Advertisement

National Bank of Canada (TSX:NA): Exploring Valuation Perspectives After 24% Share Price Gain in 2024

Simply Wall St

Reviewed by Simply Wall St

National Bank of Canada (TSX:NA) shares have delivered steady gains this year, rising 24% so far. Investors tracking Canadian banks may be curious about how these results compare with broader sector trends for 2024.

See our latest analysis for National Bank of Canada.

National Bank of Canada’s share price has jumped nearly 24% year-to-date, fueled by renewed confidence in Canadian financials and a steady drumbeat of positive sentiment around the sector. While the pace of gains has cooled recently, the bank’s three-year total shareholder return of 83% shows that long-term performance remains strong.

If you’re weighing what else is worth a closer look, now is a great time to broaden your investing horizons and discover fast growing stocks with high insider ownership.

With shares currently outpacing analyst price targets and the bank’s fundamentals still robust, the key question becomes whether National Bank of Canada is undervalued or if the market has already priced in the potential for future growth.

Most Popular Narrative: 6.5% Overvalued

With the latest fair value set at CA$151.69, National Bank of Canada’s most popular valuation narrative signals the shares are slightly overpriced compared to the last close of CA$161.54. This puts the focus squarely on future earnings and margin pressures driving expectations.

Successful integration of Canadian Western Bank (CWB) and rapid realization of cost and funding synergies are progressing ahead of expectations, with revenue synergies yet to come. This positions the bank for accelerated revenue growth and improved net margins as integration milestones are completed over the next 18 months.

What assumptions unlock this price premium? The primary drivers are ambitious revenue and profit projections, all linked to a future earnings multiple that exceeds the sector. Interested in which bold forecasts support that optimism? Find out exactly how far these numbers stretch the valuation.

Result: Fair Value of $151.69 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure and increased technology investment costs could still challenge sustained profitability. This makes future performance less certain than current optimism suggests.

Find out about the key risks to this National Bank of Canada narrative.

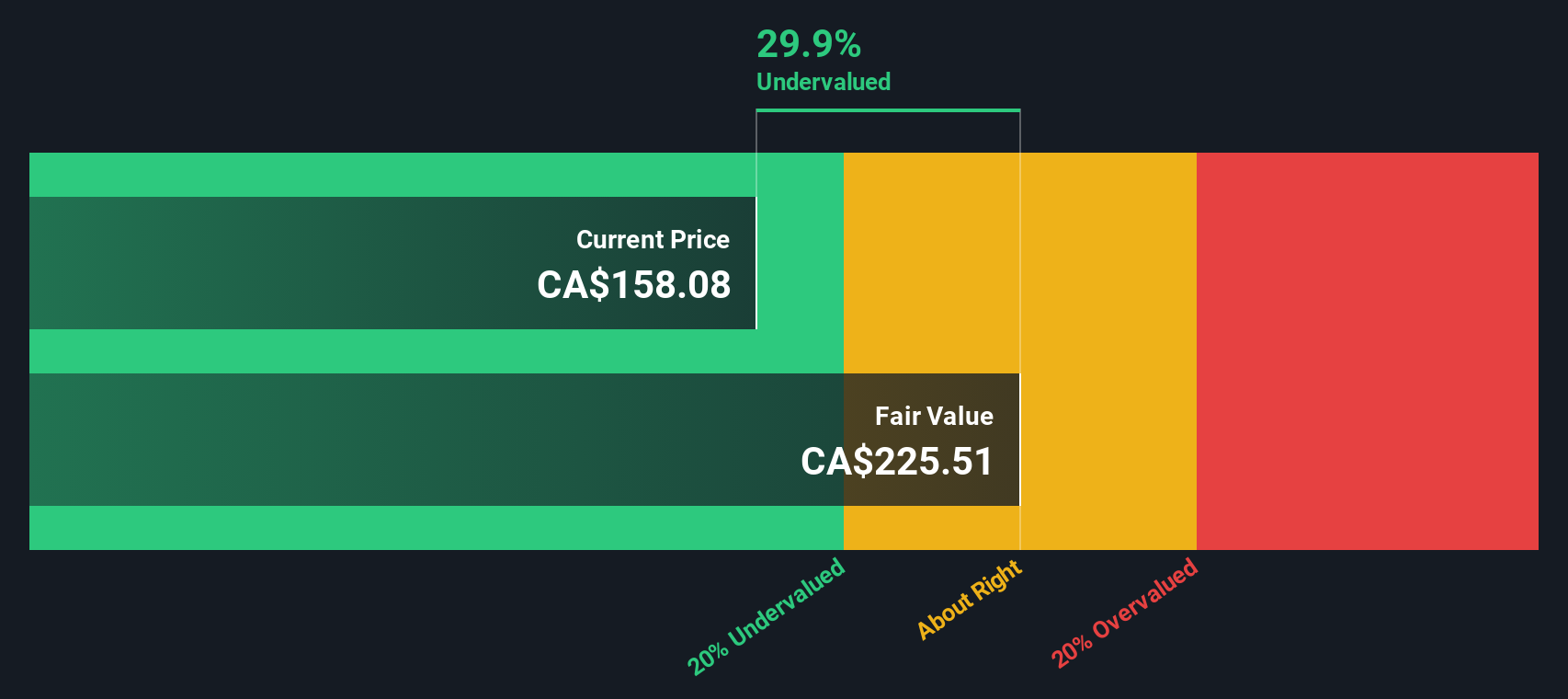

Another View: Discounted Cash Flow Points to Undervaluation

While recent analysis suggests National Bank of Canada is overvalued according to price targets and sector multiples, the SWS DCF model presents a different perspective. It estimates fair value at CA$221.63, which is significantly higher than today’s price. If accurate, this could indicate that shares are actually undervalued by a substantial amount. Which view best reflects reality?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out National Bank of Canada for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 904 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own National Bank of Canada Narrative

If you see things differently or want to chart your own path, it only takes a few minutes to analyze the numbers your way with Do it your way.

A great starting point for your National Bank of Canada research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors never stand still. If you want to future-proof your portfolio and avoid missing the next big opportunity, check out these standout stock ideas:

- Unlock steady income streams by targeting companies with strong yields through these 18 dividend stocks with yields > 3%, and get ahead with the latest in high-quality dividend opportunities.

- Capitalize on the artificial intelligence surge by sorting top innovators using these 27 AI penny stocks, where the fastest-growing disruptors are just a click away.

- Maximize your upside by zeroing in on value with these 904 undervalued stocks based on cash flows, connecting with shares that the market may be overlooking right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if National Bank of Canada might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NA

National Bank of Canada

Provides financial services to individuals, businesses, institutional clients, and governments in Canada and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor