Advertisement

- Canada

- /

- Auto Components

- /

- TSX:MG

Upgraded Sales Guidance and Safety Innovation Might Change The Case For Investing In Magna International (TSX:MG)

Simply Wall St

Reviewed by Simply Wall St

- Magna International recently reported higher net income and raised its full-year sales guidance, while also affirming its quarterly dividend, following advancements in its interior sensing safety technologies.

- The company’s focus on vehicle safety innovation, particularly in interior sensing systems like Child Presence Detection, underscores its commitment to meeting emerging regulatory and consumer demands in the automotive industry.

- Next, we'll explore how Magna’s upgraded annual sales guidance and earnings growth feed into the outlook for margin expansion and global competitiveness.

We've found 22 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Magna International Investment Narrative Recap

To be a shareholder in Magna International, you have to believe in the company's ability to drive margin expansion through operational improvements, innovation in vehicle safety, and disciplined capital management. The latest report of higher net income and an upgraded full-year sales outlook reinforces the short-term catalyst of margin improvement, but ongoing softness in vehicle production and foreign exchange pressures remain the biggest risks. These results have not materially reduced concerns over lower production volumes or macro pressures, risks that continue to deserve close attention.

Among recent announcements, Magna's affirmation of its quarterly dividend stands out by supporting the company's track record of reliable shareholder returns amid a period of heightened investment in safety technology. Stable dividends, alongside earnings growth, may help balance investor sentiment as the company manages margin pressures and global market uncertainties.

However, while profit growth appears solid, investors should be aware that underlying production headwinds and the strength of the U.S. dollar could eventually temper future earnings growth...

Read the full narrative on Magna International (it's free!)

Magna International's outlook forecasts $41.6 billion in revenue and $1.7 billion in earnings by 2028. This is based on a projected annual revenue decline of 1.0% and an earnings increase of $0.7 billion from the current $1.0 billion.

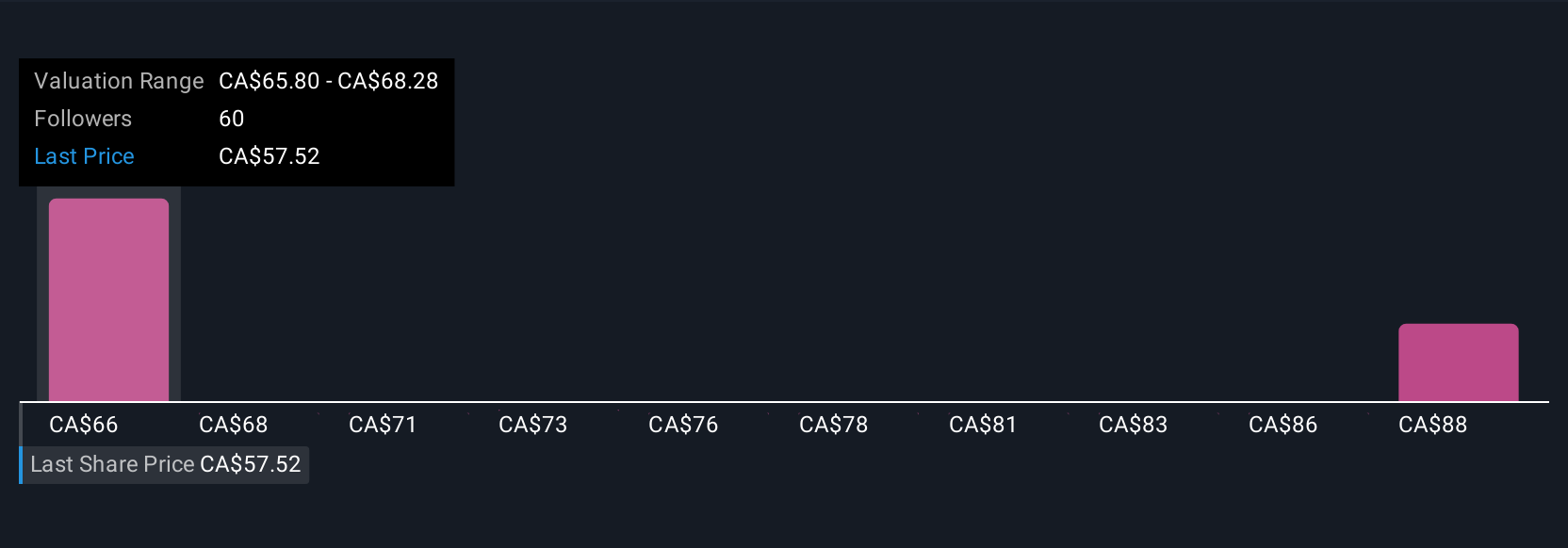

Uncover how Magna International's forecasts yield a CA$60.64 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Four members of the Simply Wall St Community valued Magna International between CA$60.64 and CA$92.33 per share. Ongoing macro challenges and uncertain production volumes may weigh on results, so it pays to assess a range of viewpoints before making decisions.

Explore 4 other fair value estimates on Magna International - why the stock might be worth just CA$60.64!

Build Your Own Magna International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Magna International research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Magna International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Magna International's overall financial health at a glance.

Curious About Other Options?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- These 18 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 26 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:MG

Magna International

Manufactures and supplies vehicle engineering, contract, and automotive space.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor