- Canada

- /

- Energy Services

- /

- TSX:TOT

Top TSX Dividend Stocks To Consider In October 2024

Reviewed by Simply Wall St

As the Canadian market navigates a landscape shaped by shifting expectations around U.S. Federal Reserve rate cuts and global economic uncertainties, investors are increasingly focused on stable income sources such as dividend stocks. In this context, selecting dividend stocks that offer consistent payouts and potential for growth can be an effective strategy to weather fluctuating interest rates and economic conditions.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 6.95% | ★★★★★★ |

| Labrador Iron Ore Royalty (TSX:LIF) | 8.17% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 5.07% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.41% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.54% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.27% | ★★★★★☆ |

| Richards Packaging Income Fund (TSX:RPI.UN) | 5.45% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.12% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.31% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.42% | ★★★★★☆ |

Click here to see the full list of 29 stocks from our Top TSX Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

Bank of Montreal (TSX:BMO)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Bank of Montreal offers diversified financial services mainly in North America and has a market cap of approximately CA$94.50 billion.

Operations: Bank of Montreal's revenue segments include CA$10.20 billion from Canadian Personal and Commercial Banking, CA$8.89 billion from U.S. Personal and Commercial Banking, CA$7.61 billion from BMO Wealth Management, and CA$6.47 billion from BMO Capital Markets.

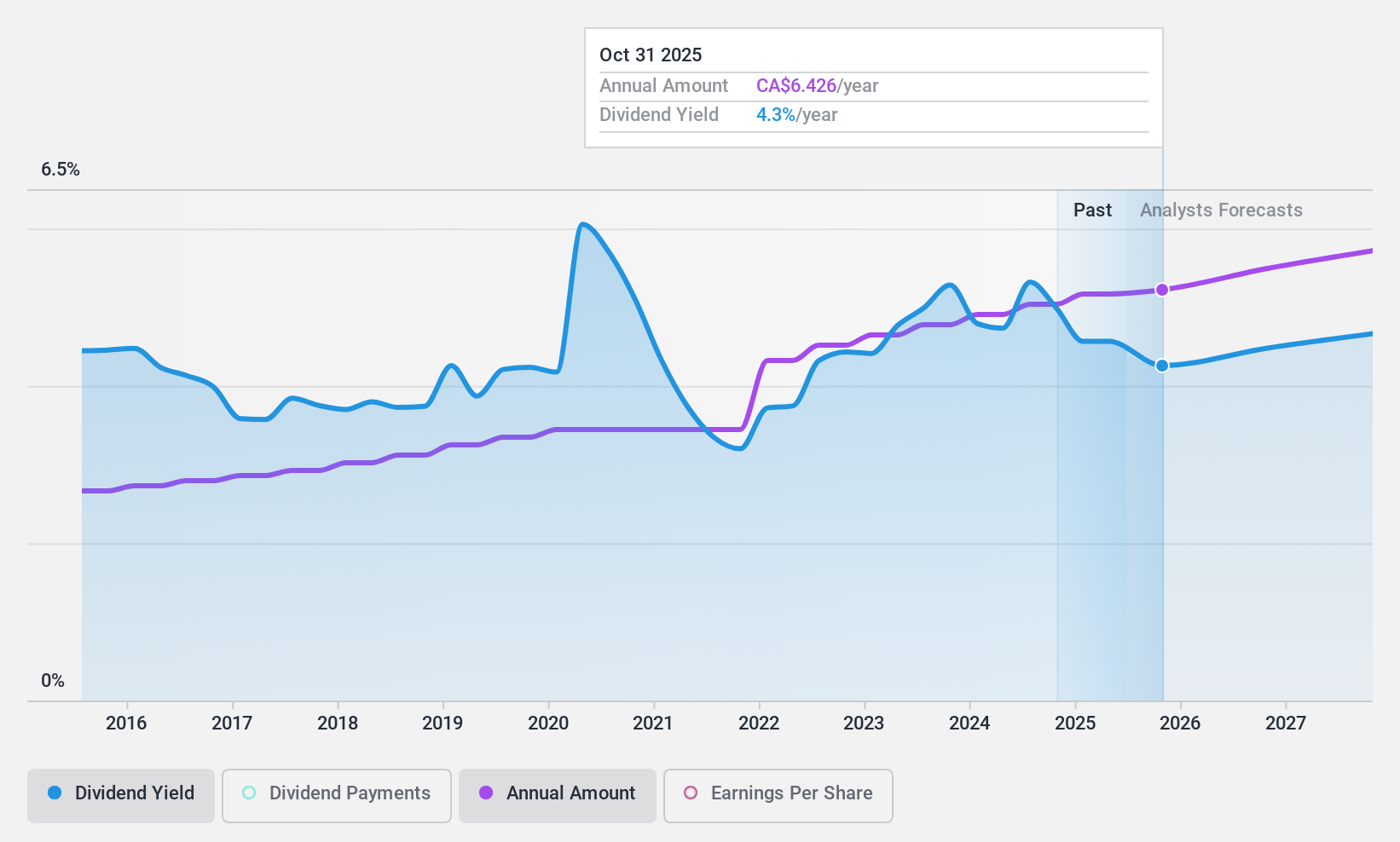

Dividend Yield: 4.9%

Bank of Montreal offers a stable dividend profile with consistent payments over the past decade. Although its current dividend yield of 4.85% is below the top tier in Canada, it remains reliable and well-covered by earnings, with a payout ratio of 69.5%. Recent board appointments may enhance governance, while ongoing fixed-income offerings reflect robust financial activities. The bank's strategic initiatives like PaySmart could support future growth and reinforce its dividend sustainability.

- Click here and access our complete dividend analysis report to understand the dynamics of Bank of Montreal.

- Upon reviewing our latest valuation report, Bank of Montreal's share price might be too optimistic.

Quebecor (TSX:QBR.A)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Quebecor Inc. operates in the telecommunications, media, and sports and entertainment sectors in Canada, with a market cap of CA$8.21 billion.

Operations: Quebecor Inc. generates revenue from its telecommunications segment with CA$4.89 billion, media segment with CA$724 million, and sports and entertainment segment with CA$208.2 million.

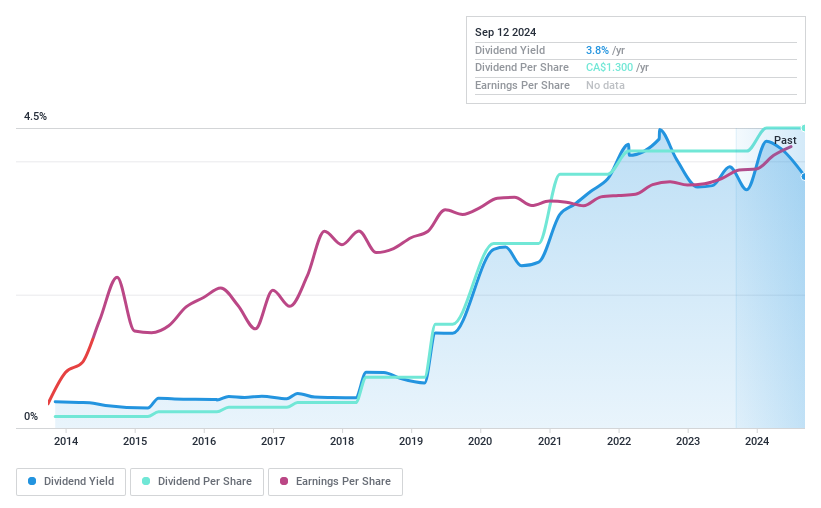

Dividend Yield: 3.7%

Quebecor's dividend profile is marked by stability and reliability, with consistent growth over the past decade. Its dividends are well-covered by earnings and cash flows, evidenced by a payout ratio of 39.2% and a cash payout ratio of 44.4%. Despite trading at an attractive value below its estimated fair value, Quebecor carries a high level of debt. Recent buyback initiatives and solid earnings growth further support its financial position, though the dividend yield remains modest compared to top Canadian payers.

- Navigate through the intricacies of Quebecor with our comprehensive dividend report here.

- In light of our recent valuation report, it seems possible that Quebecor is trading behind its estimated value.

Total Energy Services (TSX:TOT)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Total Energy Services Inc. is an energy services company operating in Canada, the United States, and Australia with a market cap of CA$368.58 million.

Operations: Total Energy Services Inc. generates revenue through four primary segments: Well Servicing (CA$89.94 million), Contract Drilling Services (CA$299.62 million), Compression and Process Services (CA$393.38 million), and Rentals and Transportation Services (CA$80.86 million).

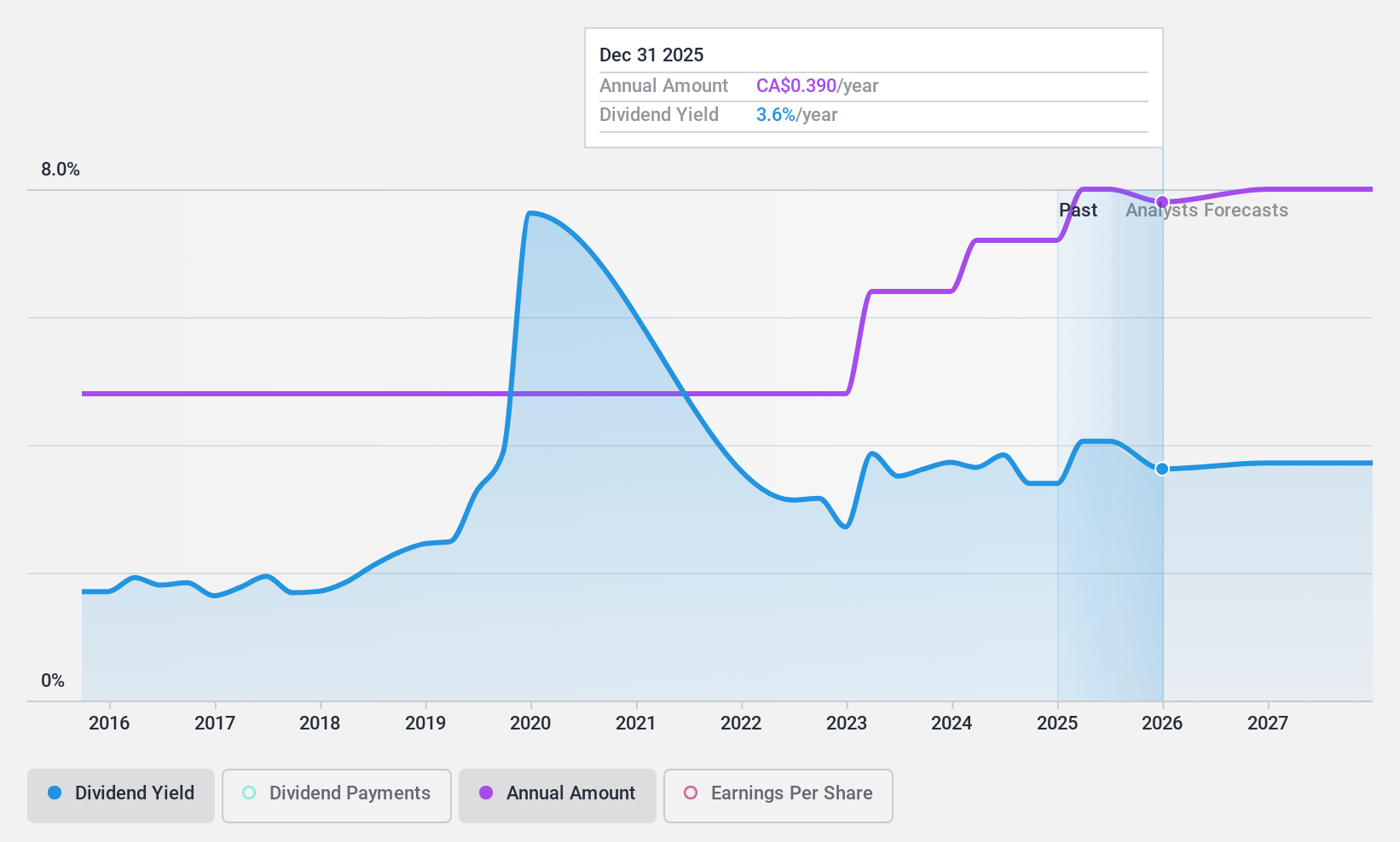

Dividend Yield: 3.7%

Total Energy Services' dividend is well-covered by earnings and cash flows, with payout ratios of 32% and 24.6%, respectively. However, its dividend history has been volatile over the past decade. The current yield of 3.73% is below top-tier Canadian payers. Recent initiatives include a share buyback program, potentially enhancing shareholder value by reducing outstanding shares from 38.19 million, while recent earnings show improved net income at C$15.47 million for Q2 2024.

- Dive into the specifics of Total Energy Services here with our thorough dividend report.

- According our valuation report, there's an indication that Total Energy Services' share price might be on the cheaper side.

Next Steps

- Get an in-depth perspective on all 29 Top TSX Dividend Stocks by using our screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Total Energy Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TOT

Total Energy Services

Operates as an energy services company primarily in Canada, the United States, and Australia.

Flawless balance sheet, good value and pays a dividend.