Advertisement

Most Shareholders Will Probably Find That The CEO Compensation For Canadian Western Bank (TSE:CWB) Is Reasonable

Under the guidance of CEO Chris Fowler, Canadian Western Bank (TSE:CWB) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 01 April 2021. We present our case of why we think CEO compensation looks fair.

See our latest analysis for Canadian Western Bank

Comparing Canadian Western Bank's CEO Compensation With the industry

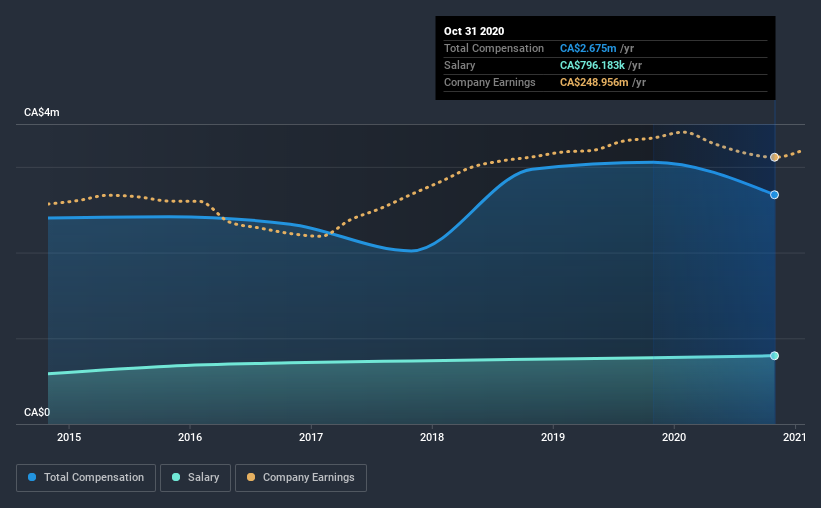

According to our data, Canadian Western Bank has a market capitalization of CA$2.8b, and paid its CEO total annual compensation worth CA$2.7m over the year to October 2020. Notably, that's a decrease of 12% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at CA$796k.

On examining similar-sized companies in the industry with market capitalizations between CA$1.3b and CA$4.0b, we discovered that the median CEO total compensation of that group was CA$2.9m. This suggests that Canadian Western Bank remunerates its CEO largely in line with the industry average. What's more, Chris Fowler holds CA$4.0m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | CA$796k | CA$774k | 30% |

| Other | CA$1.9m | CA$2.3m | 70% |

| Total Compensation | CA$2.7m | CA$3.1m | 100% |

On an industry level, around 11% of total compensation represents salary and 89% is other remuneration. According to our research, Canadian Western Bank has allocated a higher percentage of pay to salary in comparison to the wider industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Canadian Western Bank's Growth Numbers

Canadian Western Bank has seen its earnings per share (EPS) increase by 4.7% a year over the past three years. Its revenue is up 2.0% over the last year.

We'd prefer higher revenue growth, but it is good to see modest EPS growth. It's clear the performance has been quite decent, but it it falls short of outstanding,based on this information. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Canadian Western Bank Been A Good Investment?

Canadian Western Bank has generated a total shareholder return of 11% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. Despite the pleasing results, we still think that any proposed increases to CEO compensation will be examined based on a case by case basis and linked to performance outcomes.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 2 warning signs (and 1 which is concerning) in Canadian Western Bank we think you should know about.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

When trading Canadian Western Bank or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:CWB

Canadian Western Bank

As of February 3, 2025, Canadian Western Bank was acquired by National Bank of Canada.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor