Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:SOBO

A Fresh Look at South Bow (TSX:SOBO) Valuation After Higher Q3 Profits and Maintained Dividend

Simply Wall St

Reviewed by Simply Wall St

South Bow (TSX:SOBO) just released its third quarter and nine-month results, showing higher net income and earnings per share, even as sales dipped. The board also confirmed a steady dividend payout.

See our latest analysis for South Bow.

South Bow’s upbeat third quarter, combined with the confirmed dividend, has caught the market’s attention. The share price has climbed 11.1% year-to-date. This reflects both the recent 5% one-week jump and investor optimism about sustained profitability despite lower sales. Measured by total shareholder return, the past twelve months have delivered a solid 15.4% gain. This suggests that positive momentum could continue as the company shows resilience through industry ups and downs.

If these moves have you reevaluating your strategy, now’s a great moment to broaden your search and discover fast growing stocks with high insider ownership

With profits rising and dividends steady, is South Bow actually trading below its true value? Alternatively, has the market already factored in expectations for further growth, leaving little room for new investors to capitalize?

Price-to-Earnings of 17.2x: Is it justified?

South Bow’s shares are trading at a price-to-earnings (P/E) ratio of 17.2x, which signals that investors are paying a premium relative to recent company earnings. With the last close at CA$38.45, this places the stock above both industry and fair value benchmarks.

The P/E ratio is a classic valuation multiple, showing how much investors are willing to pay for each dollar of earnings. In the oil and gas sector, this figure often reflects the market’s confidence in consistent profitability and room for growth in an inherently cyclical industry.

However, at 17.2x, South Bow appears expensive compared to both the Canadian Oil and Gas industry average of 14.7x and our estimated fair P/E ratio of 14.2x. This suggests that the market may be pricing in more optimistic future performance or viewing the company as safer or more stable than its peers. The difference means that if underlying growth or profitability does not accelerate, there is a risk of valuation compression toward the fair ratio level.

Explore the SWS fair ratio for South Bow

Result: Price-to-Earnings of 17.2x (OVERVALUED)

However, a premium valuation could unwind if South Bow’s earnings miss expectations or if sector volatility reduces investor enthusiasm in coming quarters.

Find out about the key risks to this South Bow narrative.

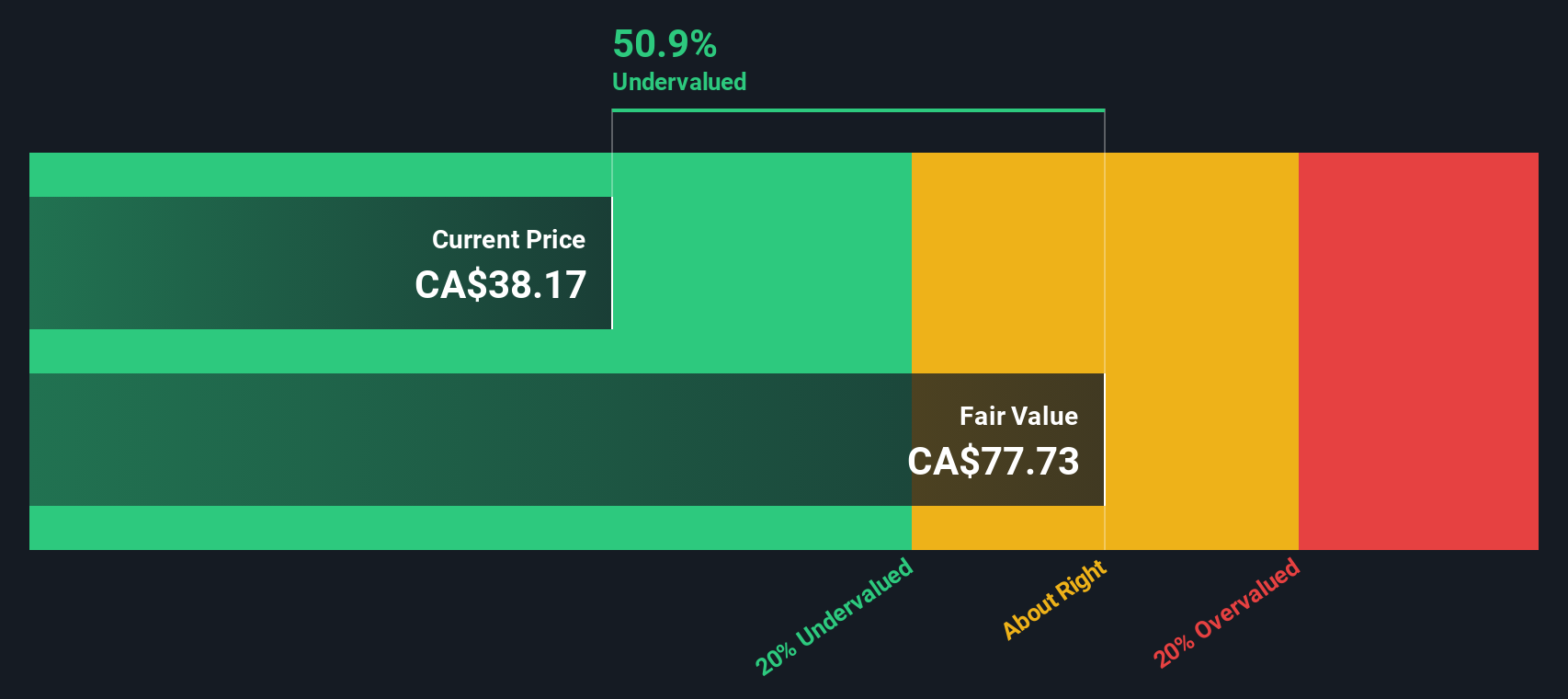

Another View: DCF Model Suggests Shares May Be Undervalued

While South Bow appears expensive when using the earnings multiple method, our DCF model takes a different approach. It estimates a fair value of CA$89.59 per share. This figure is significantly higher than today’s CA$38.45 price. Is the market overlooking long-term cash flow potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out South Bow for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own South Bow Narrative

If you’d rather reach your own conclusions, you can check out all the numbers yourself and draft your personal outlook in just a few minutes. Do it your way

A great starting point for your South Bow research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let opportunity pass you by. Make your next smart move and check out these powerful ideas, handpicked to help you stay ahead of the market.

- Capture growth potential and spot opportunities before the crowd by reviewing these 3584 penny stocks with strong financials, which are backed by robust fundamentals.

- Find tomorrow’s game-changers when you examine these 24 AI penny stocks, companies that are pushing the boundaries of artificial intelligence advances.

- Boost your income strategies and secure attractive payouts by exploring these 16 dividend stocks with yields > 3%, featuring high-yield potential and solid financials.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SOBO

Fair value with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor