Advertisement

- Brazil

- /

- Transportation

- /

- BOVESPA:SIMH3

SIMPAR (BVMF:SIMH3) Is Doing The Right Things To Multiply Its Share Price

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Speaking of which, we noticed some great changes in SIMPAR's (BVMF:SIMH3) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on SIMPAR is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

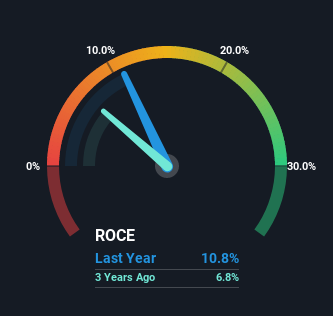

0.11 = R$5.3b ÷ (R$59b - R$10b) (Based on the trailing twelve months to March 2023).

Therefore, SIMPAR has an ROCE of 11%. That's a relatively normal return on capital, and it's around the 12% generated by the Transportation industry.

Check out our latest analysis for SIMPAR

Above you can see how the current ROCE for SIMPAR compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

SWOT Analysis for SIMPAR

Strength

- Debt is well covered by .

Weakness

- Earnings declined over the past year.

- Interest payments on debt are not well covered.

- Dividend is low compared to the top 25% of dividend payers in the Transportation market.

Opportunity

- Annual earnings are forecast to grow faster than the Brazilian market.

- Good value based on P/E ratio compared to estimated Fair P/E ratio.

Threat

- Debt is not well covered by operating cash flow.

- Paying a dividend but company has no free cash flows.

- Revenue is forecast to grow slower than 20% per year.

The Trend Of ROCE

We like the trends that we're seeing from SIMPAR. The data shows that returns on capital have increased substantially over the last five years to 11%. Basically the business is earning more per dollar of capital invested and in addition to that, 391% more capital is being employed now too. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

In Conclusion...

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what SIMPAR has. Astute investors may have an opportunity here because the stock has declined 22% in the last year. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

If you'd like to know more about SIMPAR, we've spotted 4 warning signs, and 2 of them don't sit too well with us.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:SIMH3

SIMPAR

Provides light vehicle rental, and fleet management and outsourcing services in Brazil.

Undervalued with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor