Stock Analysis

- Brazil

- /

- Consumer Services

- /

- BOVESPA:COGN3

Further weakness as Cogna Educação (BVMF:COGN3) drops 11% this week, taking five-year losses to 84%

Some stocks are best avoided. It hits us in the gut when we see fellow investors suffer a loss. For example, we sympathize with anyone who was caught holding Cogna Educação S.A. (BVMF:COGN3) during the five years that saw its share price drop a whopping 84%. And it's not just long term holders hurting, because the stock is down 48% in the last year. Shareholders have had an even rougher run lately, with the share price down 32% in the last 90 days. While a drop like that is definitely a body blow, money isn't as important as health and happiness.

After losing 11% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

Check out our latest analysis for Cogna Educação

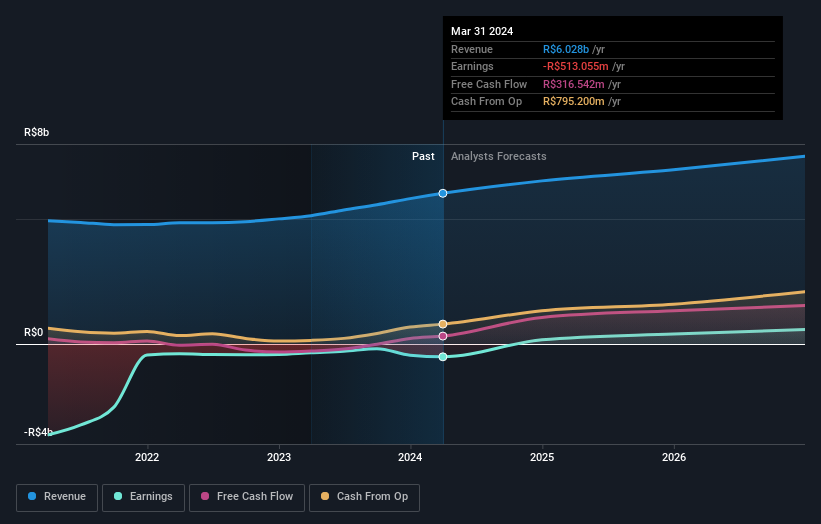

Cogna Educação isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Shareholders of unprofitable companies usually desire strong revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last five years Cogna Educação saw its revenue shrink by 3.9% per year. While far from catastrophic that is not good. The share price fall of 13% (per year, over five years) is a stern reminder that money-losing companies are expected to grow revenue. We're generally averse to companies with declining revenues, but we're not alone in that. Fear of becoming a 'bagholder' may be keeping people away from this stock.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

This free interactive report on Cogna Educação's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

Investors in Cogna Educação had a tough year, with a total loss of 48%, against a market gain of about 1.7%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 13% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Cogna Educação better, we need to consider many other factors. To that end, you should be aware of the 1 warning sign we've spotted with Cogna Educação .

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Brazilian exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Cogna Educação is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:COGN3

Cogna Educação

Operates as a private educational organization in Brazil and internationally.

Good value with reasonable growth potential.