Advertisement

We Discuss Why WiseTech Global Limited's (ASX:WTC) CEO May Deserve A Higher Pay Packet

Key Insights

- WiseTech Global will host its Annual General Meeting on 23rd of November

- Total pay for CEO Richard White includes AU$974.7k salary

- Total compensation is 94% below industry average

- WiseTech Global's total shareholder return over the past three years was 121% while its EPS grew by 8.5% over the past three years

Shareholders will be pleased by the robust performance of WiseTech Global Limited (ASX:WTC) recently and this will be kept in mind in the upcoming AGM on 23rd of November. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. In our analysis below, we discuss why we think the CEO compensation looks acceptable and the case for a raise.

Check out our latest analysis for WiseTech Global

Comparing WiseTech Global Limited's CEO Compensation With The Industry

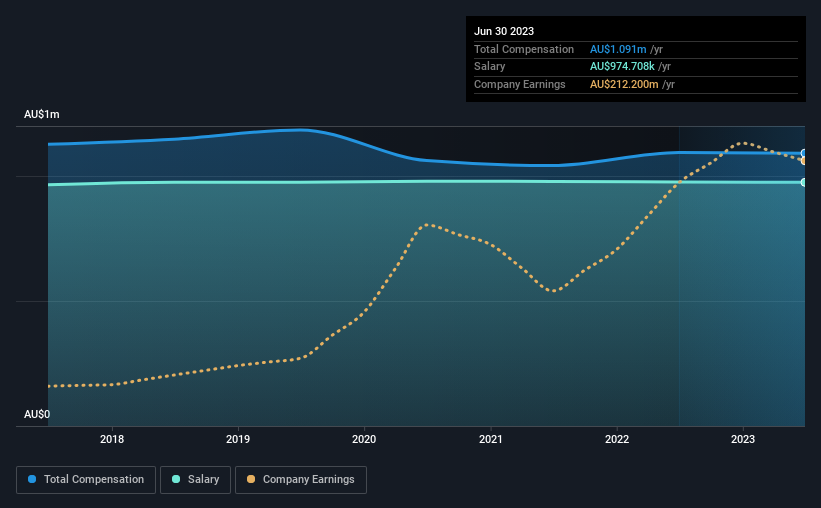

At the time of writing, our data shows that WiseTech Global Limited has a market capitalization of AU$22b, and reported total annual CEO compensation of AU$1.1m for the year to June 2023. That is, the compensation was roughly the same as last year. We note that the salary portion, which stands at AU$974.7k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the Australian Software industry with market capitalizations above AU$12b, reported a median total CEO compensation of AU$17m. This suggests that Richard White is paid below the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$975k | AU$976k | 89% |

| Other | AU$117k | AU$118k | 11% |

| Total Compensation | AU$1.1m | AU$1.1m | 100% |

On an industry level, around 59% of total compensation represents salary and 41% is other remuneration. According to our research, WiseTech Global has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at WiseTech Global Limited's Growth Numbers

WiseTech Global Limited's earnings per share (EPS) grew 8.5% per year over the last three years. It achieved revenue growth of 29% over the last year.

It's hard to interpret the strong revenue growth as anything other than a positive. With that in mind, the modestly improving EPS seems positive. We'd stop short of saying the business performance is amazing, but there are enough positives to justify further research, or even adding the stock to your watch-list. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has WiseTech Global Limited Been A Good Investment?

We think that the total shareholder return of 121%, over three years, would leave most WiseTech Global Limited shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. Rather, investors would more likely want to engage on discussions related to key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

If you think CEO compensation levels are interesting you will probably really like this free visualization of insider trading at WiseTech Global.

Switching gears from WiseTech Global, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if WiseTech Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:WTC

WiseTech Global

Engages in the development and provision of software solutions to the logistics execution industry in the Americas, the Asia Pacific, Europe, the Middle East, and Africa.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor