Advertisement

- Canada

- /

- Food and Staples Retail

- /

- TSX:NWC

Top 3 TSX Dividend Stocks To Consider

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates a period of economic cooling and inflationary adjustments, investors are keeping a keen eye on dividend stocks as a potential source of steady income. With interest rates expected to remain low, selecting stocks that offer reliable dividends can be an effective strategy for those looking to bolster their portfolios amidst these evolving conditions.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 7.70% | ★★★★★★ |

| Russel Metals (TSX:RUS) | 4.20% | ★★★★★☆ |

| Savaria (TSX:SIS) | 3.17% | ★★★★★☆ |

| Olympia Financial Group (TSX:OLY) | 6.67% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.55% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 4.40% | ★★★★★☆ |

| IGM Financial (TSX:IGM) | 4.94% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.26% | ★★★★★☆ |

| Richards Packaging Income Fund (TSX:RPI.UN) | 5.93% | ★★★★★☆ |

| Acadian Timber (TSX:ADN) | 6.50% | ★★★★★☆ |

Click here to see the full list of 25 stocks from our Top TSX Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

Canadian Imperial Bank of Commerce (TSX:CM)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Canadian Imperial Bank of Commerce is a diversified financial institution offering a range of financial products and services to personal, business, public sector, and institutional clients across Canada, the United States, and internationally with a market cap of CA$77.52 billion.

Operations: Canadian Imperial Bank of Commerce generates revenue from several segments, including Canadian Personal and Business Banking (CA$8.97 billion), Capital Markets (CA$6.12 billion), Canadian Commercial Banking and Wealth Management (CA$5.69 billion), and U.S. Commercial Banking and Wealth Management (CA$2.37 billion).

Dividend Yield: 4.7%

Canadian Imperial Bank of Commerce offers stable dividends with a current payout ratio of 47.5%, ensuring coverage by earnings. The dividend has been reliable and growing over the past decade, though its yield of 4.68% is below Canada's top tier. Earnings grew by 20.7% last year and are forecasted to continue growing, supporting future dividends. Recent fixed-income offerings, including CAD 1.25 billion in subordinated debentures, may impact capital structure but demonstrate robust financing activities.

- Click to explore a detailed breakdown of our findings in Canadian Imperial Bank of Commerce's dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Canadian Imperial Bank of Commerce shares in the market.

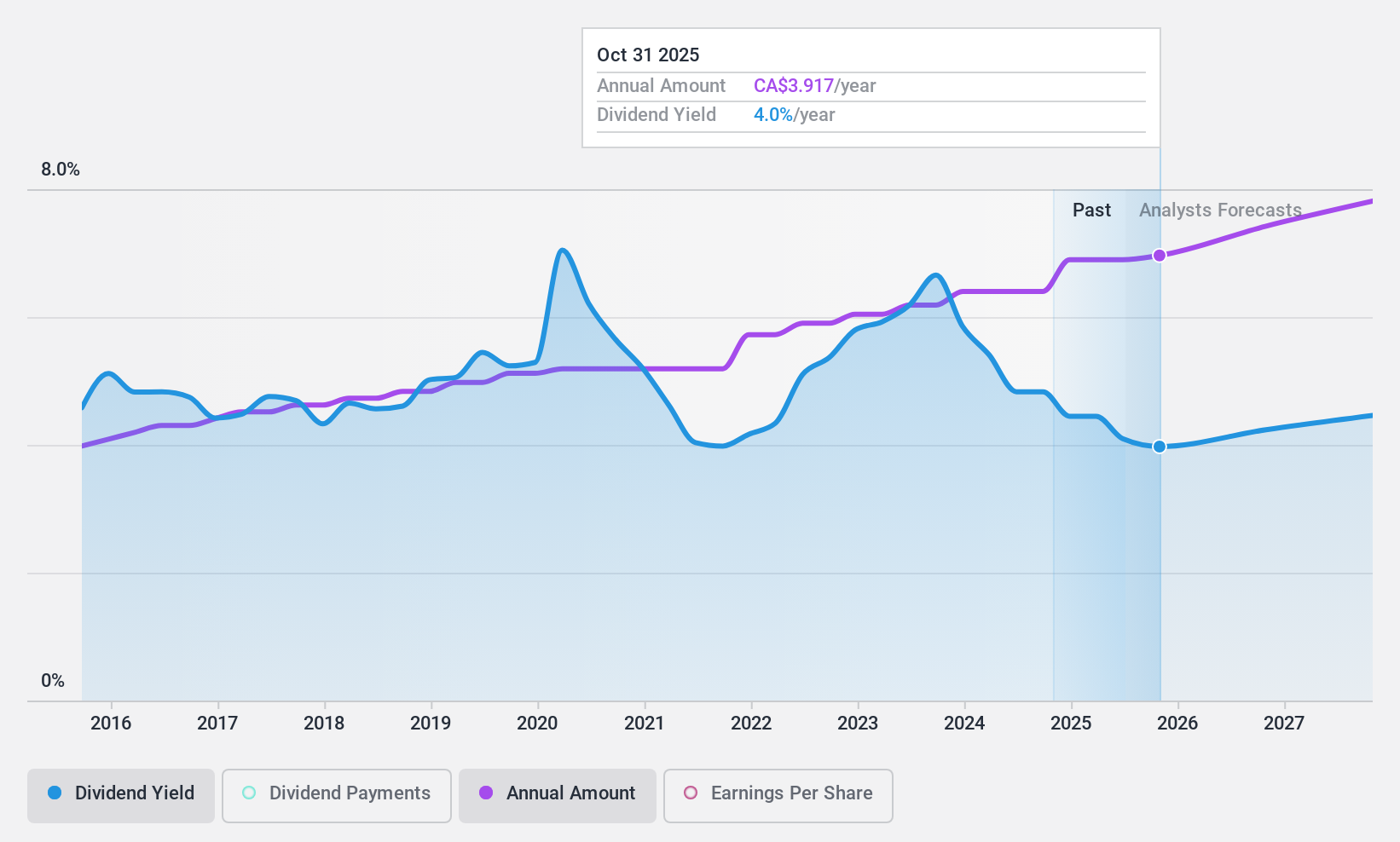

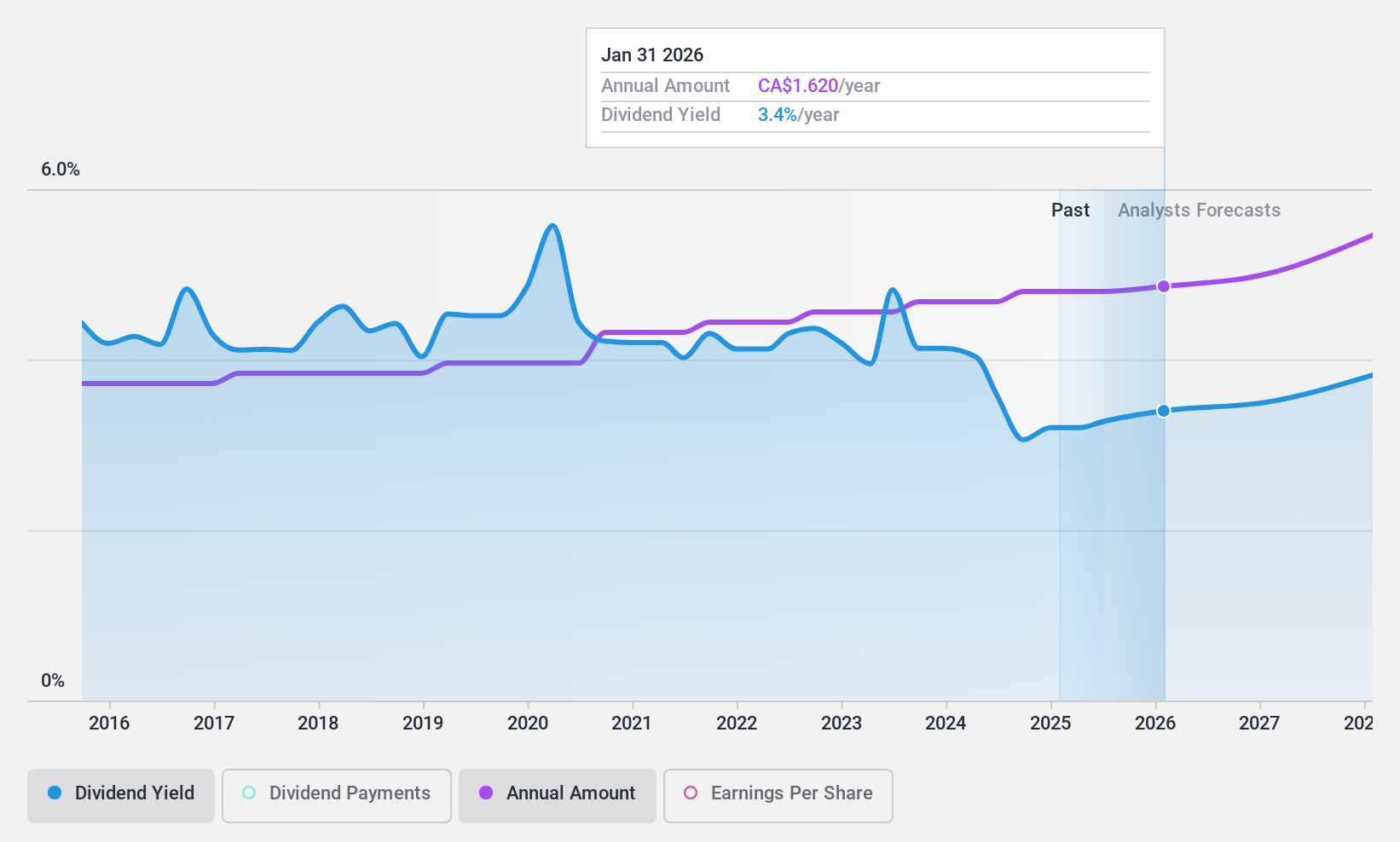

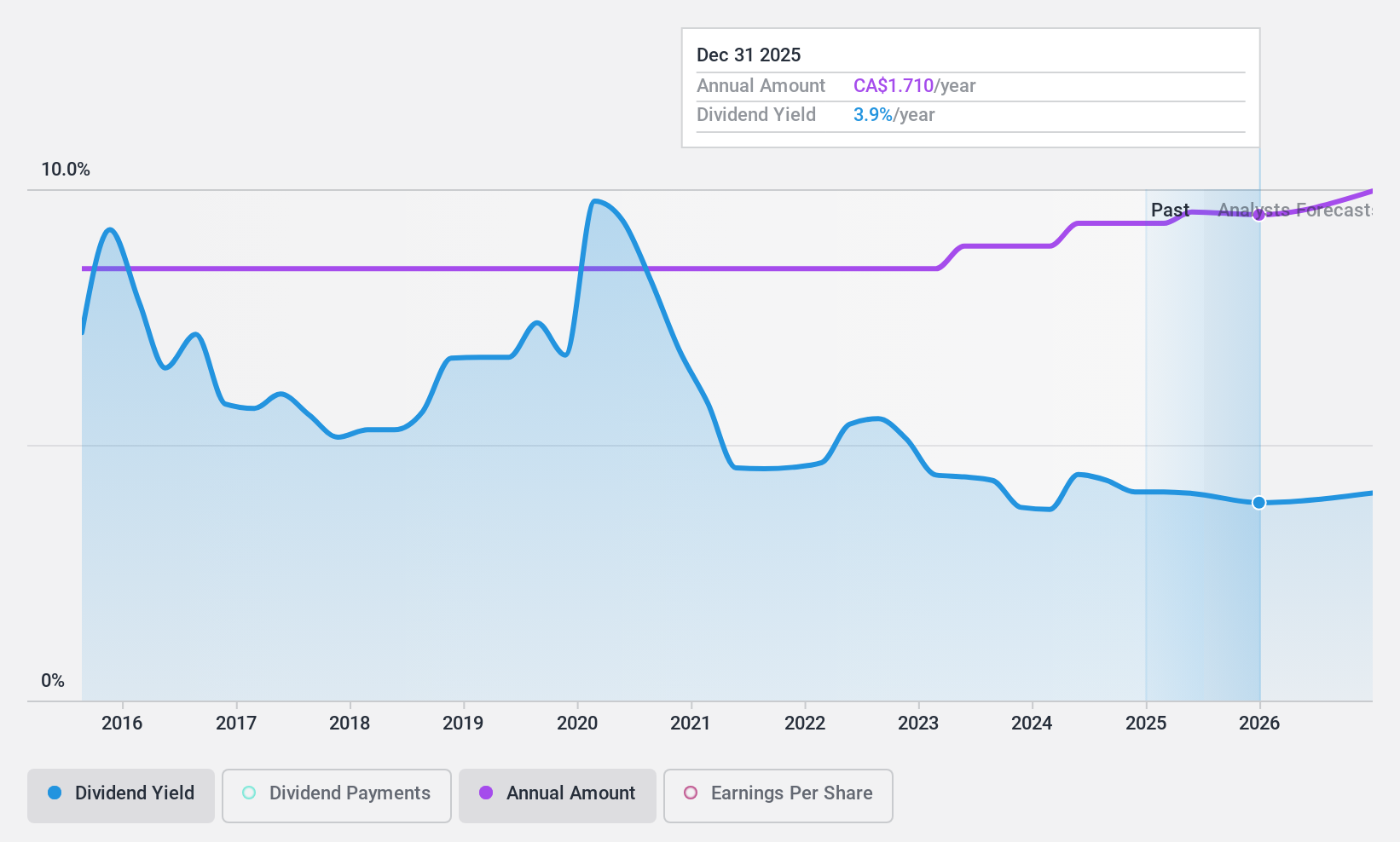

North West (TSX:NWC)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: The North West Company Inc. operates retail stores offering food and everyday products in rural and urban markets across northern Canada, rural Alaska, the South Pacific, and the Caribbean, with a market cap of CA$2.25 billion.

Operations: The North West Company Inc. generates revenue of CA$2.54 billion from retailing food and everyday products and services in various regions including northern Canada, rural Alaska, the South Pacific, and the Caribbean.

Dividend Yield: 3.4%

North West Company maintains a reliable dividend, supported by a payout ratio of 57.4% and cash payout ratio of 84.9%. With dividends stable over the past decade and consistent growth, the yield stands at 3.36%, below Canada's top tier. Revenue is projected to grow at 6.25% annually, while earnings increased by 1.4% last year. Trading significantly below estimated fair value, analysts anticipate a potential price increase of 23.1%.

- Take a closer look at North West's potential here in our dividend report.

- Our valuation report unveils the possibility North West's shares may be trading at a discount.

Russel Metals (TSX:RUS)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Russel Metals Inc. is involved in the distribution of steel and other metal products across Canada and the United States, with a market capitalization of approximately CA$2.25 billion.

Operations: Russel Metals Inc. generates revenue primarily from its Metals Service Centers at CA$2.87 billion, followed by Energy Field Stores at CA$983.90 million and Steel Distributors at CA$389.40 million.

Dividend Yield: 4.2%

Russel Metals Inc. offers a stable dividend, supported by a payout ratio of 60.7% and cash payout ratio of 37.7%. Despite a lower yield of 4.2% compared to Canada's top dividend payers, the dividends have been reliable over the past decade. Recent earnings showed reduced net income but continued dividend affirmations at $0.42 per share indicate commitment to shareholders. The CAD 300 million private placement may bolster financial stability amidst insider selling concerns.

- Dive into the specifics of Russel Metals here with our thorough dividend report.

- Upon reviewing our latest valuation report, Russel Metals' share price might be too pessimistic.

Turning Ideas Into Actions

- Discover the full array of 25 Top TSX Dividend Stocks right here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if North West might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NWC

North West

Through its subsidiaries, engages in the retail of food and everyday products and services in northern Canada, rural Alaska, the South Pacific, and the Caribbean.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor