- Canada

- /

- Oil and Gas

- /

- TSX:HWX

Undiscovered Gems in Canada Promising Stocks to Explore October 2024

Reviewed by Simply Wall St

As markets continue to ride a wave of optimism fueled by recent rate cuts and enthusiasm around AI, the TSX has reached all-time highs, reflecting a broader trend of economic expansion and rising corporate earnings. In this environment, identifying promising small-cap stocks in Canada can be particularly rewarding, as these companies often thrive under conditions of easing monetary policy and robust market fundamentals.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Mandalay Resources | 11.86% | 9.48% | 37.58% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Tornado Global Hydrovacs | 14.62% | 24.52% | 64.90% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

Freehold Royalties (TSX:FRU)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Freehold Royalties Ltd. focuses on acquiring and managing royalty interests in crude oil, natural gas, natural gas liquids, and potash properties across Western Canada and the United States, with a market cap of CA$2.14 billion.

Operations: Freehold Royalties Ltd. generates revenue primarily from its oil and gas exploration and production segment, amounting to CA$323.04 million. The company's market cap is approximately CA$2.14 billion, reflecting its valuation in the industry.

Trading at a significant discount to its estimated fair value, Freehold Royalties stands out with high-quality earnings and a satisfactory net debt to equity ratio of 24.6%. Despite recent negative earnings growth of -5.9%, the company's interest payments are well covered by EBIT at 15.3 times, indicating financial stability. Recent performance shows net income for Q2 2024 at C$39.3 million, up from C$24.26 million last year, reflecting improved profitability amidst industry challenges.

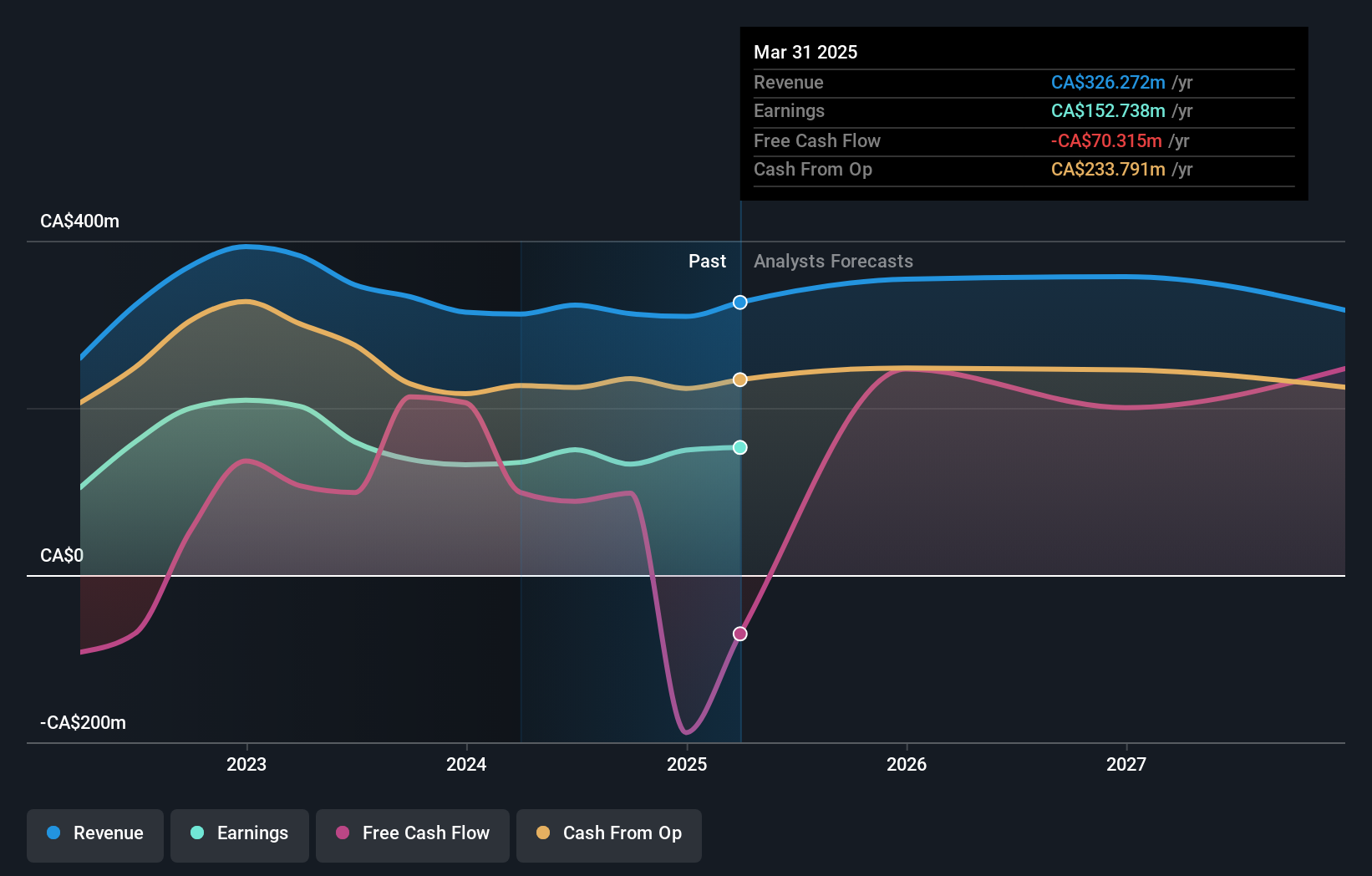

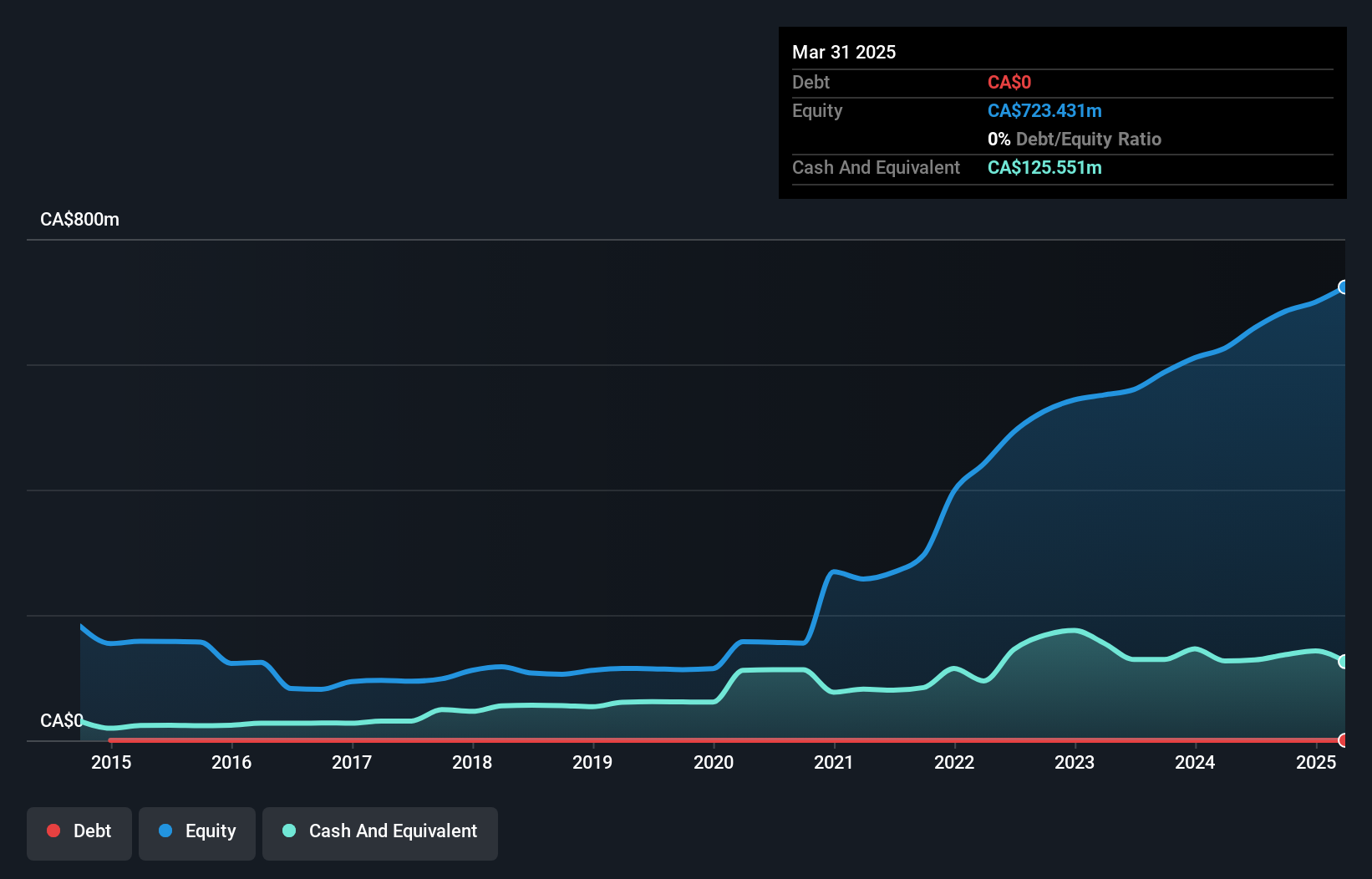

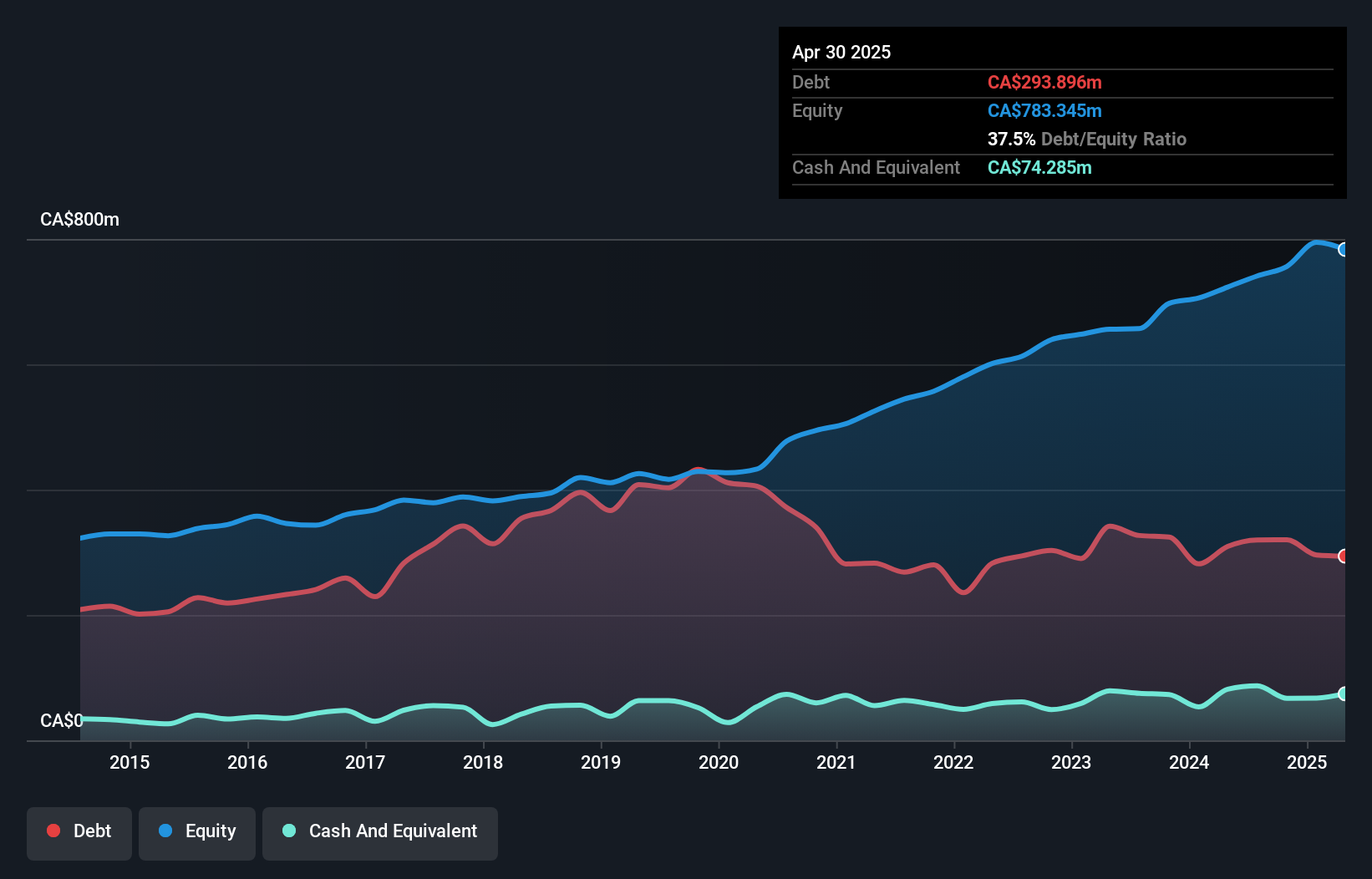

Headwater Exploration (TSX:HWX)

Simply Wall St Value Rating: ★★★★★★

Overview: Headwater Exploration Inc. is a Canadian company focused on the exploration, development, and production of petroleum and natural gas, with a market cap of CA$1.54 billion.

Operations: Headwater Exploration generates revenue primarily from the exploration, development, and production of petroleum and natural gas, amounting to CA$484.24 million.

Headwater Exploration, a Canadian oil and gas player, showcases impressive financial health with no debt over the past five years and trades at 80.4% below its estimated fair value. The company reported a net income of CAD 53.87 million for Q2 2024, up from CAD 30.95 million the previous year, highlighting high-quality earnings growth of 41.1%. Despite a dip in natural gas production to 5.5 mmcf/d from last year's 8.5 mmcf/d, heavy crude oil output rose significantly to 18,825 bbls/d compared to last year's figures.

- Delve into the full analysis health report here for a deeper understanding of Headwater Exploration.

North West (TSX:NWC)

Simply Wall St Value Rating: ★★★★★★

Overview: The North West Company Inc. operates as a retailer of food and everyday products and services in rural communities and urban neighborhood markets across northern Canada, rural Alaska, the South Pacific, and the Caribbean, with a market cap of CA$2.49 billion.

Operations: North West generates revenue primarily from retailing food and everyday products and services, amounting to CA$2.52 billion.

North West, a promising player in the consumer retail sector, has shown robust earnings growth of 9.5% over the past year, surpassing industry averages. The firm trades at 43.2% below its estimated fair value and carries a satisfactory net debt to equity ratio of 31.4%. Despite recent insider selling, North West remains free cash flow positive with well-covered interest payments by EBIT at 10.9x coverage, indicating solid financial health amidst market challenges.

- Navigate through the intricacies of North West with our comprehensive health report here.

Examine North West's past performance report to understand how it has performed in the past.

Turning Ideas Into Actions

- Click here to access our complete index of 48 TSX Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Headwater Exploration might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:HWX

Headwater Exploration

Engages in the exploration, development, and production of petroleum and natural gas in Canada.

Flawless balance sheet with solid track record.