Advertisement

- Bulgaria

- /

- Auto Components

- /

- BUL:BZR

Shareholders Would Enjoy A Repeat Of Balkancar ZARYA's (BUL:BZR) Recent Growth In Returns

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Speaking of which, we noticed some great changes in Balkancar ZARYA's (BUL:BZR) returns on capital, so let's have a look.

What Is Return On Capital Employed (ROCE)?

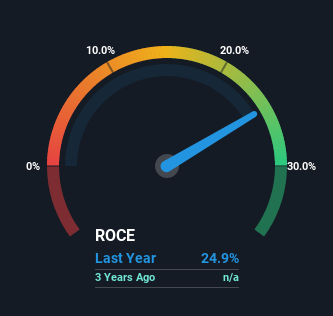

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for Balkancar ZARYA:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.25 = лв4.5m ÷ (лв22m - лв3.4m) (Based on the trailing twelve months to September 2022).

So, Balkancar ZARYA has an ROCE of 25%. In absolute terms that's a great return and it's even better than the Auto Components industry average of 7.0%.

Check out our latest analysis for Balkancar ZARYA

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Balkancar ZARYA, check out these free graphs here.

How Are Returns Trending?

The trends we've noticed at Balkancar ZARYA are quite reassuring. The data shows that returns on capital have increased substantially over the last two years to 25%. The amount of capital employed has increased too, by 38%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 16%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. This tells us that Balkancar ZARYA has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

The Key Takeaway

In summary, it's great to see that Balkancar ZARYA can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has returned a staggering 199% to shareholders over the last five years, it looks like investors are recognizing these changes. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

One more thing, we've spotted 3 warning signs facing Balkancar ZARYA that you might find interesting.

Balkancar ZARYA is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we're here to simplify it.

Discover if Balkancar ZARYA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BUL:BZR

Balkancar ZARYA

Engages in the manufacture and sale of steel rims and disc wheels in Bulgaria and internationally.

Slight risk with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor