- Canada

- /

- Construction

- /

- TSX:STN

Stantec (TSX:STN): Valuation Check as Oversold Signals Meet Steady Earnings and Rebound Expectations

Reviewed by Simply Wall St

Stantec (TSX:STN) has slipped in recent weeks, and that pullback is catching attention as some see the stock drifting into oversold territory just as its earnings strength and fundamentals stay intact.

See our latest analysis for Stantec.

Even with the recent pullback and a 90 day share price return of negative 15.24 percent, Stantec’s longer term total shareholder returns, including a 105.50 percent three year gain, still point to solid underlying momentum rather than a broken story.

If Stantec’s setup has you thinking more broadly about infrastructure linked growth, this could be a good moment to explore aerospace and defense stocks as another way to find potential opportunities.

With earnings still growing faster than revenue and the share price now trading at a steep discount to analyst targets, investors face a key question: is Stantec quietly undervalued here, or is the market already pricing in its next leg of growth?

Most Popular Narrative: 24.3% Undervalued

With Stantec last closing at CA$128.19 against a narrative fair value of about CA$169.36, the current pullback is framed as a potential discount on long term earnings power.

Strengthening mix from higher margin environmental and consulting services, plus operational discipline in project execution, is already raising adjusted EBITDA margins and earnings, with further upside as organic growth accelerates and integration synergies from recent acquisitions are realized.

Curious how steady double digit growth, widening margins, and a premium future earnings multiple all intersect to justify that higher fair value? The full narrative unpacks the precise assumptions behind those projections.

Result: Fair Value of $169.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained labor constraints or slower infrastructure funding could squeeze margins and delay project backlogs, challenging the upbeat long term earnings narrative.

Find out about the key risks to this Stantec narrative.

Another View: High Multiple Signals Caution

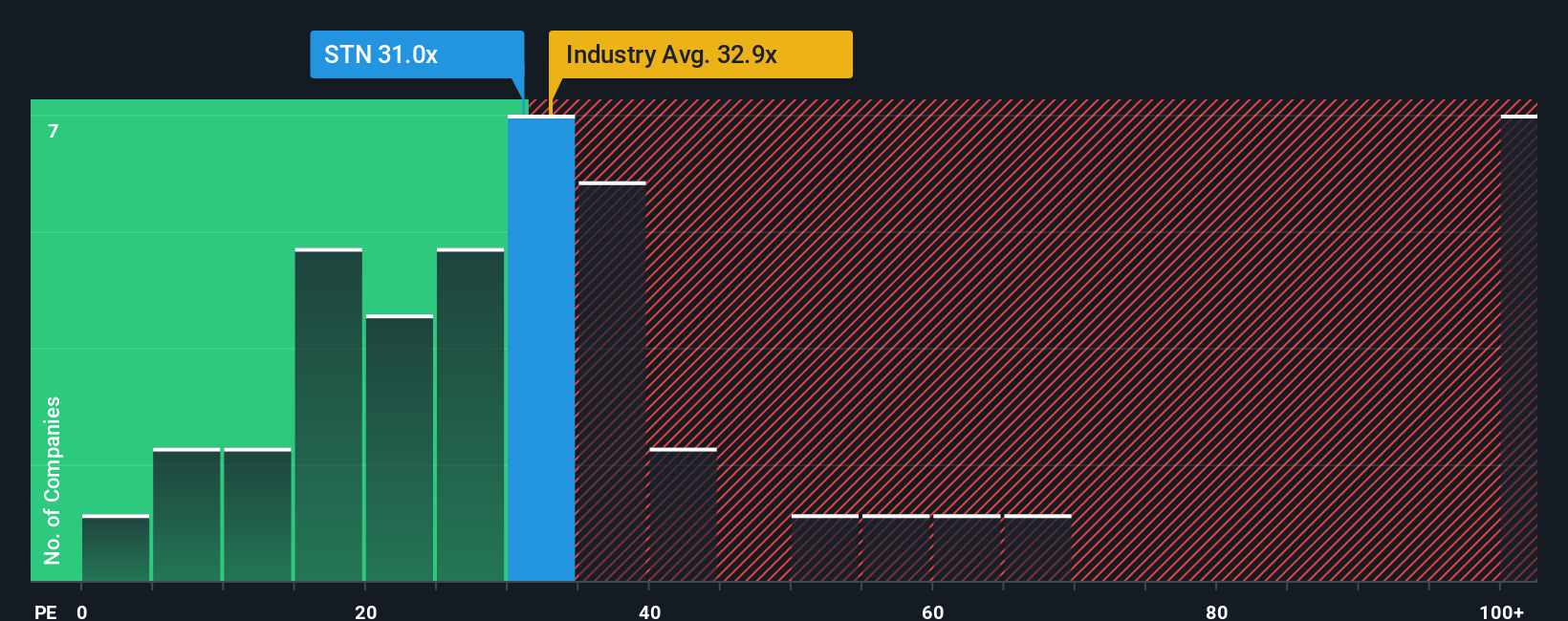

While narratives suggest upside to fair value, the current price already bakes in a lot of optimism. Stantec is trading on a 30.2x price to earnings ratio compared with a 24.8x fair ratio, 22.1x peers, and 29.9x the wider industry. Is the recent pullback enough to offset that valuation risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Stantec Narrative

If you see the numbers differently or prefer to dig into the assumptions yourself, you can craft a complete view in minutes: Do it your way.

A great starting point for your Stantec research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

Before you move on, lock in an edge by screening for fresh opportunities other investors might overlook, all powered by the same framework behind this narrative.

- Capture potential bargains early by targeting quality companies trading below their intrinsic value through these 916 undervalued stocks based on cash flows that focus on robust cash flow support.

- Ride structural growth trends by zeroing in on innovators at the intersection of medicine and machine learning using these 29 healthcare AI stocks to refine your watchlist.

- Tap into a new wave of digital asset adoption with these 80 cryptocurrency and blockchain stocks highlighting businesses positioned to benefit from blockchain infrastructure and crypto related services.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:STN

Stantec

Provides professional services in the areas of infrastructure and facilities to the public and private sectors in Canada, the United States, and internationally.

Solid track record with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion