- Canada

- /

- Capital Markets

- /

- TSX:BAM

Brookfield Asset Management (TSX:BAM): Assessing Valuation After Recent Share Price Underperformance

Reviewed by Simply Wall St

Brookfield Asset Management (TSX:BAM) has quietly underperformed this year, with the stock down about 8% year to date even as its underlying business continues to post double digit revenue and net income growth.

See our latest analysis for Brookfield Asset Management.

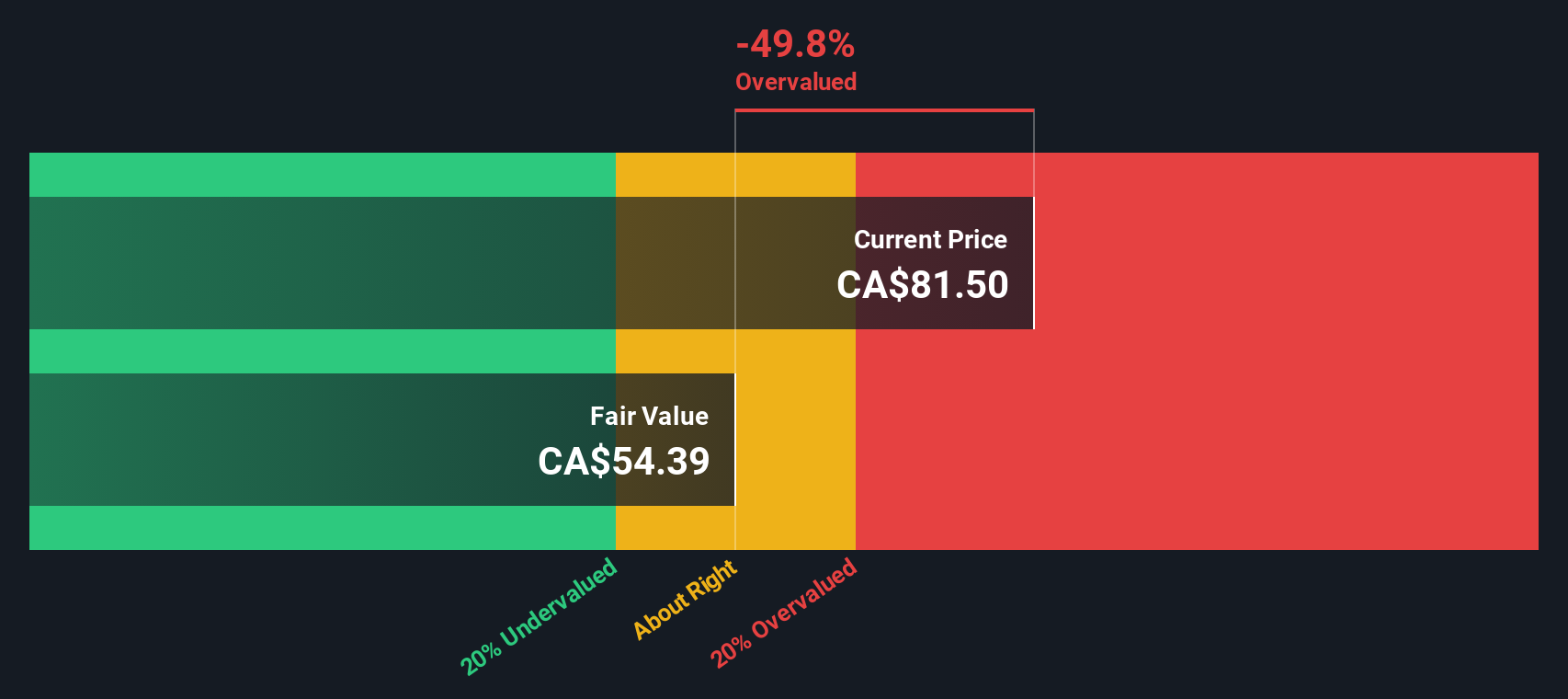

That disconnect shows up in the tape too, with the shares sitting at $72.11 after a roughly 8% year to date share price decline. Even so, the three year total shareholder return of about 110% still signals strong long term momentum rather than a broken story.

If you like the long term compounding angle behind Brookfield’s growth platform, it is also worth scanning for other managers and operators with aligned incentives via fast growing stocks with high insider ownership.

With double digit earnings growth, a modest discount to analyst targets and a stellar three year track record, investors now face the key question: is Brookfield Asset Management undervalued, or is the market already pricing in its future growth?

Price-to-Earnings of 32.3x: Is it justified?

On a price-to-earnings basis, Brookfield Asset Management looks richly priced at 32.3 times earnings compared to its CA$72.11 last close.

The price-to-earnings ratio compares the current share price to per share earnings and is a quick snapshot of how much investors are willing to pay for each dollar of profit. For a capital markets and asset management business, this multiple often reflects expectations for durable fee income, scalable growth and the quality of earnings.

In Brookfield Asset Management’s case, the 32.3 times earnings tag stands well above the Canadian Capital Markets industry average of 8.9 times. This suggests the market is assigning a premium to its profit growth, high margins and return profile. However, it also trades above the estimated fair price-to-earnings ratio of 23.9 times. This is a level the market could gravitate toward if growth expectations or sentiment cool from current levels.

Explore the SWS fair ratio for Brookfield Asset Management

Result: Price-to-Earnings of 32.3x (OVERVALUED)

However, investors should watch for slower fund inflows or weaker capital markets, which could compress fees, challenge growth assumptions, and pressure that premium valuation.

Find out about the key risks to this Brookfield Asset Management narrative.

Another Angle on Valuation

Our DCF model points in a different direction, suggesting Brookfield Asset Management is overvalued, with the current CA$72.11 price sitting above an estimated fair value of CA$58.27. If cash flows matter more than today’s earnings momentum, the downside risk could be larger than it appears.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Brookfield Asset Management for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 917 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Brookfield Asset Management Narrative

If you see the numbers differently or want to dig into the data yourself, you can build a custom narrative in just a few minutes using Do it your way.

A great starting point for your Brookfield Asset Management research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

Brookfield might be on your radar, but do not stop there, smart investors stay ahead by acting on fresh, data driven stock ideas before the crowd.

- Catch early stage potential by scanning these 3629 penny stocks with strong financials that pair tiny share prices with real business strength.

- Target mispriced opportunities using these 917 undervalued stocks based on cash flows built around cash flow driven valuation signals.

- Lock in reliable income prospects through these 13 dividend stocks with yields > 3% focused on yields above 3 percent.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Brookfield Asset Management might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BAM

Brookfield Asset Management

A private equity firm specializing in acquisitions and growth capital investments.

Outstanding track record with excellent balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion