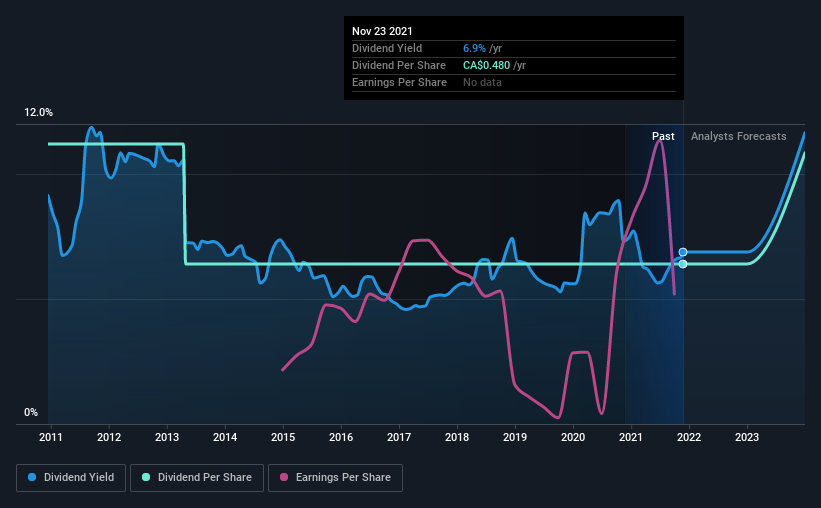

Extendicare Inc. (TSE:EXE) stock is about to trade ex-dividend in four days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Accordingly, Extendicare investors that purchase the stock on or after the 29th of November will not receive the dividend, which will be paid on the 15th of December.

The company's upcoming dividend is CA$0.04 a share, following on from the last 12 months, when the company distributed a total of CA$0.48 per share to shareholders. Looking at the last 12 months of distributions, Extendicare has a trailing yield of approximately 6.9% on its current stock price of CA$6.98. If you buy this business for its dividend, you should have an idea of whether Extendicare's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

Check out our latest analysis for Extendicare

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Extendicare distributed an unsustainably high 158% of its profit as dividends to shareholders last year. Without extenuating circumstances, we'd consider the dividend at risk of a cut. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Extendicare paid out more free cash flow than it generated - 139%, to be precise - last year, which we think is concerningly high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

As Extendicare's dividend was not well covered by either earnings or cash flow, we would be concerned that this dividend could be at risk over the long term.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. With that in mind, we're encouraged by the steady growth at Extendicare, with earnings per share up 2.4% on average over the last five years. Earnings are not growing much and Extendicare paid out a lot more than it earned in profit last year. This makes the dividend look potentially unsustainable in the long run.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Extendicare has seen its dividend decline 5.4% per annum on average over the past 10 years, which is not great to see. Extendicare is a rare case where dividends have been decreasing at the same time as earnings per share have been improving. It's unusual to see, and could point to unstable conditions in the core business, or more rarely an intensified focus on reinvesting profits.

Final Takeaway

Is Extendicare an attractive dividend stock, or better left on the shelf? The dividends are not well covered by either income or free cash flow, although at least earnings per share are slowly increasing. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

With that being said, if you're still considering Extendicare as an investment, you'll find it beneficial to know what risks this stock is facing. Our analysis shows 3 warning signs for Extendicare that we strongly recommend you have a look at before investing in the company.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Extendicare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:EXE

Extendicare

Through its subsidiaries, provides care and services for seniors in Canada.

Solid track record established dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion