Advertisement

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Evergreen Gaming Corporation (CVE:TNA) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Evergreen Gaming

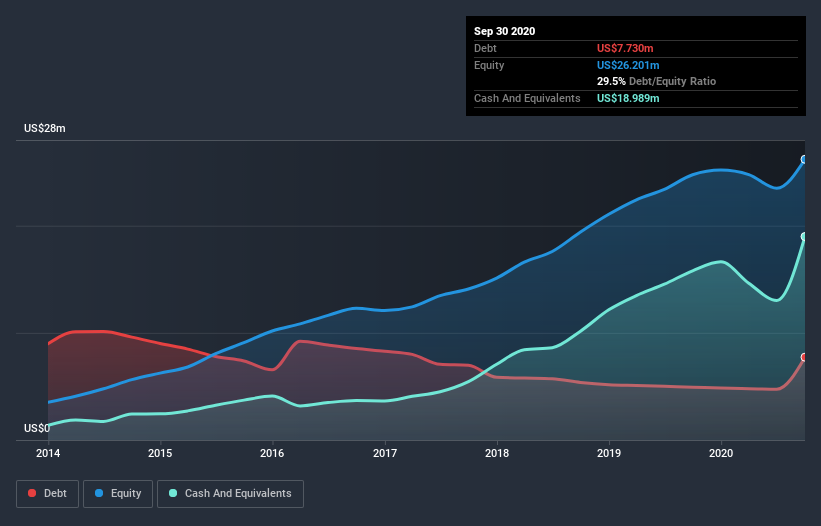

What Is Evergreen Gaming's Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Evergreen Gaming had US$7.73m of debt, an increase on US$4.93m, over one year. However, it does have US$19.0m in cash offsetting this, leading to net cash of US$11.3m.

A Look At Evergreen Gaming's Liabilities

Zooming in on the latest balance sheet data, we can see that Evergreen Gaming had liabilities of US$3.20m due within 12 months and liabilities of US$8.71m due beyond that. On the other hand, it had cash of US$19.0m and US$36.0k worth of receivables due within a year. So it actually has US$7.12m more liquid assets than total liabilities.

It's good to see that Evergreen Gaming has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Succinctly put, Evergreen Gaming boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Evergreen Gaming will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Evergreen Gaming made a loss at the EBIT level, and saw its revenue drop to US$23m, which is a fall of 40%. That makes us nervous, to say the least.

So How Risky Is Evergreen Gaming?

Although Evergreen Gaming had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of US$1.4m. So taking that on face value, and considering the cash, we don't think its very risky in the near term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Evergreen Gaming you should be aware of, and 1 of them shouldn't be ignored.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Evergreen Gaming, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Evergreen Gaming might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TSXV:TNA

Evergreen Gaming

Evergreen Gaming Corporation, through its subsidiaries, engages in the operation of casinos in the United States and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|57.7% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.6% undervalued

ZW

Community Contributor