Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:IPCO

International Petroleum (TSX:IPCO): Assessing Valuation Following Latest Share Cancellation for Capital Optimization

Simply Wall St

Reviewed by Simply Wall St

International Petroleum (TSX:IPCO) has just cancelled 24,538 common shares that were repurchased as part of its active share buyback program. This move fits neatly into the company’s consistent focus on tightening capital structure and strengthening shareholder value.

See our latest analysis for International Petroleum.

After this latest share cancellation update, International Petroleum’s momentum remains notable. While the short-term 30-day share price return is down 5.5%, the company’s year-to-date share price is still up 27.8%, and the one-year total shareholder return sits at an impressive 41%, with five-year total returns near 961%. This kind of performance, alongside upcoming financial results, suggests that investors continue to see long-term potential, even as short-term swings reflect the typical volatility of the energy sector.

If you’re sizing up what’s working outside the usual energy names, now’s the perfect time to broaden your search and discover fast growing stocks with high insider ownership

But with shares still trading at a 13% discount to analyst price targets and strong fundamentals, investors must now decide whether International Petroleum remains undervalued or if the market is fully pricing in future growth.

Most Popular Narrative: 11.5% Undervalued

The current fair value calculation places International Petroleum at a double-digit discount to the latest closing price, sparking renewed debate among followers as to whether the rally still has legs. The following narrative, supported by the prevailing catalysts and financial projections, forms the foundation for this viewpoint.

The imminent completion and ramp-up of Blackrod Phase 1 is expected to significantly increase long-life, low-cost production, materially improving operating cash flow and free cash flow from late 2026 onwards, supporting future revenue and earnings growth.

Want to glimpse the logic behind this bullish price tag? The main assumptions driving fair value focus on a pivotal new asset and a bold profit forecast, both set to reshape earnings expectations. Wondering just how aggressive these projections are, or what makes analysts confident about this inflection point? Dive in to uncover what numbers underpin this narrative's valuation call.

Result: Fair Value of $25.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued dependence on Blackrod Phase 1 and sector-wide climate policy shifts could quickly challenge bullish assumptions if project timelines are delayed or if regulations become more stringent.

Find out about the key risks to this International Petroleum narrative.

Another View: Market Multiples Paint a Costlier Picture

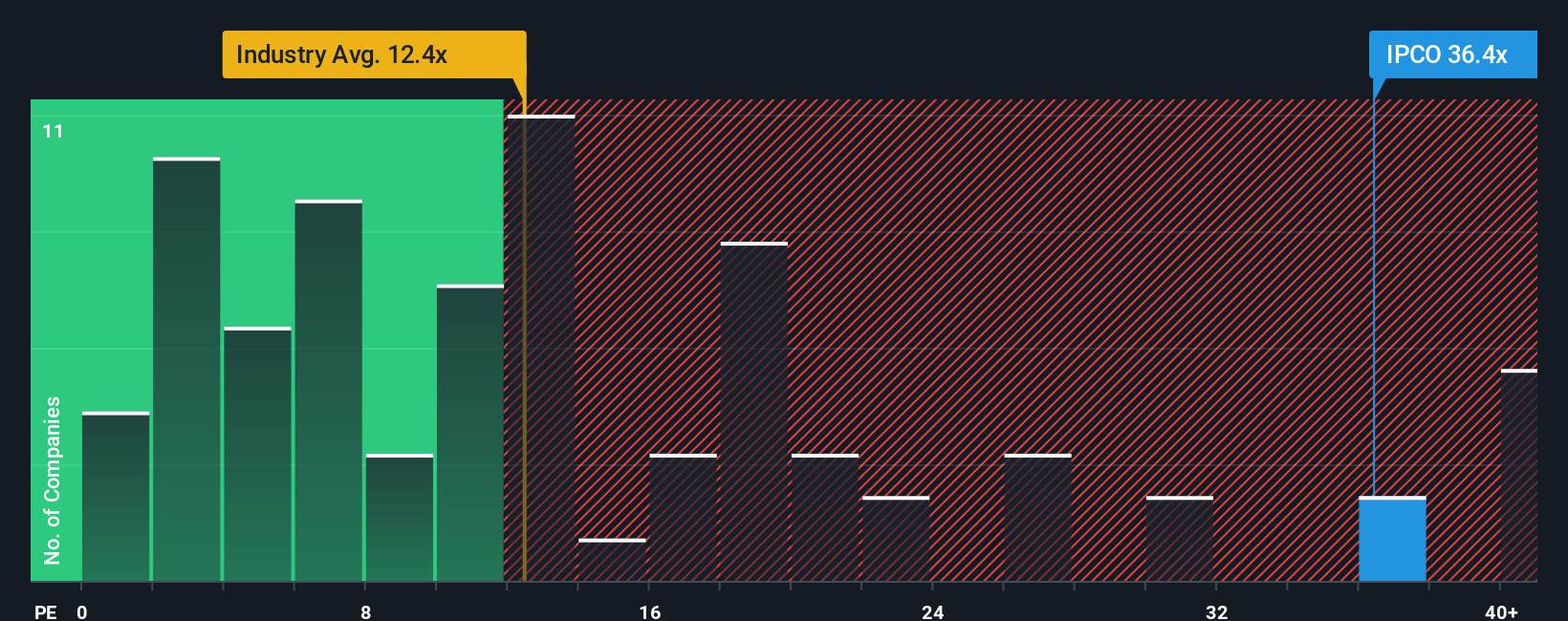

Looking at International Petroleum through the lens of its price-to-earnings ratio, things do not look as cheap. The company trades at 33.4 times earnings, well above the Canadian Oil and Gas industry average of 12.4x and its peer average of 15.4x. Even compared to its fair ratio of 18.9x, the shares appear expensive. This wide gap suggests the market is placing a hefty premium on future growth. The question remains whether recent performance truly justifies that optimism.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own International Petroleum Narrative

If you think there’s another angle to the story or want to run the numbers your way, you can quickly craft your own take in under three minutes with Do it your way.

A great starting point for your International Petroleum research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Staying ahead of the market means always broadening your opportunity set. Don’t let your next winning idea slip by. Tap into these powerful stock searches now:

- Spot tomorrow’s winners early by checking out these 3588 penny stocks with strong financials making waves with strong financials and bold growth stories.

- Capitalize on unstoppable trends by tracking these 26 AI penny stocks transforming industries through breakthroughs in artificial intelligence and automation.

- Capture more upside in today’s market by finding these 840 undervalued stocks based on cash flows that are priced below their potential based on real cash flow data.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:IPCO

International Petroleum

Explores for, develops, and produces oil and gas.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor