Advertisement

- Canada

- /

- Aerospace & Defense

- /

- TSXV:FLY

We Think FLYHT Aerospace Solutions (CVE:FLY) Has A Fair Chunk Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that FLYHT Aerospace Solutions Ltd. (CVE:FLY) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for FLYHT Aerospace Solutions

What Is FLYHT Aerospace Solutions's Debt?

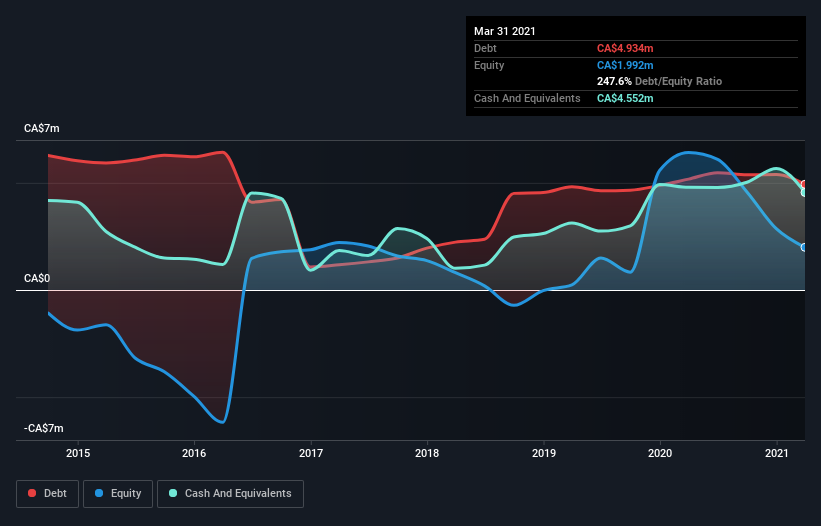

As you can see below, FLYHT Aerospace Solutions had CA$4.93m of debt at March 2021, down from CA$5.17m a year prior. However, it does have CA$4.55m in cash offsetting this, leading to net debt of about CA$381.9k.

How Healthy Is FLYHT Aerospace Solutions' Balance Sheet?

The latest balance sheet data shows that FLYHT Aerospace Solutions had liabilities of CA$6.12m due within a year, and liabilities of CA$4.66m falling due after that. Offsetting these obligations, it had cash of CA$4.55m as well as receivables valued at CA$2.20m due within 12 months. So it has liabilities totalling CA$4.02m more than its cash and near-term receivables, combined.

Of course, FLYHT Aerospace Solutions has a market capitalization of CA$33.2m, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Carrying virtually no net debt, FLYHT Aerospace Solutions has a very light debt load indeed. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine FLYHT Aerospace Solutions's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year FLYHT Aerospace Solutions had a loss before interest and tax, and actually shrunk its revenue by 48%, to CA$11m. To be frank that doesn't bode well.

Caveat Emptor

While FLYHT Aerospace Solutions's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. Its EBIT loss was a whopping CA$4.9m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through CA$598k of cash over the last year. So to be blunt we think it is risky. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 4 warning signs for FLYHT Aerospace Solutions you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:FLY

FLYHT Aerospace Solutions

Provides real-time communications with aircrafts for the aerospace industry.

Slight and slightly overvalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor