Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:HWX

There's No Escaping Headwater Exploration Inc.'s (TSE:HWX) Muted Earnings Despite A 28% Share Price Rise

The Headwater Exploration Inc. (TSE:HWX) share price has done very well over the last month, posting an excellent gain of 28%. Taking a wider view, although not as strong as the last month, the full year gain of 25% is also fairly reasonable.

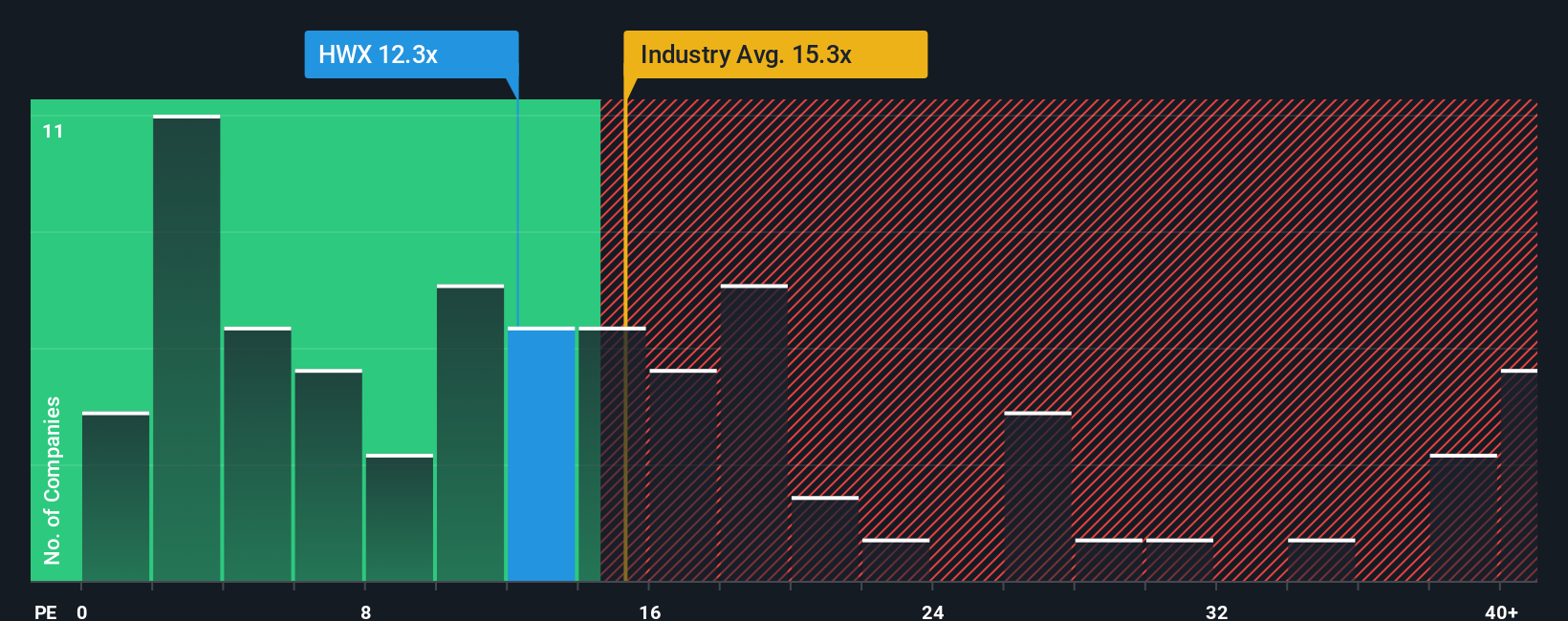

In spite of the firm bounce in price, given about half the companies in Canada have price-to-earnings ratios (or "P/E's") above 17x, you may still consider Headwater Exploration as an attractive investment with its 12.3x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Headwater Exploration hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

See our latest analysis for Headwater Exploration

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Headwater Exploration's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 6.9% decrease to the company's bottom line. Regardless, EPS has managed to lift by a handy 6.1% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Shifting to the future, estimates from the four analysts covering the company suggest earnings growth is heading into negative territory, declining 21% over the next year. Meanwhile, the broader market is forecast to expand by 23%, which paints a poor picture.

In light of this, it's understandable that Headwater Exploration's P/E would sit below the majority of other companies. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Key Takeaway

Headwater Exploration's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Headwater Exploration maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 2 warning signs for Headwater Exploration (1 shouldn't be ignored!) that we have uncovered.

If these risks are making you reconsider your opinion on Headwater Exploration, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Headwater Exploration might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:HWX

Headwater Exploration

Engages in the exploration, development, and production of petroleum and natural gas resources in Canada.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor