Advertisement

- Brazil

- /

- Electric Utilities

- /

- BOVESPA:LIGT3

Market Might Still Lack Some Conviction On Light S.A. (BVMF:LIGT3) Even After 27% Share Price Boost

Light S.A. (BVMF:LIGT3) shareholders would be excited to see that the share price has had a great month, posting a 27% gain and recovering from prior weakness. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 10% in the last twelve months.

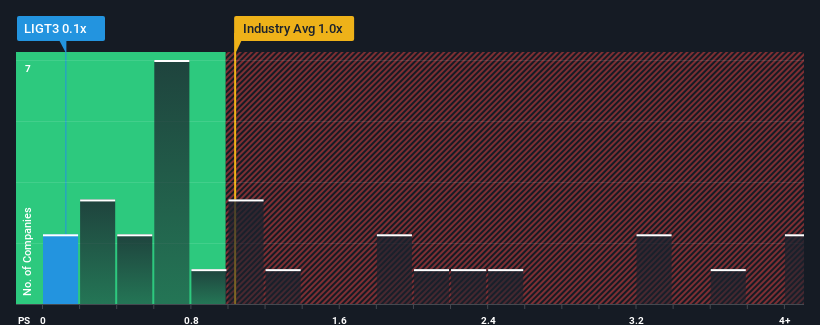

Even after such a large jump in price, it would still be understandable if you think Light is a stock with good investment prospects with a price-to-sales ratios (or "P/S") of 0.1x, considering almost half the companies in Brazil's Electric Utilities industry have P/S ratios above 1x. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Light

How Has Light Performed Recently?

Recent times haven't been great for Light as its revenue has been rising slower than most other companies. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Light.What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, Light would need to produce sluggish growth that's trailing the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.5% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 4.7% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should bring diminished returns, with revenue decreasing 8.8% as estimated by the dual analysts watching the company. With the rest of the industry predicted to shrink by 12%, it's still an optimal result.

In light of this, the fact Light's P/S sits below the majority of other companies is peculiar but certainly not shocking. With revenue going in reverse, it's not guaranteed that the P/S has found a floor yet. There's still potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Final Word

Despite Light's share price climbing recently, its P/S still lags most other companies. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Light's analyst forecasts revealed that its P/S ratio is lower than expected, given it's set to outperform the broader industry. The P/S ratio may not align with the more favourable outlook due to the market pricing in potential revenue risks. Perhaps there is some hesitation about the company's ability to keep resisting the broader industry turmoil. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Before you take the next step, you should know about the 1 warning sign for Light that we have uncovered.

If you're unsure about the strength of Light's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:LIGT3

Light

Engages in the generation, transmission, distribution, and sale of electric power in Brazil.

Undervalued with acceptable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor